Will Lowering Supermajority Thresholds Reshape Avista's (AVA) Governance Balance Between Management and Shareholders?

Avista Corporation AVA | 41.88 | +1.13% |

- In early April 2026, Avista Corporation proposed amending its Restated Articles of Incorporation to lower the shareholder approval threshold for certain matters from 80% of outstanding common shares to a simple majority.

- This shift toward a lower voting hurdle could reshape how quickly and easily major corporate decisions are authorized, potentially changing the balance of influence between management and shareholders.

- Next, we’ll examine how this move toward majority-based approvals interacts with Avista’s existing investment narrative and risk profile.

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

Avista Investment Narrative Recap

To own Avista, you generally need to be comfortable with a regulated utility focused on the Pacific Northwest, with steady but modest earnings growth and meaningful exposure to regional regulatory and weather risks. The proposed shift from an 80% supermajority to simple-majority approvals looks more like a governance clean‑up than a swing factor for near term earnings, so it does not materially change the key catalyst or the biggest current risk.

Among recent announcements, the most relevant context is Avista’s 2025 earnings, with revenue of US$1,964 million and net income of US$193 million, which frame the company’s capacity to fund its large capital program. Those same grid modernization, renewable integration, and wildfire mitigation investments remain a central catalyst for long term reliability and earnings potential, but they also heighten the risk of balance sheet strain if regulators do not allow timely recovery of rising costs.

Yet behind these governance changes, investors should be aware of how rising capital needs could interact with already pressured free cash flows and...

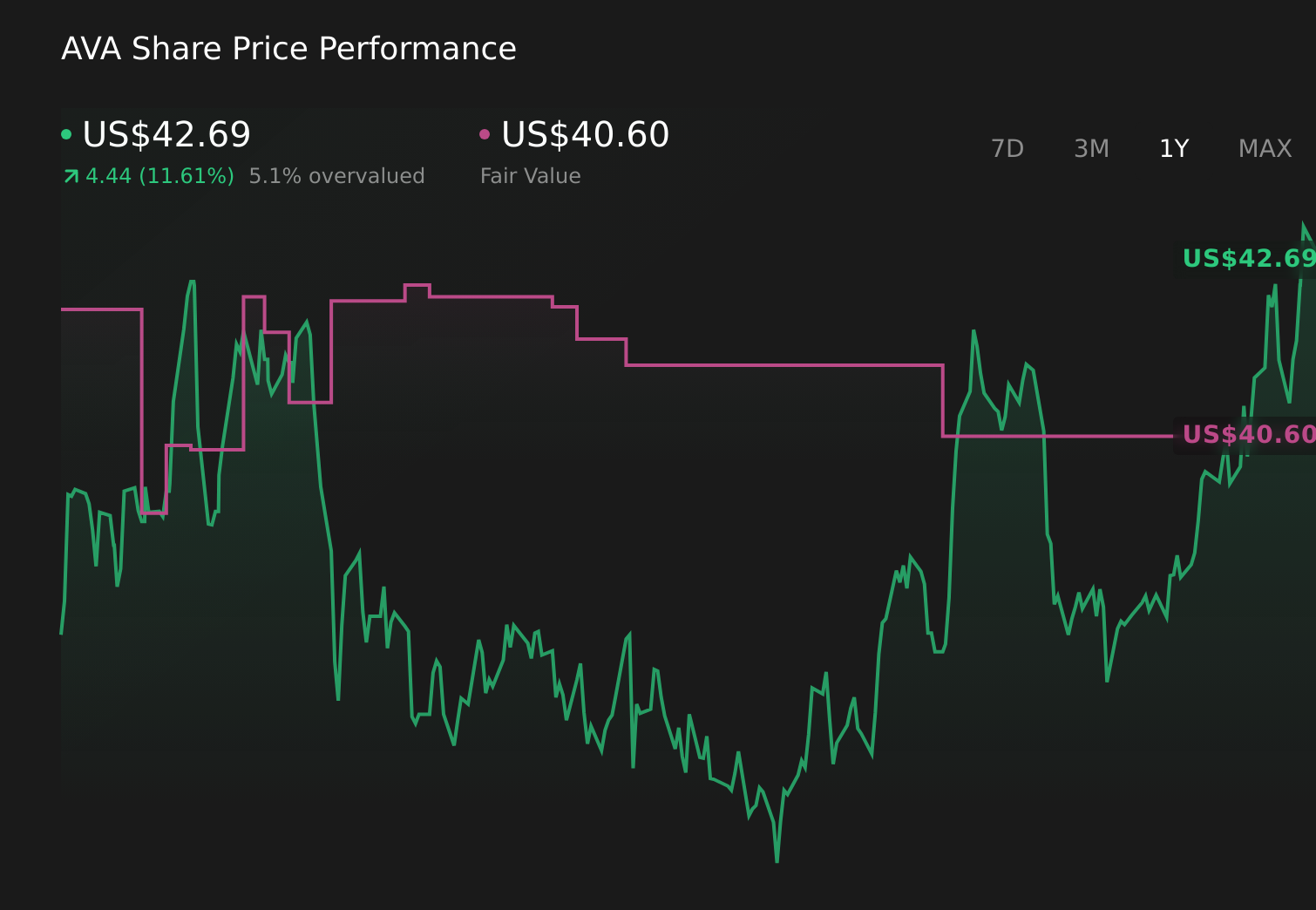

Avista's narrative projects $2.1 billion revenue and $245.2 million earnings by 2028. This requires 3.1% yearly revenue growth and a $66.2 million earnings increase from $179.0 million today.

Uncover how Avista's forecasts yield a $40.33 fair value, in line with its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$36.73 to US$40.33 per share, showing how differently individual investors assess Avista’s prospects. You can weigh these views against the company’s growing capital expenditure and regulatory recovery risk, and decide which assumptions about future performance feel more realistic to you.

Explore 2 other fair value estimates on Avista - why the stock might be worth 11% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Avista research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 26 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.