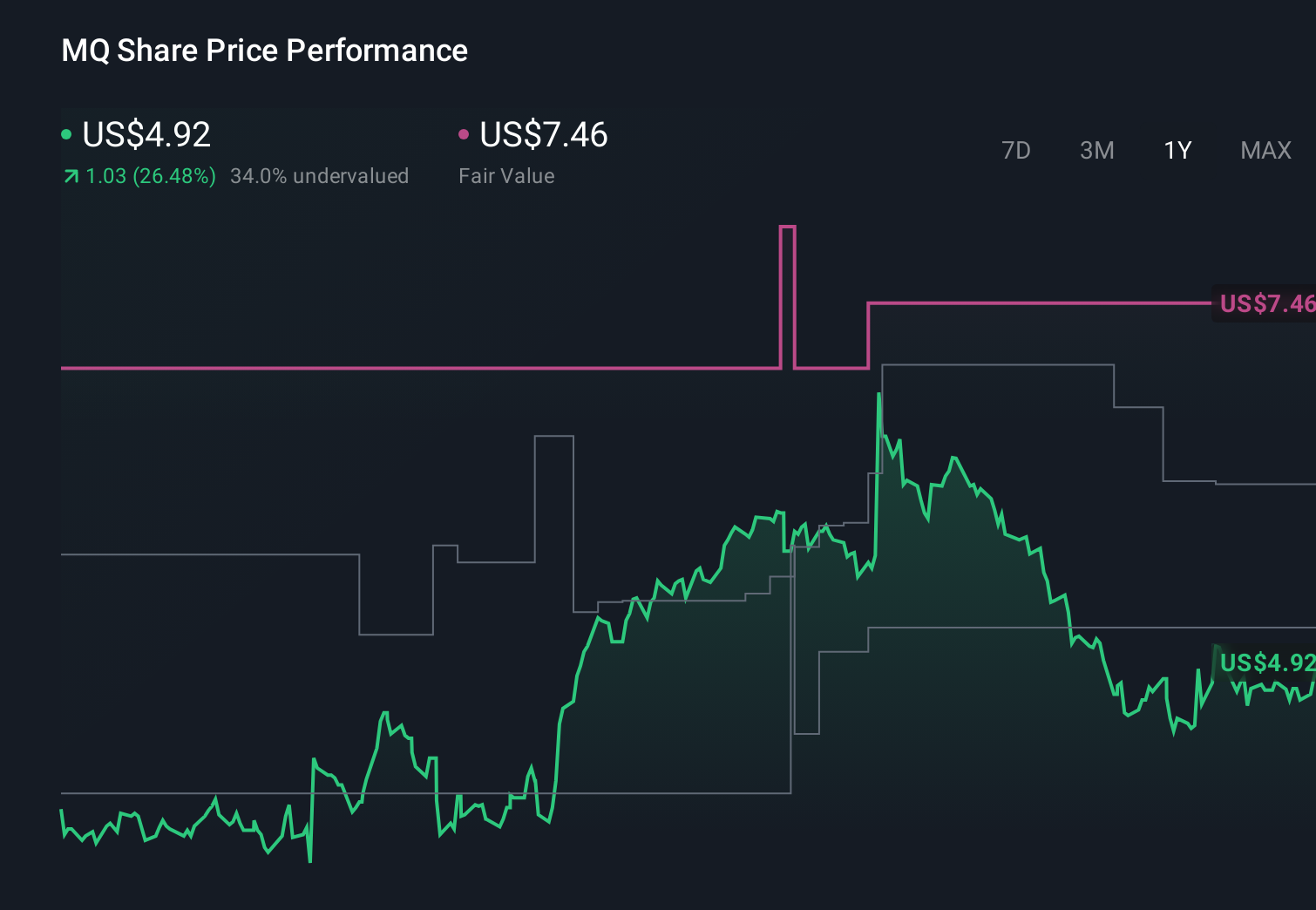

Will Marqeta’s (MQ) Banking Circle Deal and EU Expansion Redefine Its Embedded Finance Narrative?

Marqeta, Inc. MQ | 0.00 |

- In May 2026, Marqeta announced it had expanded its account and money movement tools into 30 additional European countries through a collaboration with Luxembourg-licensed bank Banking Circle, building on its prior TransactPay acquisition and regional regulatory framework alignment.

- This move deepens Marqeta’s embedded finance capabilities in Europe by combining multi-currency virtual accounts, faster payments, and SEPA rail access under a unified, compliant program management offering.

- Next, we will examine how this expanded European money movement footprint, enabled by Banking Circle, may influence Marqeta’s existing investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Marqeta Investment Narrative Recap

To own Marqeta, you have to believe its card issuing and embedded finance platform can convert higher payment volumes into durable, profitable revenue, despite customer concentration and pricing pressure. The Banking Circle expansion strengthens its European narrative, but the most important near term catalyst still looks like translating recent revenue growth into consistent, higher margin profitability, while the biggest risk remains reliance on a handful of large clients whose decisions could quickly alter that path.

Among recent developments, the enhancement of Marqeta’s Real Time Decisioning with AI driven risk scoring is especially relevant. As Marqeta extends money movement across Europe, fraud management and smarter authorization become more central to its value proposition, potentially reinforcing its ability to win and keep embedded finance customers. If this risk suite deepens client relationships at scale, it could support the same profitability and margin inflection that investors are watching most closely.

However, investors should also be aware that if a major customer recalibrates its relationship with Marqeta, the impact on revenue concentration risk could...

Marqeta's narrative projects $969.0 million revenue and $73.1 million earnings by 2029.

Uncover how Marqeta's forecasts yield a $5.19 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected Marqeta to reach about US$1.0 billion in revenue and US$194.5 million in earnings by 2028, so this European expansion could either reinforce that bullish view of harmonized North America Europe growth or prompt a rethink of how much client concentration and rising competition might still cap the upside.

Explore 4 other fair value estimates on Marqeta - why the stock might be worth just $3.70!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.