Will JPMorgan’s (JPM) Leadership Shake-Up and $50 Billion Buyback Shift Its Investment Narrative?

Jpmorgan Chase JPM | 0.00 |

- In late June 2026, JPMorgan Chase & Co. named Doug Petno and Troy Rohrbaugh co-presidents, reshuffled key business leadership as Marianne Lake announced her retirement, lifted its planned quarterly dividend to US$1.65 per share, and authorized a new US$50.00 billion share repurchase program after clearing the Federal Reserve’s stress test.

- These moves simultaneously clarify the bank’s CEO succession path and signal confidence in its capital strength and cash generation, as management commits to larger, ongoing capital returns to shareholders.

- We’ll now examine how JPMorgan’s decision to pair a higher dividend with a US$50.00 billion buyback may influence its investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

JPMorgan Chase Investment Narrative Recap

To own JPMorgan Chase, you need to believe its diversified banking, payments and wealth engines can offset regulatory, technology and competition pressures. The latest leadership reshuffle and capital return announcements do not fundamentally change that near term. The key short term catalyst remains management’s ability to keep fee and payments growth resilient, while the biggest risk is still mounting regulatory and capital demands that could restrict how flexibly JPMorgan deploys its balance sheet.

The new US$1.65 quarterly dividend and fresh US$50.00 billion buyback authorization, following the Fed stress test, are the most directly relevant developments. They underline that regulators currently view JPMorgan’s capital position as solid, which matters if you care about continued buybacks supporting per share metrics. At the same time, larger distributions increase the importance of how the bank manages future capital rules and any shifts in earnings from more cyclical businesses.

Yet beneath this confidence in capital strength, investors should be aware of how tighter rules and higher tech spending could still squeeze returns over time...

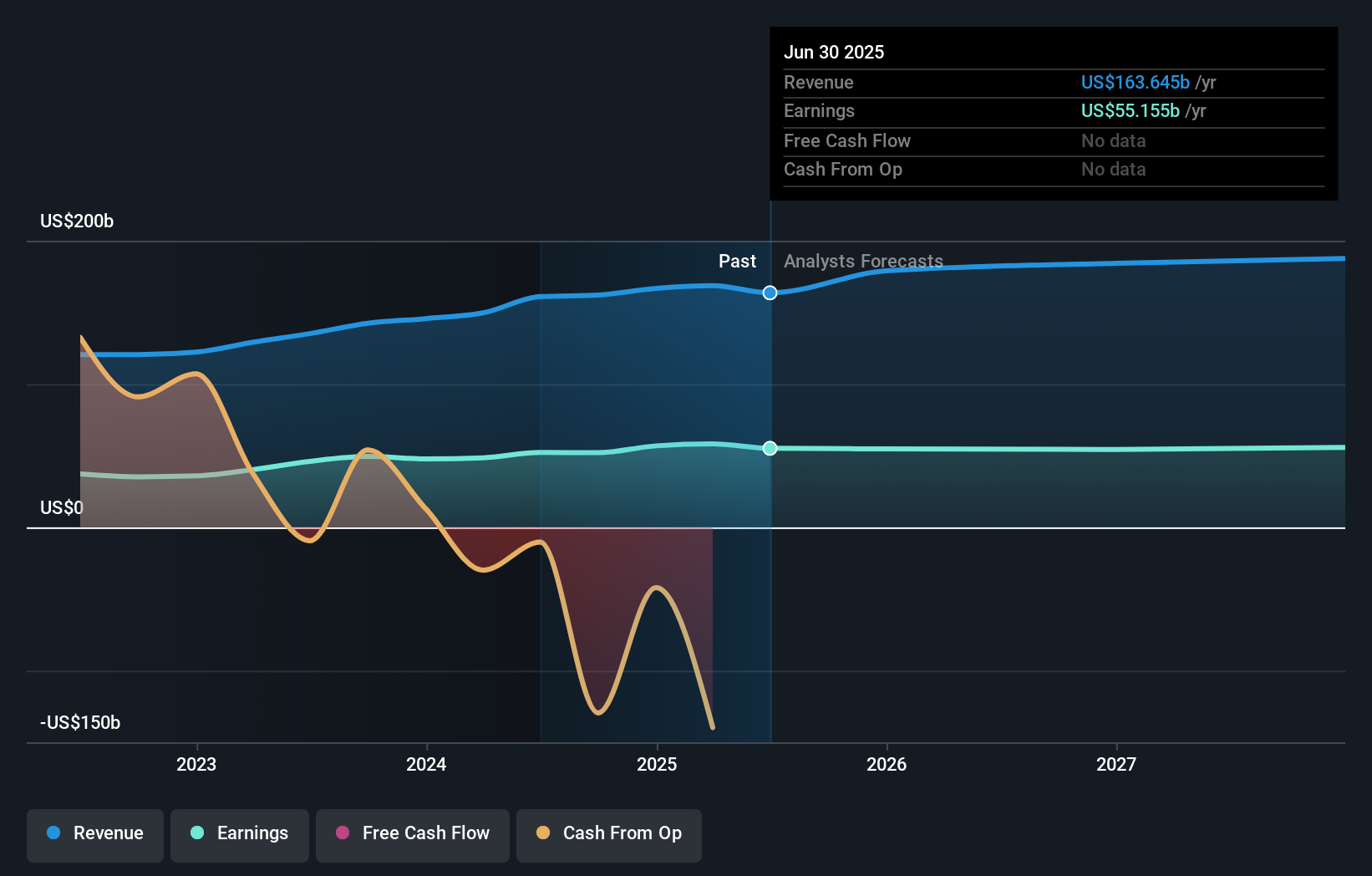

JPMorgan Chase's narrative projects $209.8 billion revenue and $63.3 billion earnings by 2029. This requires 7.6% yearly revenue growth and about a $7.6 billion earnings increase from $55.7 billion today.

Uncover how JPMorgan Chase's forecasts yield a $337.75 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected JPMorgan to lift earnings from about US$57.5 billion to nearly US$69.8 billion, and see AI and private credit as margin boosters, so this latest capital return news could either reinforce that optimism or force you to question whether those expectations fully reflect the regulatory and tech cost risks you are now watching unfold.

Explore 19 other fair value estimates on JPMorgan Chase - why the stock might be worth as much as 30% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your JPMorgan Chase research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free JPMorgan Chase research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate JPMorgan Chase's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.