Will Devon’s Q2 Synergy Update and Asset Sales Strategy Change Devon Energy's (DVN) Narrative

Devon Energy Corporation DVN | 0.00 |

- In the past week, Devon Energy drew attention as investors looked ahead to its August 4, 2026 Q2 earnings release and the first detailed update on its recently combined organization following acquisition activity.

- Beyond the headline expectations for stronger earnings and revenue, the upcoming report is set to spotlight how efficiently Devon is capturing integration synergies and reshaping its asset portfolio through planned divestitures.

- We’ll now examine how expectations for Q2 integration progress and synergy updates could influence Devon Energy’s broader investment narrative and risks.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Devon Energy Investment Narrative Recap

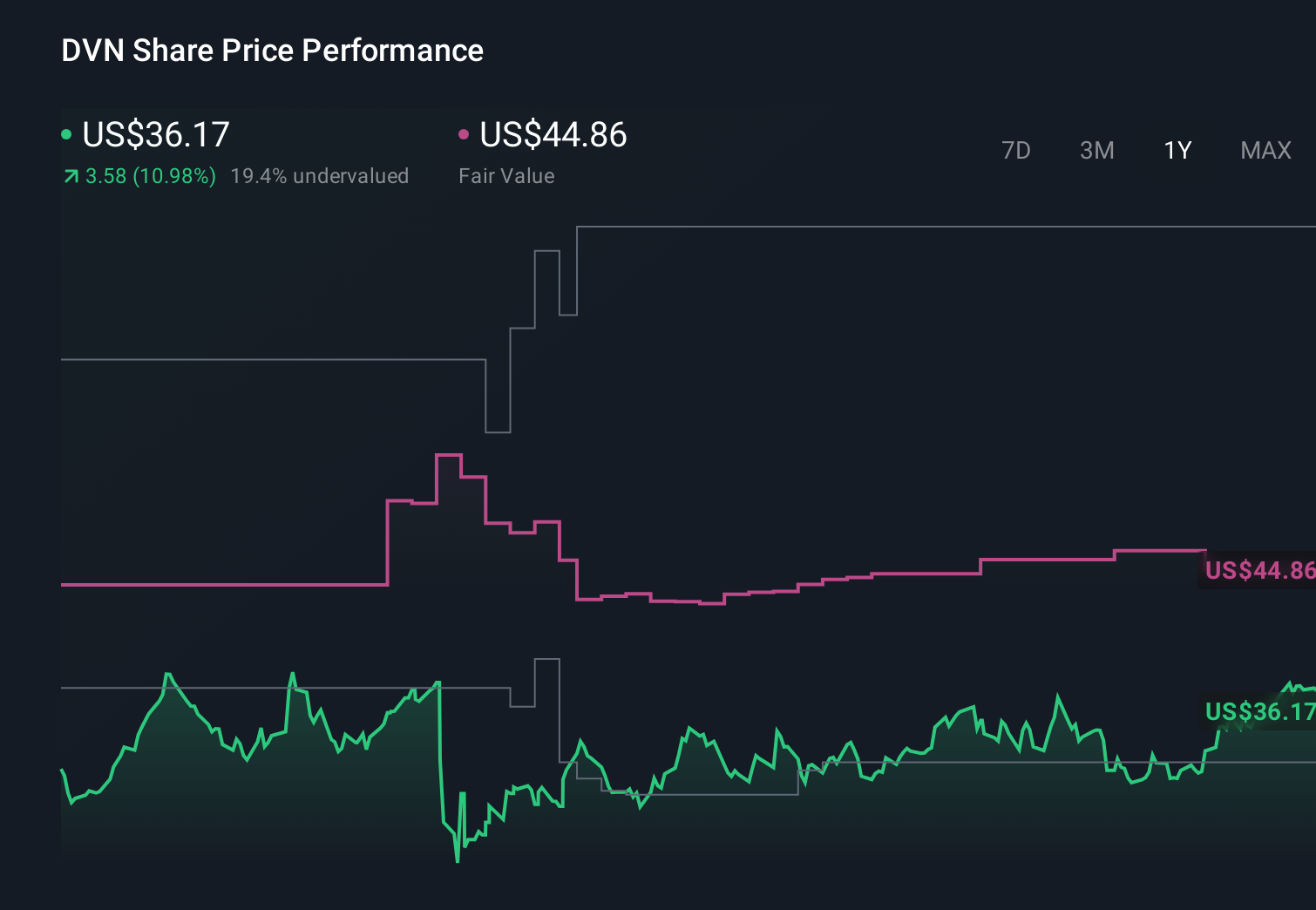

To own Devon Energy today, you need to believe the combined company can translate its U.S. shale footprint and integration efforts into durable free cash flow, despite commodity and regulatory uncertainty. The upcoming August 4 Q2 report is the clearest short term catalyst, as it should clarify merger integration progress and planned divestitures. The recent share pullback and estimate revisions do not appear to materially change the key risk, which remains Devon’s dependence on volatile oil and gas prices.

Among recent announcements, the expanded US$8.0 billion share repurchase authorization stands out in light of the upcoming Q2 update. While the market is focused on earnings growth and synergy capture, this long dated buyback plan, paired with the higher fixed dividend, reinforces that Devon is prioritizing capital returns even as it absorbs new assets, restructures its balance sheet, and responds to activist pressure around portfolio sales.

But while the integration story is front and center, investors also need to be aware of the growing regulatory and environmental pressure that could...

Devon Energy's narrative projects $23.3 billion revenue and $4.8 billion earnings by 2029.

Uncover how Devon Energy's forecasts yield a $59.28 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Compared with the consensus story around integration and cost efficiencies, the most pessimistic analysts paint a very different picture, assuming revenue of about US$22.8 billion and earnings of roughly US$5.6 billion by 2029, yet only assigning a low valuation multiple. As you weigh fresh Q2 synergy and divestiture details, it is worth remembering that views on Devon’s long term risk and reward can differ sharply, and that new information could shift both the bullish and bearish cases.

Explore 8 other fair value estimates on Devon Energy - why the stock might be worth just $48.44!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Devon Energy research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Devon Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Devon Energy's overall financial health at a glance.

No Opportunity In Devon Energy?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.