Will GM’s (GM) Shift Toward Trucks and Subscriptions Change Its EV-Led Growth Narrative?

General Motors Company GM | 76.42 75.80 | -0.40% -0.81% Pre |

- In recent months, General Motors has paused production and temporarily laid off about 1,300 workers at its Factory Zero EV plant while simultaneously ramping up heavy-duty Silverado and Sierra truck output in Flint to a six-day schedule, responding to softer U.S. EV demand, strong gas-powered pickup demand, and evolving tariff and policy conditions.

- At the same time, GM has maintained leadership in overall U.S. auto sales and the No. 2 position in EVs, while growing high-margin subscription revenue and expanding Cadillac EV volumes, highlighting a business model increasingly balanced between traditional trucks, electrified vehicles, and software-based services.

- We’ll now examine how GM’s decision to cut EV production while expanding heavy-duty truck output may alter its investment narrative and risk balance.

Find 59 companies with promising cash flow potential yet trading below their fair value.

General Motors Investment Narrative Recap

To own GM, you need to believe it can balance slower EV adoption with profitable trucks, growing software subscriptions, and disciplined capital allocation. The latest step was a new US$2,000 million 364 day revolving credit line for GM Financial, which modestly reinforces liquidity rather than changing the near term story, where the key catalyst is execution on mixed EV and truck production, and the biggest risk is policy driven EV demand and tariff pressure.

That new 364 day facility, earmarked for GM Financial and backed by liquidity covenants of at least US$4,000 million globally and US$2,000 million in the U.S., underpins the balance sheet as GM pivots production toward high demand heavy duty pickups while tempering EV capacity. It sits alongside growing high margin subscription revenue and GM’s leading North American truck franchise, which many investors view as central to funding ongoing EV and software investments.

Yet behind GM’s strong truck margins and growing subscriptions, investors should be aware that...

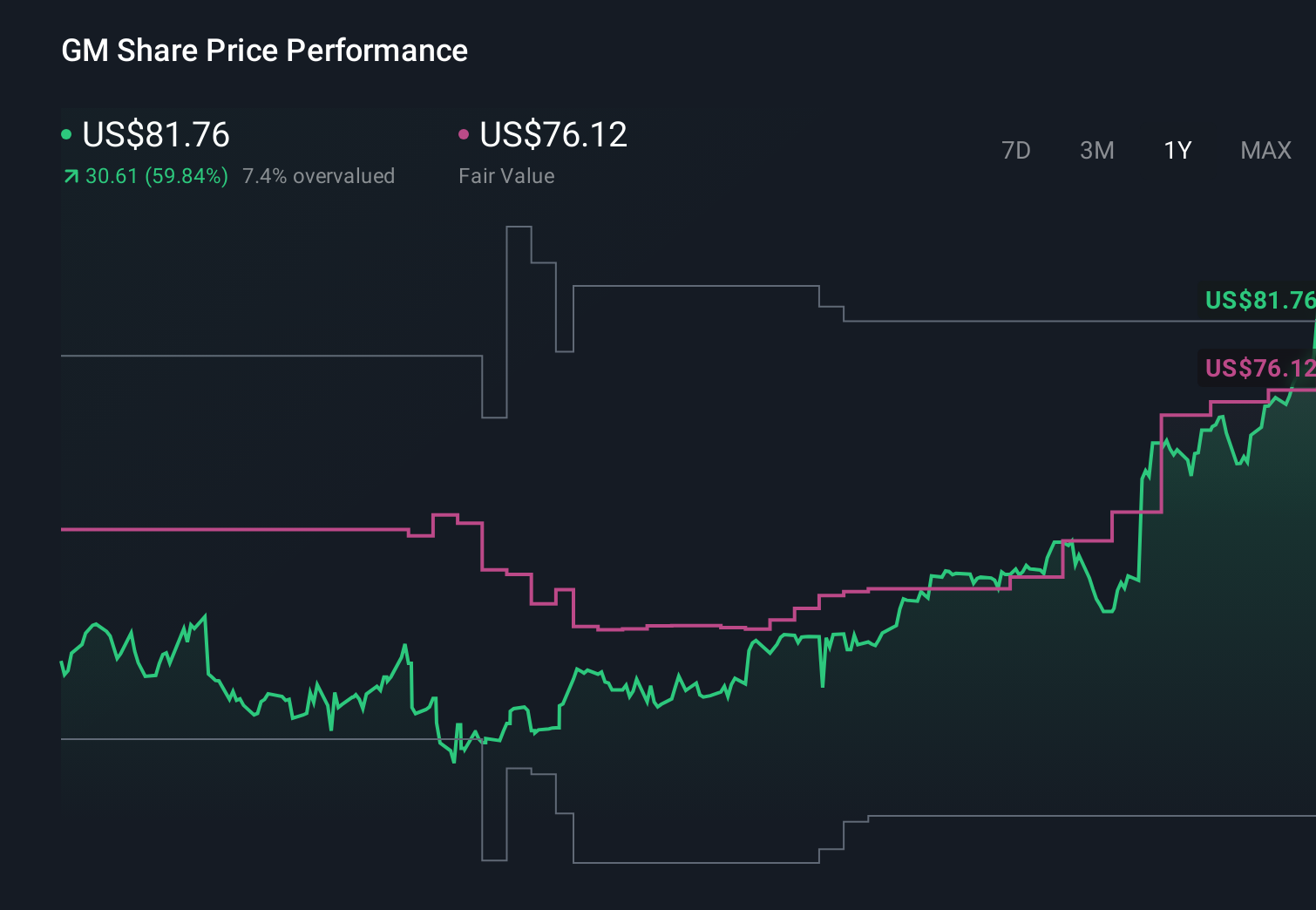

General Motors' narrative projects $185.3 billion in revenue and $8.0 billion in earnings by 2028. This assumes a 0.4% yearly revenue decline and an earnings increase of about $1.5 billion from $6.5 billion today.

Uncover how General Motors' forecasts yield a $79.46 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting GM to reach about US$192.5 billion in revenue and US$12.8 billion in earnings, but this shift toward trucks over EVs could either support that margin focused view or expose how dependent those forecasts are on high truck profitability and successful EV cost reduction, so you should weigh how differently you might see the same risks and opportunities.

Explore 7 other fair value estimates on General Motors - why the stock might be worth 8% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Motors research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free General Motors research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Motors' overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.