Will Life Time’s Sale-Leasebacks and Resort Club Expansion Shift Life Time Group Holdings’ (LTH) Narrative?

Life Time Group Holdings, Inc. LTH | 0.00 |

- Life Time Group Holdings has recently closed US$200 million of sale-leaseback transactions on five owned properties and opened several large-format, resort-style athletic country clubs in Phoenix and Winter Park, Orlando, while planning further club and residential expansions through 2027.

- This combination of real estate monetization and capital-intensive growth in affluent, mixed-use developments highlights how Life Time is reshaping its balance sheet while doubling down on its premium wellness ecosystem.

- Next, we'll examine how using sale-leasebacks to target positive free cash flow may influence Life Time's existing investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Life Time Group Holdings Investment Narrative Recap

To own Life Time, you have to believe its premium, in-person wellness ecosystem can justify ongoing heavy investment in large clubs while supporting healthier cash generation. The US$200 million in sale leasebacks and new openings in Phoenix and Orlando feed the core growth story, but they also sharpen the key near term tension: using real estate transactions to target positive free cash flow while keeping balance sheet risk and rent obligations in check.

The most relevant recent announcement is Life Time’s plan for up to US$400 million of sale leaseback proceeds in 2026, paired with an expectation of positive free cash flow while still growing its owned real estate portfolio. For investors focused on catalysts, this matters because it directly ties the funding of new destination clubs to the same financing tool that could become a pressure point if capital markets or real estate valuations change.

But while the expansion headlines are appealing, investors should also be aware of how reliant this model has become on sale leasebacks and...

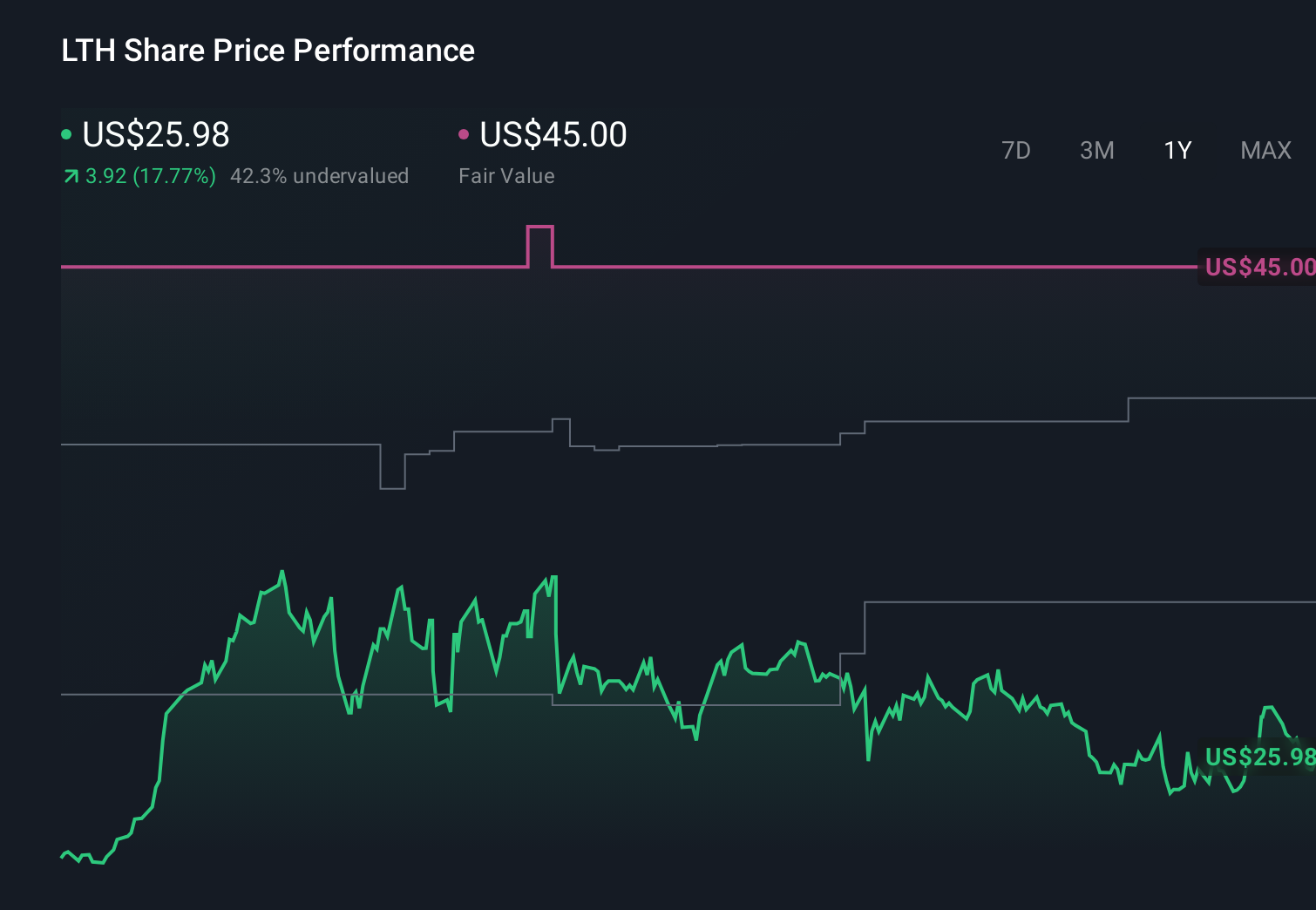

Life Time Group Holdings' narrative projects $4.1 billion revenue and $448.6 million earnings by 2029. This requires 10.8% yearly revenue growth and about a $74.9 million earnings increase from $373.7 million today.

Uncover how Life Time Group Holdings' forecasts yield a $40.00 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already assuming revenue of about US$4.0 billion and only modest earnings growth by 2029, so compared with the more optimistic narrative around club openings and sale leasebacks, they paint a far more cautious picture of how much expansion and digital add ons might really deliver, reminding you that equally informed people can read the same numbers very differently and that both views may evolve after this latest news.

Explore 3 other fair value estimates on Life Time Group Holdings - why the stock might be worth as much as 69% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.