Will Delta Air Lines' (DAL) Leadership Shake-Up Reframe Its Balance Between Cost Discipline and Customer Experience?

Delta Air Lines, Inc. DAL | 66.76 | -1.24% |

- Earlier this month, Delta Air Lines announced a wide-ranging leadership reshuffle effective April 2026, promoting Peter Carter to President, moving CFO Dan Janki into the Chief Operating Officer role, appointing Erik Snell as Chief Financial Officer, and adjusting responsibilities across its international, operations, and marketing teams following key retirements and departures.

- This reorganization concentrates decision-making around enterprise strategy, operations, finance, and customer-facing functions under CEO Ed Bastian’s direct reports, potentially reshaping how Delta balances cost control, service quality, and global growth priorities.

- We’ll now examine how this leadership overhaul, particularly Erik Snell’s move from customer experience to CFO, could influence Delta’s investment narrative.

We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Delta Air Lines Investment Narrative Recap

To own Delta today, you need to believe its focus on premium, loyalty and international revenue can offset fuel volatility and softer main cabin demand. The leadership reshuffle, especially Erik Snell’s move from customer experience to CFO, does not materially change the near term fuel cost risk, which remains the key swing factor for margins and sentiment.

The most relevant recent announcement here is Delta’s confirmation of 2026 earnings guidance in January, which some analysts warned could be at risk if WTI crude moves toward US$100. Snell’s expanded remit over finance, fleet and Monroe Energy now sits right at the intersection of that guidance and fuel exposure, making upcoming updates on costs and capacity particularly important to watch.

But while the headlines focus on upside, investors should also be aware that rising fuel costs and guidance sensitivity could...

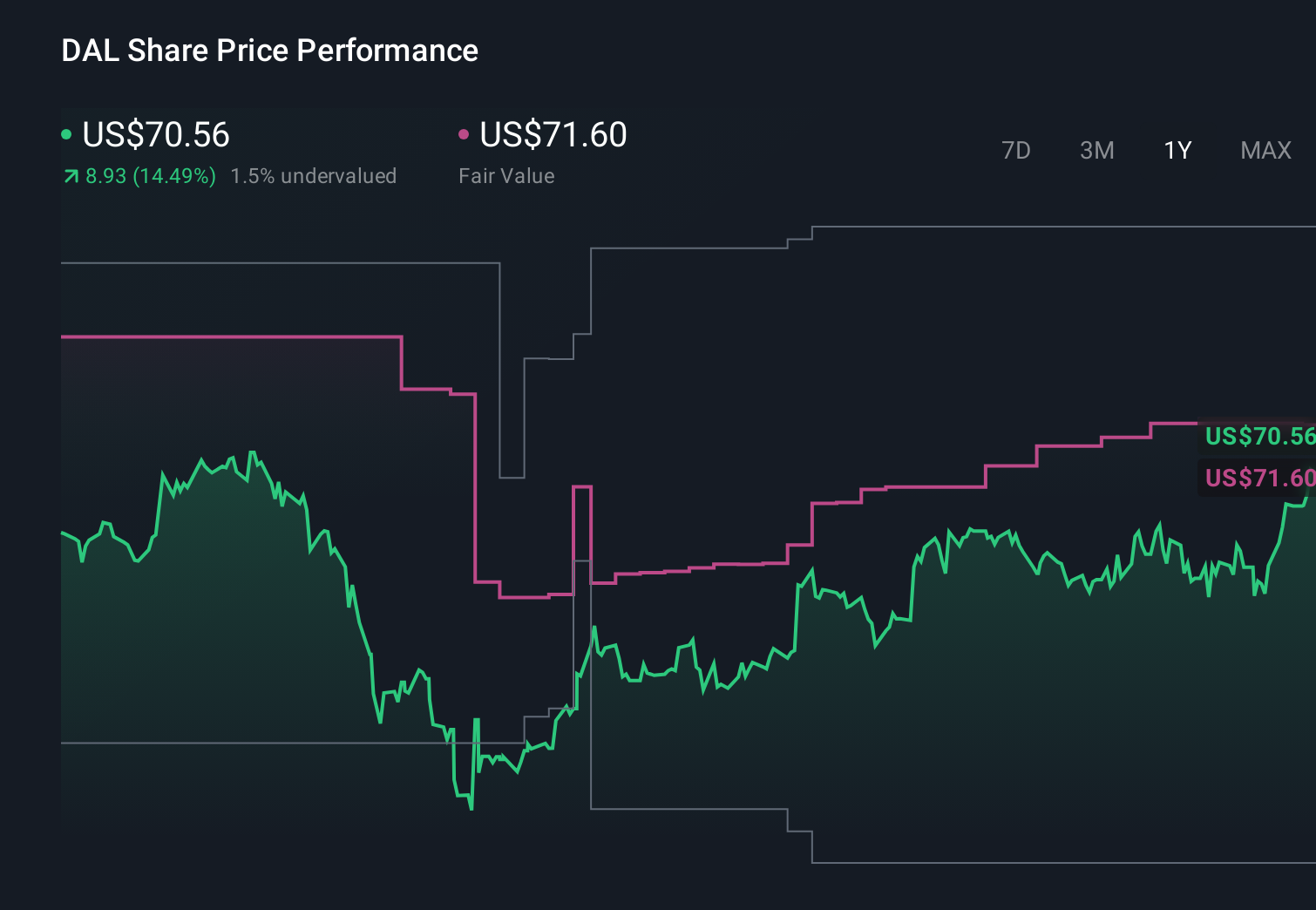

Delta Air Lines' narrative projects $68.4 billion revenue and $4.6 billion earnings by 2028. This requires 3.4% yearly revenue growth and a modest $0.1 billion earnings increase from $4.5 billion today.

Uncover how Delta Air Lines' forecasts yield a $81.29 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the most optimistic analysts were assuming Delta could lift revenue to about US$70.6 billion and earnings to US$6.2 billion, helped by premium and loyalty growth, yet this leadership shake up and fuel uncertainty could easily shift how realistic that more optimistic path looks, so it is worth weighing both the upside story and the risk that demand softness in domestic main cabin travel lingers longer than expected.

Explore 10 other fair value estimates on Delta Air Lines - why the stock might be worth 9% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Delta Air Lines research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.