Will Bandwidth’s (BAND) Zero-Coupon Converts Quietly Redefine Its AI Communications Investment Story?

Bandwidth Inc. Class A BAND | 0.00 |

- Earlier this month, Bandwidth Inc. completed a US$275,000,000 private Rule 144A offering of callable, senior unsecured zero-coupon convertible notes due July 1, 2032.

- Alongside this financing, Bandwidth named veteran cloud communications executive Kimberly McLachlan as Chief Revenue Officer to lead enterprise-focused growth of its AI-driven Communications Cloud.

- Now we’ll examine how the zero-coupon convertible notes offering reshapes Bandwidth’s existing investment narrative built around AI-driven communications.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Bandwidth Investment Narrative Recap

To own Bandwidth, you need to believe its AI-driven Communications Cloud and Maestro platform can stay mission-critical for large enterprises while managing capital intensity and competition. In the near term, the key catalyst is continued enterprise adoption of AI communications, while a major risk is pressure on margins from rising R&D and network spend. The new US$275,000,000 zero-coupon convertible notes add non-cash financing flexibility but do not materially change these core drivers.

The recent appointment of Kimberly McLachlan as Chief Revenue Officer ties directly into this financing story. As Bandwidth leans into enterprise-focused AI communications, her track record in scaling cloud communications revenues may be central to turning today’s capital raise and AI partnerships, such as Salesforce’s Agentforce Contact Center integration, into higher quality, longer term enterprise contracts that support the company’s growth ambitions while balancing the risk of concentrated large customers.

Yet even as AI momentum builds, investors should be aware that rising compliance and regulatory costs could still...

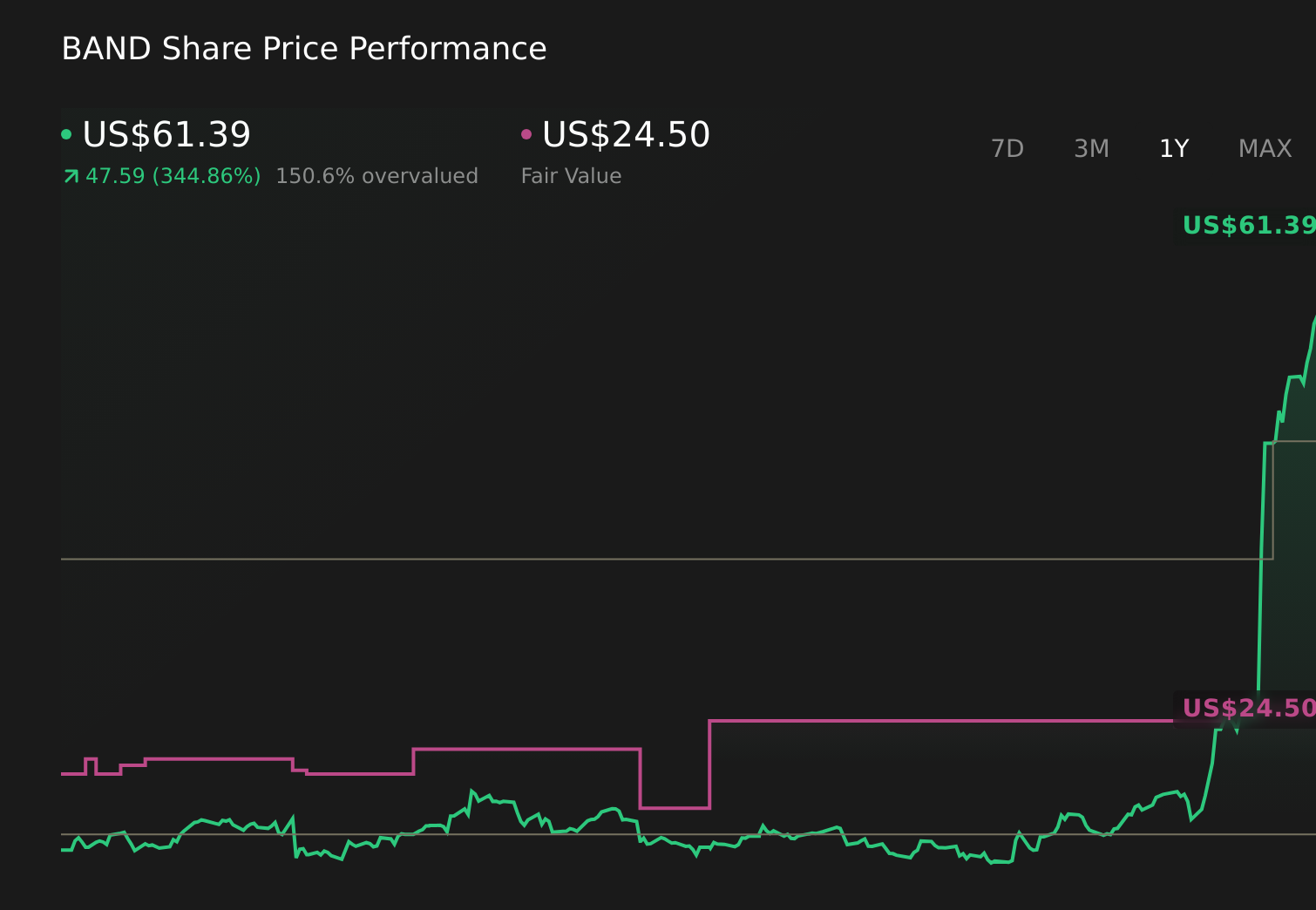

Bandwidth's narrative projects $987.7 million revenue and $17.8 million earnings by 2028.

Uncover how Bandwidth's forecasts yield a $24.50 fair value, a 52% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already projecting revenue of about US$1.2 billion and earnings of roughly US$82.7 million by 2029, so if you see AI partnerships and the new convertible notes as reinforcing that upside while others worry more about commoditization and rising compliance costs, it shows how far views can differ and why it is worth comparing several perspectives before deciding what you believe.

Explore 3 other fair value estimates on Bandwidth - why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bandwidth research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Bandwidth research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bandwidth's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 31 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.