Will Flowserve’s (FLS) Activist Clash Over Margins and Targets Change Its Long-Term Narrative?

Flowserve Corporation FLS | 0.00 |

- In late May 2026, Flowserve Corporation responded to an activist letter from Starboard Value LP by emphasizing 860-basis-point adjusted operating margin improvement since 2022, reaffirming 2026 guidance, and reiterating 2030 financial targets underpinned by aftermarket strength and a resurgent power and nuclear market linked to AI, data centers, and electrification.

- The exchange spotlights how investor pressure is intersecting with Flowserve’s push for portfolio optimization, capital deployment, and margin expansion to support long-term value creation.

- Now, we’ll examine how Flowserve’s reaffirmed long-term margin and earnings targets in response to Starboard’s activism influence its existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Flowserve Investment Narrative Recap

To own Flowserve, you need to believe its margin expansion, aftermarket mix, and exposure to power and nuclear can support durable earnings, even with uneven project timing. The Starboard exchange underscores near term focus on hitting 2026 guidance and safeguarding the margin story; for now, the activism itself does not materially change the key catalyst of execution on margin and earnings targets or the top risk of project delays and pricing pressure in large engineered orders.

The most relevant recent announcement here is Flowserve’s reaffirmation of its 2026 guidance and 2030 targets after Q1 2026 results, including adjusted margin expansion and double digit EPS growth. That reaffirmation, now reiterated in response to Starboard, ties directly to the core catalyst of sustained profitability improvement, but it also heightens the importance of delivering on complexity reduction and growth initiatives without causing the revenue or backlog volatility that could unsettle the story.

Yet beneath this margin progress, investors should also be aware of the risk that tighter, more competitive bidding could...

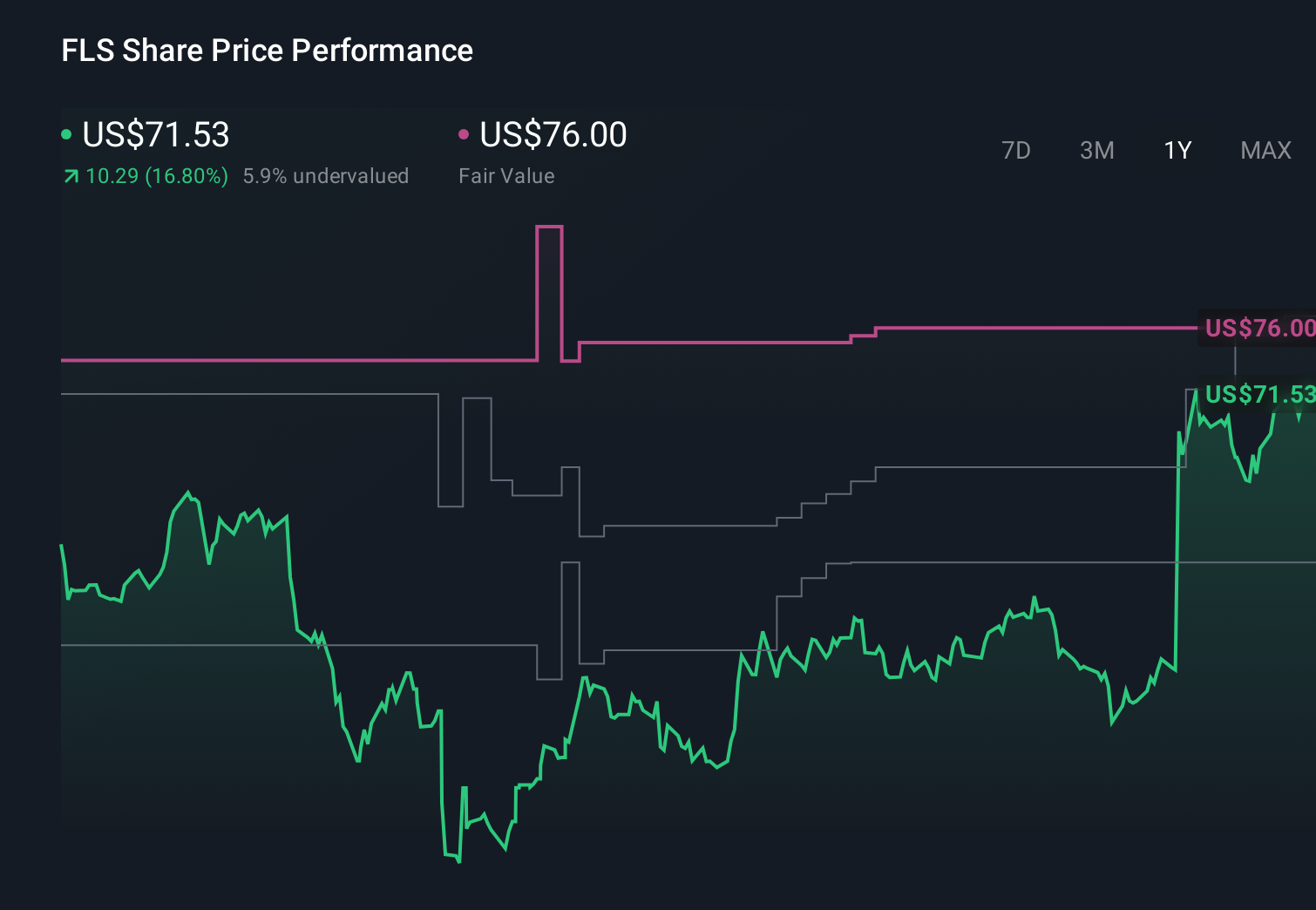

Flowserve's narrative projects $5.6 billion revenue and $660.0 million earnings by 2029. This requires 5.5% yearly revenue growth and about a $313.8 million earnings increase from $346.2 million today.

Uncover how Flowserve's forecasts yield a $94.80 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$5.7 billion and earnings near US$697 million, yet they still flagged Flowserve’s exposure to fossil fuel end markets as a key long term risk, reminding you that views can differ widely and may shift again as the Starboard activism and AI driven power demand story evolve.

Explore 5 other fair value estimates on Flowserve - why the stock might be worth just $80.93!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Flowserve research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.