Will Earnings Estimate Downgrades Amid Solid Margins Change Royal Caribbean Cruises' (RCL) Narrative?

Royal Caribbean Group RCL | 0.00 |

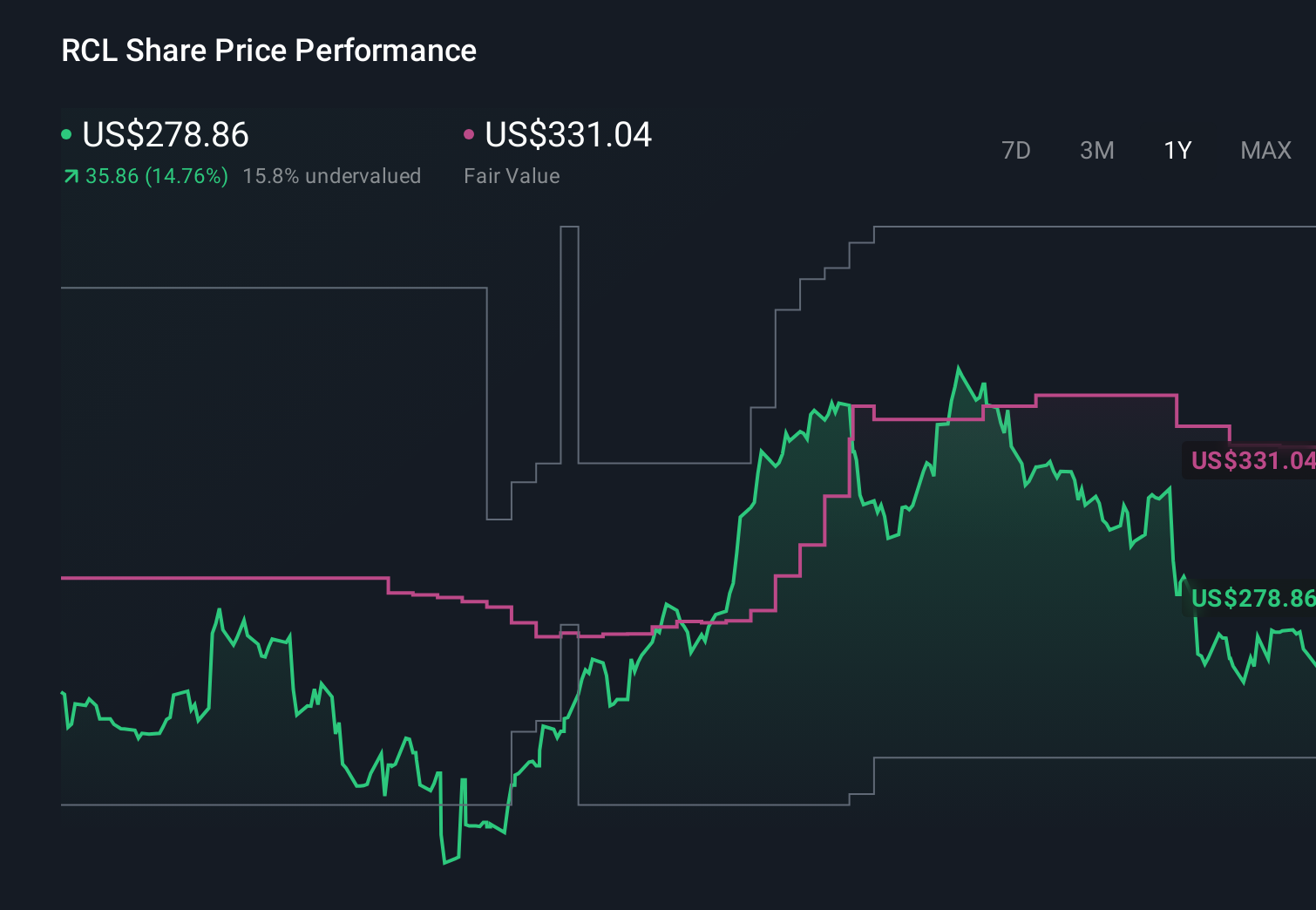

- In recent days Royal Caribbean Cruises has drawn increased investor attention after earnings estimate downgrades led Zacks to assign the stock a Rank #5 (Strong Sell), even as revenue and net margins remain solid.

- This contrast between weaker earnings revisions and ongoing operational strength, including a large global fleet and revenue growth, has sharpened debate about the company’s near-term outlook.

- We’ll now examine how these earnings estimate downgrades, despite healthy margins, may influence Royal Caribbean’s existing investment narrative and assumptions.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean today, you need to believe that experience-focused travel, a global fleet of nearly 70 ships, and strong net margins can continue to support earnings, even as the macro backdrop and consumer spending remain uncertain. The Zacks Rank #5 (Strong Sell) on the back of earnings estimate downgrades sharpens attention on the key near term catalyst of yield and occupancy trends, while reinforcing the main risk that any softening in demand or pricing could pressure margins.

The most relevant recent development is Zacks’ downgrade following weaker earnings revisions despite Royal Caribbean’s solid 23.8% net margin and revenue growth. This tension between reduced earnings expectations and ongoing operational strength, including high load factors and expanding itineraries, will be central to how investors weigh upcoming catalysts such as new ship introductions, private destinations, and loyalty driven onboard spending against risks tied to any slowdown in close in bookings or consumer confidence...

Royal Caribbean Cruises' narrative projects $23.5 billion revenue and $6.1 billion earnings by 2029. This requires 8.6% yearly revenue growth and a $1.6 billion earnings increase from $4.5 billion today.

Uncover how Royal Caribbean Cruises' forecasts yield a $338.33 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Against this backdrop, the most bearish analysts were already assuming revenue of about US$23.0 billion and earnings of roughly US$5.8 billion by 2029, so you should expect that some of these more cautious voices may now see the combination of estimate cuts and rising regulatory and environmental pressures as further evidence that Royal Caribbean’s long term profit path is less certain than the consensus suggests, and it is worth weighing that more pessimistic view against your own assumptions.

Explore 6 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth as much as 52% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.