Will Avista's (AVA) Modest 2025 Profit Gain Signal a More Durable Efficiency Narrative?

Avista Corporation AVA | 41.34 | +1.62% |

- Avista Corporation has released its full-year 2025 results, reporting revenue of US$1,964 million and net income of US$193 million, with basic and diluted earnings per share from continuing operations of US$2.38, all modestly higher than the prior year.

- The combination of slightly higher sales and a lift in earnings per share suggests improved operational efficiency and cost management over 2024.

- Now we’ll explore how Avista’s higher full-year net income and earnings per share shape its existing investment narrative and outlook.

Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Avista Investment Narrative Recap

To own Avista, you need to be comfortable with a regulated utility that is steadily investing for long term grid and generation needs while managing regulatory and wildfire related risks in the Pacific Northwest. The 2025 results, with modestly higher revenue and earnings, support the short term catalyst around capital investment and rate recovery, but they do not materially change the key near term risk that rising spend could pressure the balance sheet if regulators limit cost recovery.

Among recent announcements, the February 2026 dividend increase to US$0.4925 per share quarterly (US$1.97 annualized) is most relevant to these earnings. It ties the slightly stronger 2025 net income and earnings per share to Avista’s ongoing capital plan and regulatory outcomes, since sustaining and growing the dividend depends on cash flows keeping pace with rising grid modernization and wildfire mitigation spend. Yet investors should still pay close attention to how future rate cases address...

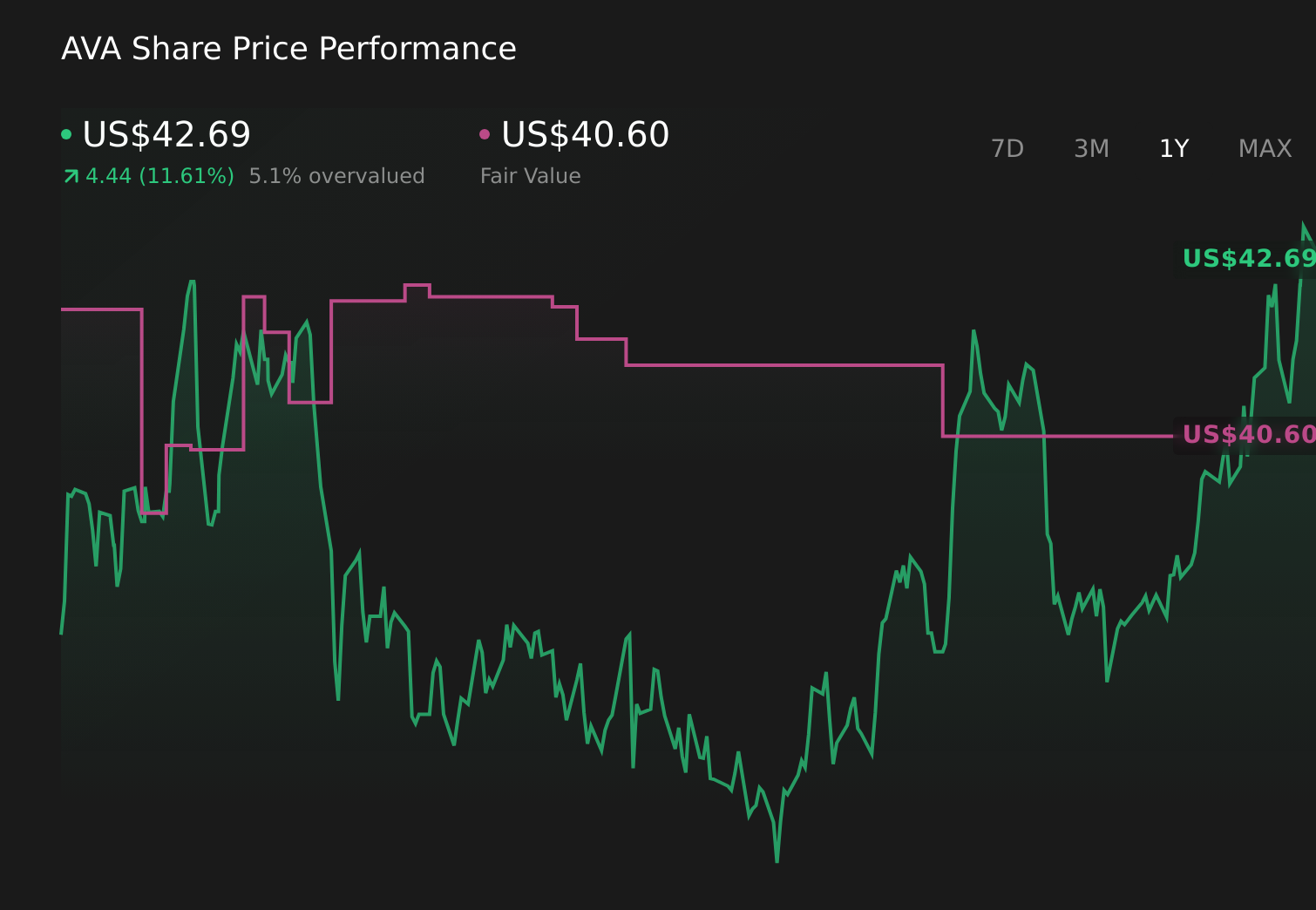

Avista's narrative projects $2.1 billion revenue and $245.2 million earnings by 2028.

Uncover how Avista's forecasts yield a $40.60 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between about US$37.83 and US$40.60, showing how far personal views can diverge. You can weigh these against the central risk that rising capital expenditure for grid upgrades and wildfire mitigation could strain cash flows if regulatory decisions limit timely cost recovery, with clear implications for how you think about Avista’s future performance.

Explore 2 other fair value estimates on Avista - why the stock might be worth as much as $40.60!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Avista research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.