Will Renewed Institutional Buying After Share Weakness Shift MercadoLibre’s (MELI) Fintech-Led Growth Narrative?

MercadoLibre, Inc. MELI | 0.00 |

- In the first quarter, Fisher Funds Management and Sara-Bay Financial increased their positions in MercadoLibre, together adding nearly 37,000 shares worth over US$71 million, following earlier share price weakness but in the context of strong recent revenue growth and fintech expansion.

- This renewed interest from institutional investors underlines confidence in MercadoLibre’s efforts such as lowering free shipping thresholds in Brazil to attract more buyers, boost purchase frequency, and grow market share, even at the cost of some near-term margin pressure.

- We’ll now explore how this institutional buying, backed by confidence in MercadoLibre’s fintech and e-commerce expansion, may influence its investment narrative.

Find 60 companies with promising cash flow potential yet trading below their fair value.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you need to believe its e-commerce and fintech ecosystem in Latin America can keep scaling while managing rising credit, logistics, and margin pressures. The recent institutional buying signals renewed confidence but does not materially change the key near term catalyst, which remains user and revenue growth from commerce and fintech, or the biggest risk, which is credit and margin strain from more aggressive shipping, pricing, and lending.

The most relevant recent announcement here is MercadoLibre’s push to lower free shipping thresholds in Brazil, which has been linked to higher buyer acquisition, purchase frequency, and market share gains. This same initiative, however, also feeds directly into today’s main risk: higher fulfillment and shipping costs, which, if not balanced by scale efficiencies and disciplined credit performance, could weigh on net margins and earnings.

Yet behind this growth story, one risk investors should be aware of is how quickly expanding credit in volatile markets could...

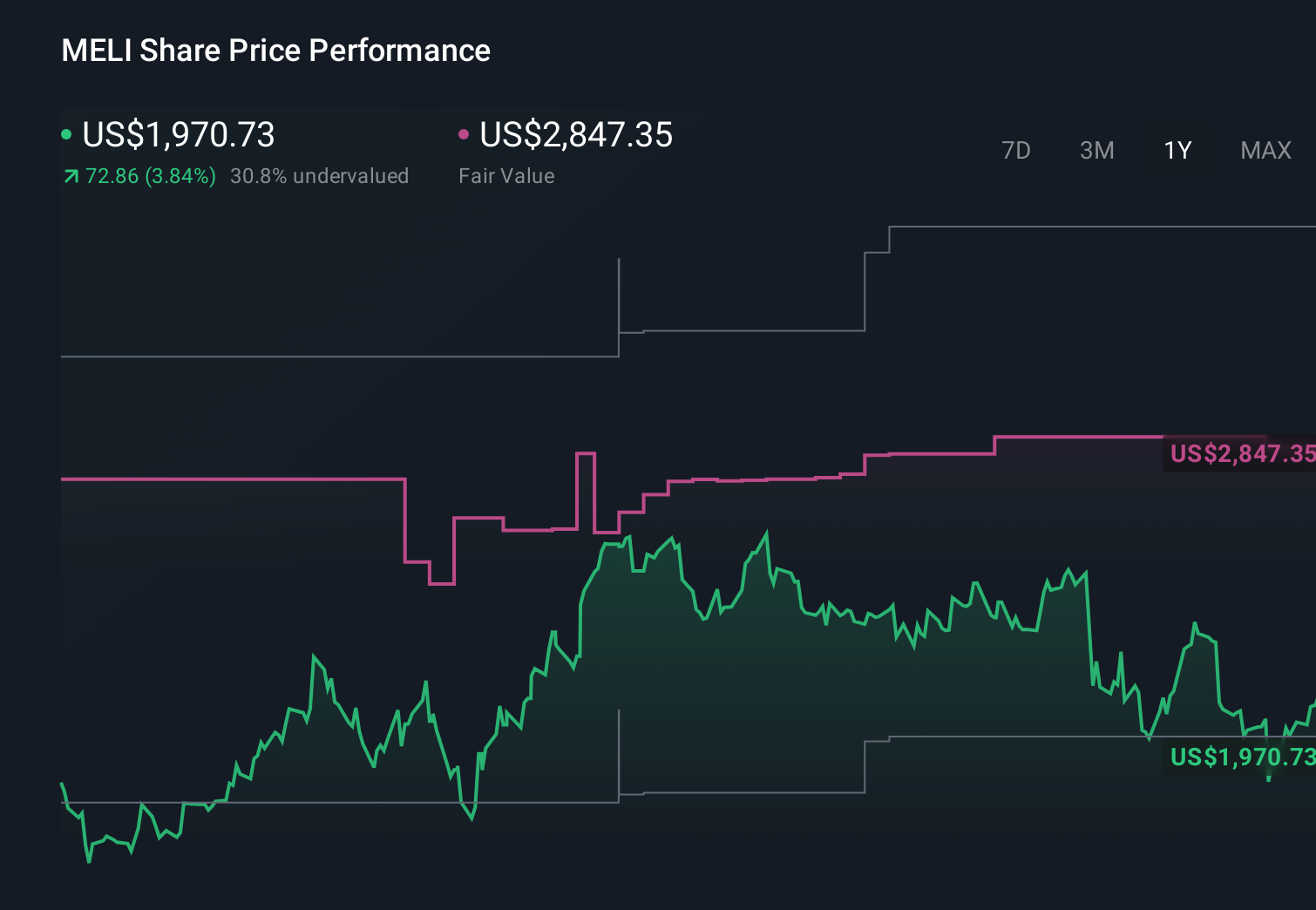

MercadoLibre's narrative projects $46.9 billion revenue and $5.1 billion earnings by 2028. This requires 24.8% yearly revenue growth and an earnings increase of about $3.0 billion from $2.1 billion today.

Uncover how MercadoLibre's forecasts yield a $2640 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in revenue of about US$52.3 billion and earnings of roughly US$5.9 billion before this news, which is a far more bullish view than consensus and assumes credit and logistics investments pay off smoothly; this fresh institutional buying might support that story, or it could end up highlighting how sharply opinions can differ, so it is worth comparing several viewpoints before deciding what you believe.

Explore 28 other fair value estimates on MercadoLibre - why the stock might be worth just $1827!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MercadoLibre research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.