Will Power Integrations’ (POWI) GaN Breakthrough Deepen Its Competitive Moat in AI Data Centers?

Power Integrations, Inc. POWI | 0.00 |

- At the 2025 OCP Global Summit, Power Integrations published a white paper outlining the performance benefits of its PowiGaN™ gallium-nitride technology for 800 VDC power in next-generation AI data centers, highlighting its collaboration with NVIDIA to accelerate the adoption of these new power architectures.

- A distinctive feature is Power Integrations’ introduction of a 1250 V PowiGaN switch capable of supporting up to 1000 VC input voltage, offering over 90.3% system efficiency in liquid-cooled, fan-less data center designs.

- We'll examine how Power Integrations' rollout of high-voltage PowiGaN technology for AI data centers may reshape its investment outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Power Integrations Investment Narrative Recap

To be a shareholder in Power Integrations, you need confidence in the company’s ability to move beyond cyclical consumer appliance markets and gain meaningful traction in high-growth segments like AI data centers. The recent announcement of its 1250 V PowiGaN switch at the OCP Global Summit, along with expanded collaboration with NVIDIA, has the potential to reinforce the company’s positioning as an innovation leader, but is unlikely to change the importance of securing major customer wins or approval to accelerate adoption, the dominant short-term catalyst, and also the biggest risk if not achieved. Among recent company announcements, the debut of new 1700 V InnoSwitch™ ICs for automotive applications earlier this year stands out. This highlights the broad approach Power Integrations is taking to diversify into segments where cutting-edge power conversion is essential, reinforcing ongoing efforts to reduce dependence on cyclical end-markets and capture higher-margin opportunities tied to secular demand. In contrast, investors should also recognize the persistent headwinds from tariff exposure and global trade risks...

Power Integrations' narrative projects $634.3 million revenue and $96.7 million earnings by 2028. This requires 12.8% yearly revenue growth and a $63.1 million earnings increase from $33.6 million today.

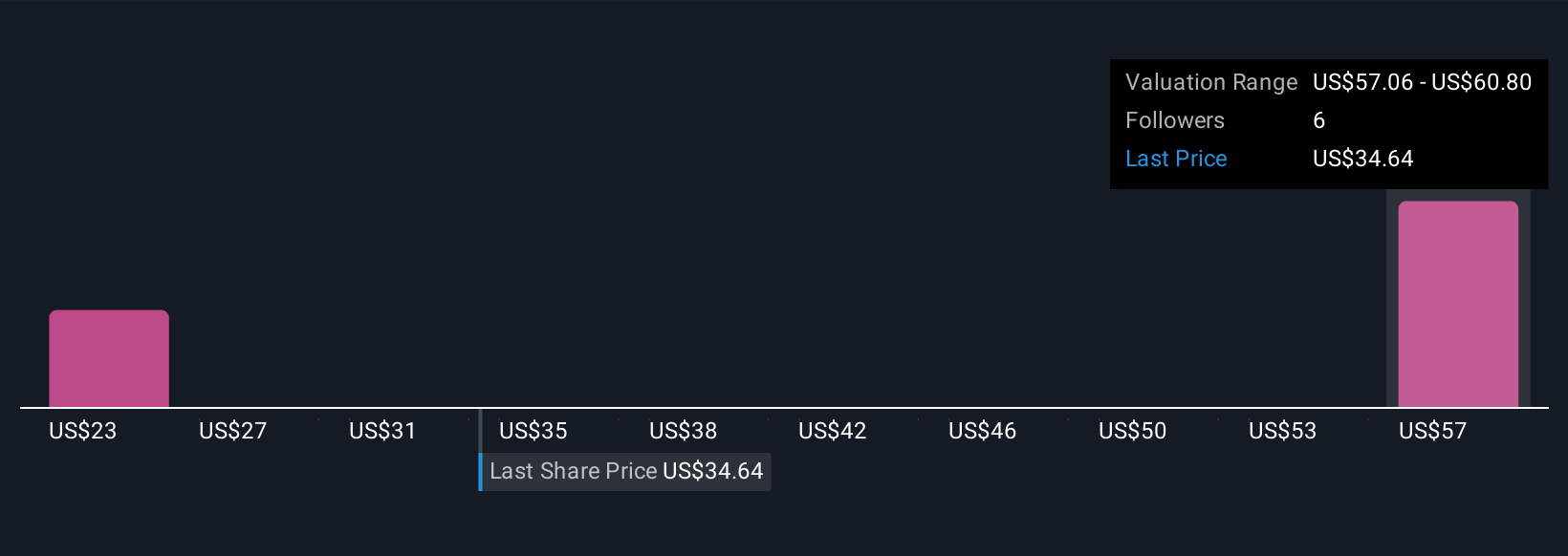

Uncover how Power Integrations' forecasts yield a $60.80 fair value, a 41% upside to its current price.

Exploring Other Perspectives

Private fair value estimates from three Simply Wall St Community members range from US$23.54 to US$60.80 per share. While views vary, many are watching whether design wins with critical customers materialize as a potential turning point for growth.

Explore 3 other fair value estimates on Power Integrations - why the stock might be worth 45% less than the current price!

Build Your Own Power Integrations Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Power Integrations research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Power Integrations research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Power Integrations' overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.