Will Increased Medicare Advantage Rates Reshape Humana's (HUM) Long-Term Growth Narrative?

Humana Inc. HUM | 177.83 181.00 | +0.50% +1.78% Post |

- Recent coverage highlights that the U.S. health insurance sector, particularly HMOs like Humana, is expected to benefit from increased commercial plan enrollment and higher Medicare Advantage rates, despite ongoing medical cost pressures and regulatory uncertainty.

- Commentators point to Humana's efforts to expand through new platforms and acquisitions, which may help counter industry challenges and support long-term growth in Medicare Advantage.

- We'll examine how growing commercial plan opportunities may shape Humana's investment narrative and the company's outlook on future revenue streams.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Humana Investment Narrative Recap

To be a shareholder in Humana, you need to believe in the long-term prospects of private health insurers, especially as commercial and Medicare Advantage enrollment grows. The latest sector news supports this outlook, though for Humana, the immediate catalyst remains Medicare Advantage rate stability, while the risk of unpredictable medical costs continues to weigh on near-term earnings. The news does not materially alter these fundamental drivers.

Among recent announcements, Humana's new partnerships with Vori Health, HOPCo, and TailorCare are particularly relevant. These ventures focus on improving care coordination and outcomes for Medicare Advantage members, aligning directly with industry trends favoring value-based care and potentially reinforcing one of Humana's most important growth engines in this segment.

However, it’s important for investors to keep in mind that, despite promising growth vectors, ongoing litigation relating to future Medicare Advantage Star ratings remains unresolved and could...

Humana's narrative projects $150.9 billion revenue and $3.3 billion earnings by 2028. This requires 7.0% yearly revenue growth and a $1.7 billion increase in earnings from $1.6 billion today.

Uncover how Humana's forecasts yield a $298.95 fair value, a 18% upside to its current price.

Exploring Other Perspectives

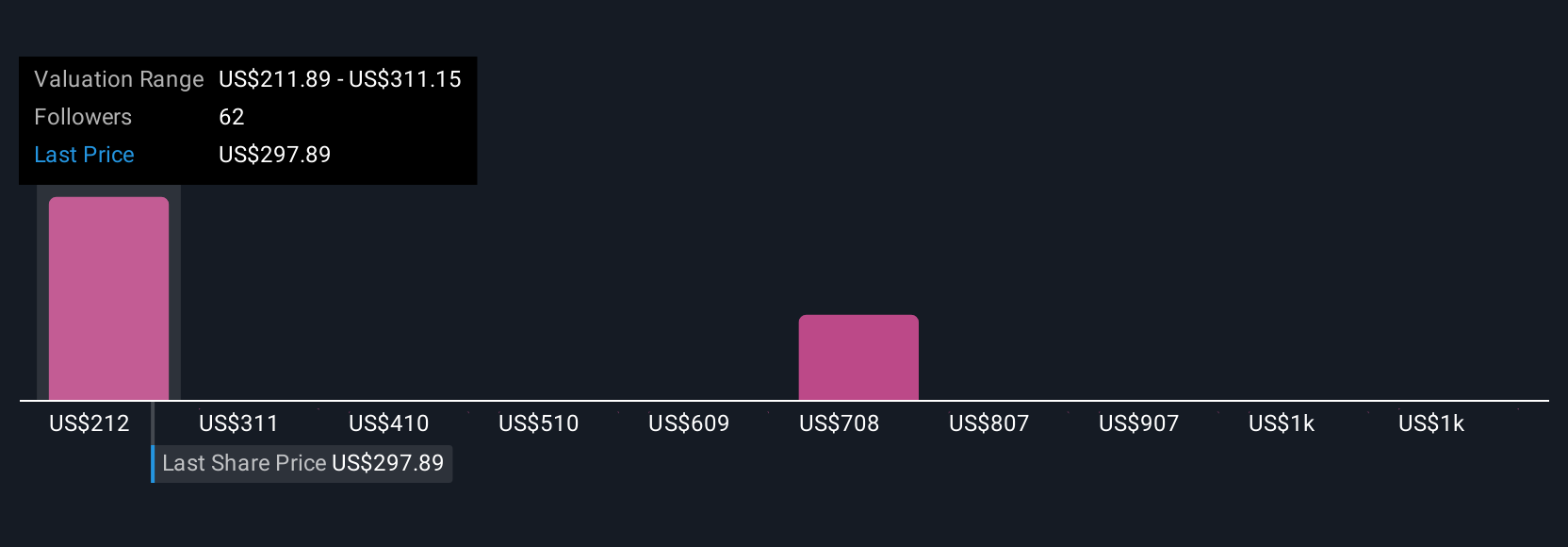

The Simply Wall St Community includes 11 fair value estimates for Humana, ranging from US$211.89 to US$1,204.45 per share, showing widely varied outlooks. Several members see commercial and Medicare Advantage opportunities as key, yet regulatory uncertainty could shape long-term outcomes in ways that current fair values do not capture.

Explore 11 other fair value estimates on Humana - why the stock might be worth 16% less than the current price!

Build Your Own Humana Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Humana research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Humana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Humana's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.