Will Ingersoll Rand’s (IR) Q1 Results and Buybacks Shift Its Growth‑Versus‑Returns Narrative?

Ingersoll Rand Inc. IR | 0.00 |

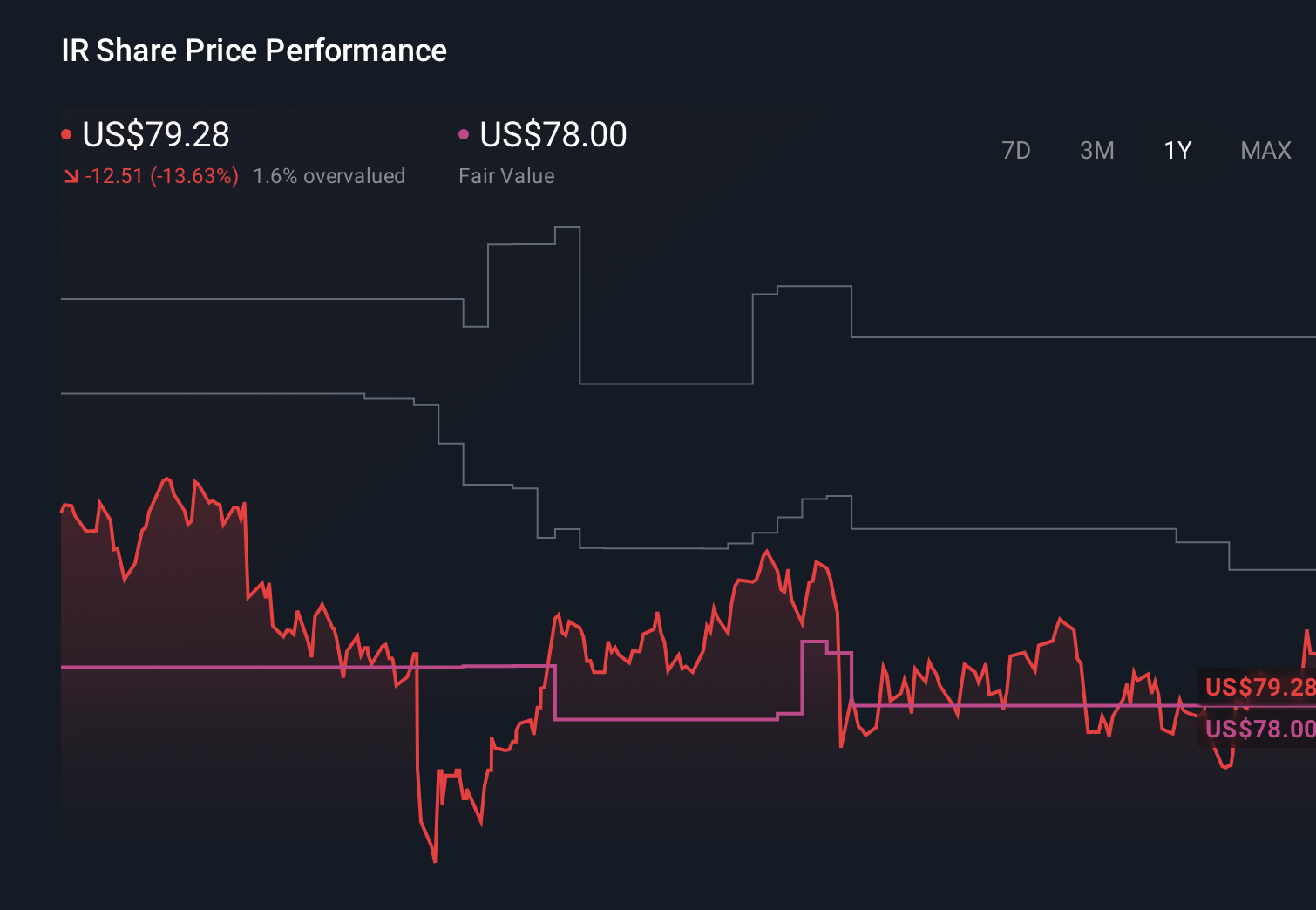

- Ingersoll Rand Inc. recently reported past first-quarter 2026 results with sales of US$1,847.2 million and net income of US$192.1 million, while maintaining its full-year 2026 revenue growth guidance of 2.5% to 4.5%.

- Over the same period, the company completed a large multi-year share repurchase effort and reiterated a focus on bolt-on acquisitions, highlighting an ongoing balance between shareholder returns and growth investments.

- Next, we’ll examine how Ingersoll Rand’s reaffirmed 2026 outlook and continued buybacks may influence its existing investment narrative and risk profile.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to believe in its role supplying mission-critical, energy-efficient equipment and services, with growth increasingly supported by aftermarket revenue and disciplined bolt-on M&A. The reaffirmed 2026 revenue outlook and continued buybacks do not appear to change the key near term catalyst, which is execution on margin and earnings quality after recent one off charges, nor the main risk around integration and returns from future acquisitions in a mixed macro backdrop.

The most relevant update is the completion of the multi year buyback program, which has retired 6.44% of shares for about US$1,847.96 million. Combined with a low regular dividend and ongoing M&A focus, this reinforces a capital allocation mix that leans on both earnings growth and per share support as potential drivers of returns, while still leaving investors exposed to the risk that new acquisitions may not deliver the expected benefits.

Yet investors should be aware that the real concern may be how any future acquisition stumble could affect margins and long term returns...

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029. This requires 5.0% yearly revenue growth and an earnings increase of about $813 million from $587.0 million today.

Uncover how Ingersoll Rand's forecasts yield a $96.47 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$8.8 billion and earnings US$1.5 billion by 2028, so if bolt-on deals or new markets underperform after this latest M&A-focused commentary, that more upbeat story could look very different, and it is worth comparing these views before you decide what you believe.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 24% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.