Will New Director Joseph Kim and US$1 Billion Buyback Authorization Change Quanta Services' (PWR) Narrative

Quanta Services, Inc. PWR | 0.00 |

- In May 2026, Quanta Services, Inc. appointed Sunoco GP LLC CEO Joseph Kim to its Board of Directors and authorized a US$1.00 billion share repurchase program, while directors reported several routine equity compensation settlements into common stock.

- This combination of fresh supply chain and logistics expertise on the board and increased capital return commitments adds an extra dimension to Quanta’s already infrastructure-focused business profile.

- We’ll now examine how the new US$1.00 billion buyback authorization may influence Quanta’s existing investment narrative and risk-reward profile.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Quanta Services Investment Narrative Recap

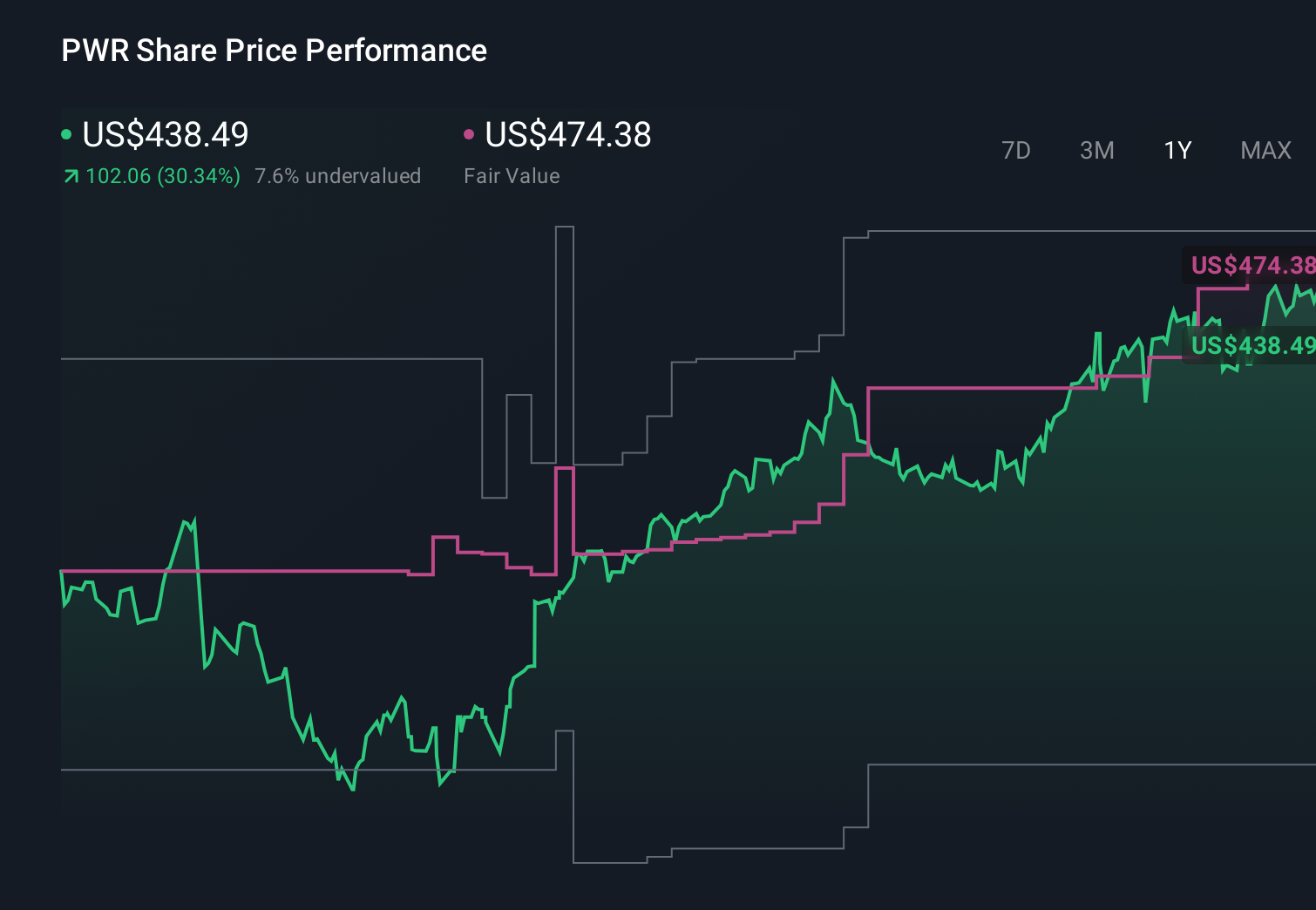

To own Quanta Services today, you have to believe in a long runway of utility, grid and data center infrastructure work that supports its record backlog and cash generation. The key near term catalyst remains execution on large, complex transmission and data center related projects, while the biggest risk is that any slowdown or disruption in these utility and data center capex plans could weaken backlog quality. The new US$1.00 billion buyback and Joseph Kim’s appointment do not materially change those fundamentals.

The most relevant recent announcement alongside the buyback is Quanta’s raised 2026 guidance, with revenues now expected between US$34.7 billion and US$35.2 billion and net income between US$1.40 billion and US$1.50 billion. Together with the repurchase authorization and ongoing dividend, this frames a capital return story that depends heavily on Quanta continuing to convert its infrastructure exposure and record remaining performance obligations into consistent earnings and free cash flow.

Yet investors should also be aware that project delays, regulatory shifts or changes in utility spending priorities could...

Quanta Services' narrative projects $46.6 billion revenue and $2.4 billion earnings by 2029. This requires 15.7% yearly revenue growth and approximately a $1.3 billion earnings increase from $1.1 billion today.

Uncover how Quanta Services' forecasts yield a $761.35 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Quanta could reach about US$49.2 billion of revenue and US$3.3 billion of earnings by 2029, which is far more upbeat than consensus; the new buyback and board appointment might strengthen that view or expose how dependent it is on continued grid and data center spending.

Explore 6 other fair value estimates on Quanta Services - why the stock might be worth 40% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Quanta Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Quanta Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quanta Services' overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.