Will MasTec’s (MTZ) Strong Q4 Beat and Higher EBITDA Guidance Recast Its Growth-Risk Narrative

MasTec, Inc. MTZ | 0.00 |

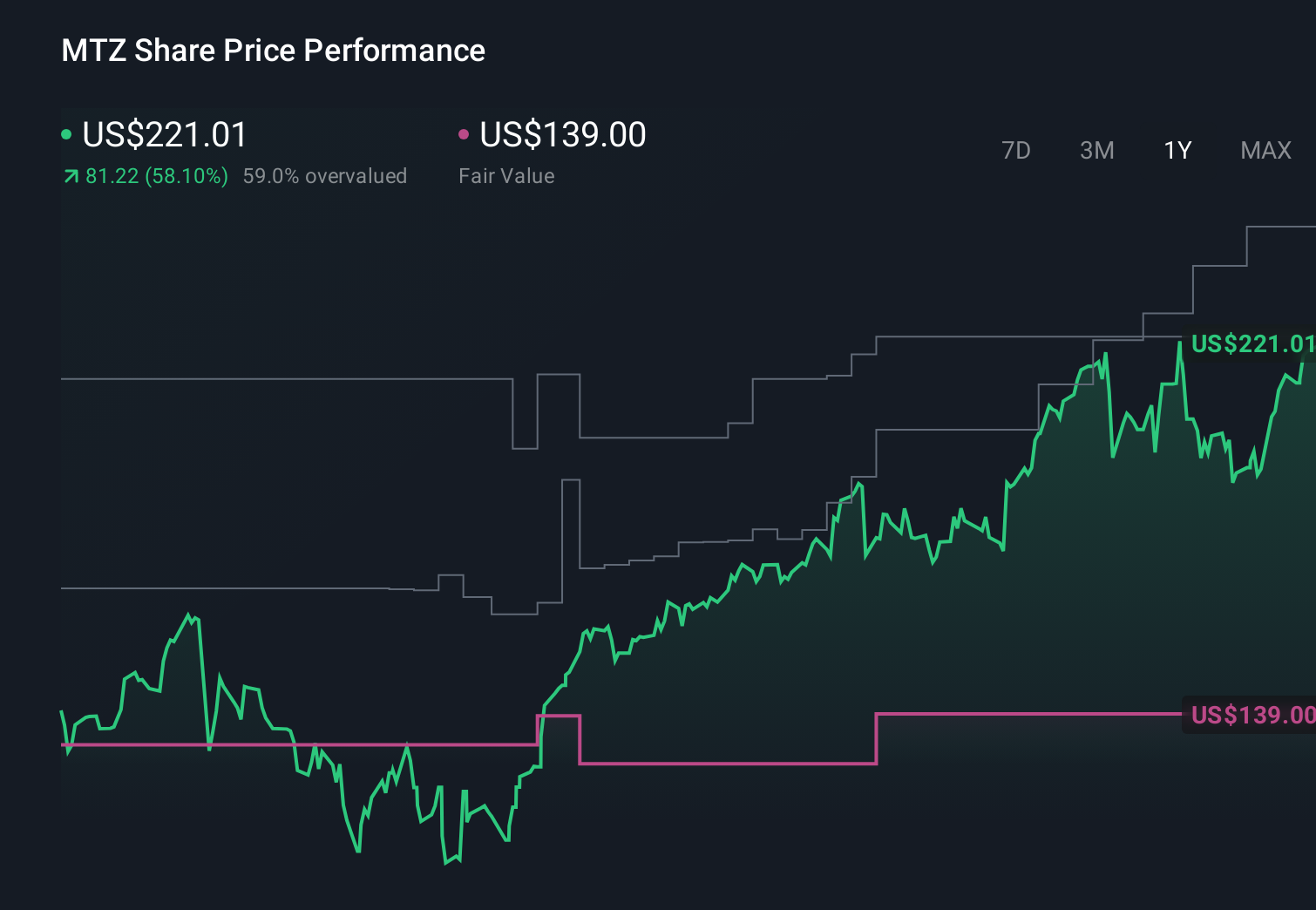

- MasTec recently reported a strong past Q4, with revenue rising 15.8% year on year and beating analyst expectations by 5.9%, alongside EBITDA guidance for the next quarter that also came in ahead of forecasts.

- The combination of this outperformance with relatively weaker full-year guidance versus peers highlights investors' focus on MasTec's near-term execution rather than its longer-horizon targets.

- We’ll now examine how MasTec’s better-than-expected EBITDA guidance could reshape its existing investment narrative around growth, margins, and risk.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

MasTec Investment Narrative Recap

To own MasTec, you need to believe that large scale energy, power, and communications projects will keep filling its backlog and that management can convert this work into healthier margins without overreaching on costs. The latest Q4 beat and stronger near term EBITDA guidance support that execution story and appear to be the key short term catalyst, while the biggest risk remains that MasTec’s recent build out of people and equipment proves too heavy if project timing slips.

The most relevant recent announcement here is MasTec’s updated 2026 guidance, which targets full year revenue of about US$17,000 million and GAAP net income of about US$566 million. This outlook frames the stronger near term EBITDA guidance in a broader context, reminding investors that even with a strong quarter, the path to improving margins and earnings across a record backlog still depends on consistent project delivery and disciplined use of that expanded workforce and equipment base.

Yet behind the strong quarter, investors should still be aware of how quickly higher fixed costs could hurt margins if...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$22,700 million and earnings about US$1,100 million by 2029, which is a much more bullish outlook than the baseline view that highlights project execution and cost risks, and this latest earnings beat could either reinforce that optimism or prompt you to reconsider how wide the range of possibilities really is.

Explore 6 other fair value estimates on MasTec - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MasTec research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.