Will Devon’s Marcellus Sale and Bigger Buyback Shift Devon Energy’s (DVN) Capital Return Narrative?

Devon Energy Corporation DVN | 0.00 |

- In recent weeks, Devon Energy advanced its merger with Coterra Energy, moved toward divesting its Marcellus asset after receiving an approximately US$8.00 billion offer, and filed to issue up to 175,000 shares tied to preferred stock conversion.

- Alongside these changes, Devon announced a new share repurchase authorization exceeding US$5.00 billion and a higher fixed dividend, highlighting a sharper focus on returning cash to shareholders.

- We’ll now examine how the planned Marcellus divestiture and larger buyback program may reshape Devon Energy’s previously outlined investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Devon Energy Investment Narrative Recap

To own Devon, you need to be comfortable with a U.S. shale producer whose cash flows are tightly linked to oil and gas prices and ongoing drilling needs. Right now, the key near term catalyst is the Coterra merger and how quickly Devon can simplify its asset base and capital structure. The Marcellus sale talks and planned buybacks support that focus, but they do not remove core risks around commodity volatility and high decline rate assets.

The planned Marcellus divestiture is the most relevant development here, because it directly affects Devon’s asset mix and potential balance sheet flexibility. If completed around the time of the Coterra merger close, it could leave the combined company more concentrated in its core shale basins while freeing capacity to support the new US$5.0 billion plus repurchase program and higher fixed dividend, both of which tie directly into the near term capital return catalyst.

Yet while capital returns may look attractive, investors should also be aware of how Devon’s concentrated U.S. shale exposure could amplify the effects of...

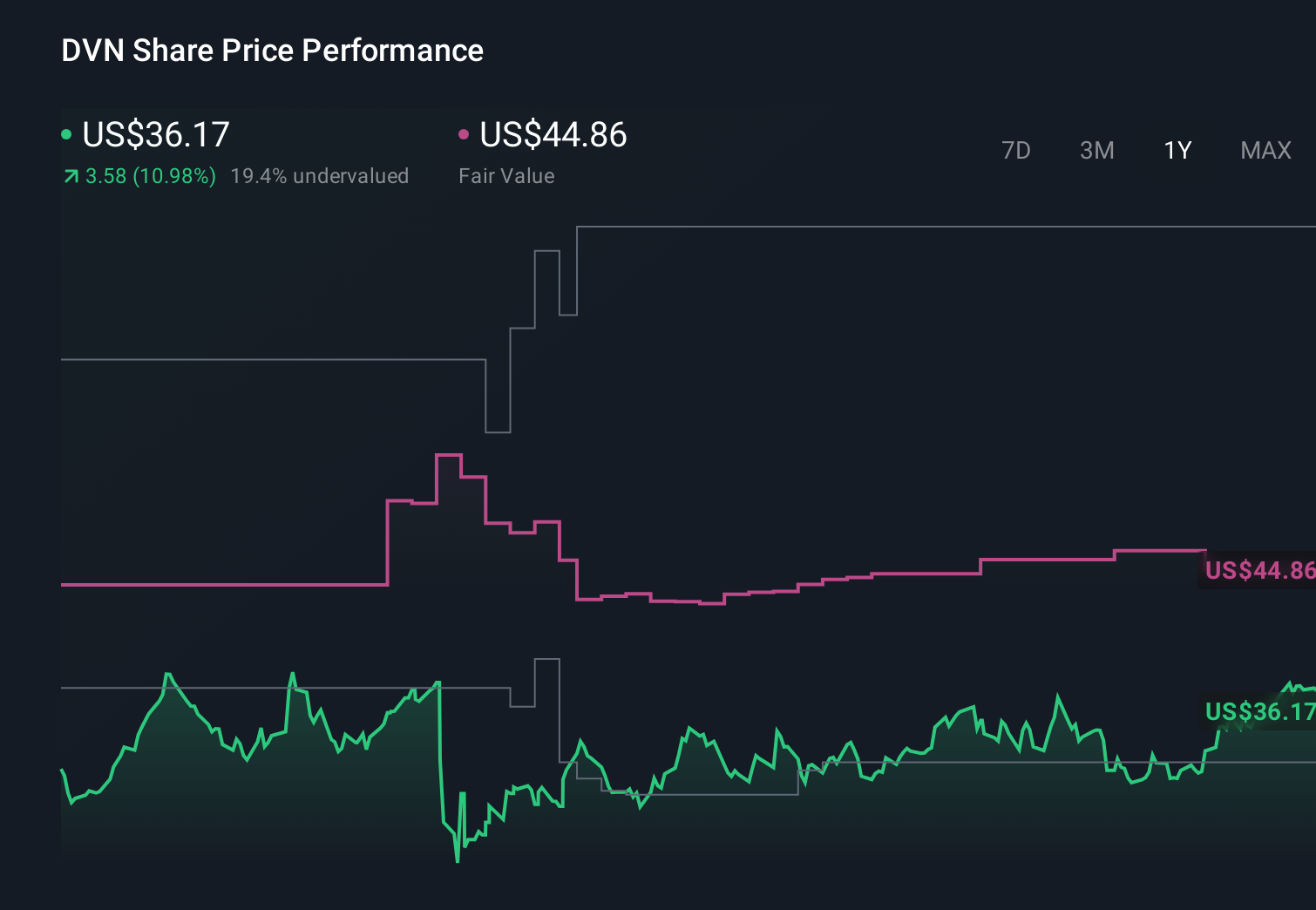

Devon Energy's narrative projects $23.3 billion revenue and $4.8 billion earnings by 2029.

Uncover how Devon Energy's forecasts yield a $59.28 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were assuming only about 8 percent annual revenue growth and a PE near 8.8x by 2029, which is far more pessimistic than the consensus, so it is worth comparing those expectations to your own and seeing how this latest merger and divestiture news might shift the balance of risks and potential outcomes.

Explore 8 other fair value estimates on Devon Energy - why the stock might be worth over 3x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Devon Energy research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.