Will SK Hynix’s HBM Re‑Prioritization Shift Change Photronics’ (PLAB) AI Supply Chain Narrative?

Photronics, Inc. PLAB | 0.00 |

- Recently, reports that South Korea's SK Hynix is slowing its high‑bandwidth memory expansion to prioritize higher‑margin conventional DRAM unsettled sentiment across the AI‑chip supply chain, affecting related companies such as Photronics.

- While the shift reflects SK Hynix’s margin focus rather than weaker AI demand, it underscores how sensitive upstream suppliers like Photronics are to changes in memory makers’ capacity decisions and product mix.

- We’ll now examine how concerns about SK Hynix’s HBM slowdown and AI supply chain adjustments could influence Photronics’ existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that its global photomask network and exposure to advanced nodes and displays can turn cyclical swings in chip and panel demand into durable earnings power. The SK Hynix HBM slowdown highlights near term sensitivity to memory makers’ capacity choices, but does not appear to alter Photronics’ key catalyst around new advanced capacity or its main risks tied to capital intensity and customer concentration in Asia in a material way.

Against this backdrop, the recent delivery of Photronics’ most advanced mask writer to its Korea facility stands out, because it directly links to the same display and memory ecosystem that reacted to the SK Hynix news. This upgrade supports the company’s push into higher value AMOLED and Gen 8.6 display photomasks, which remains central to the current investment story even as investors reassess near term AI related demand signals.

But while the SK Hynix headlines may fade, the real issue investors should be watching is the ongoing risk that...

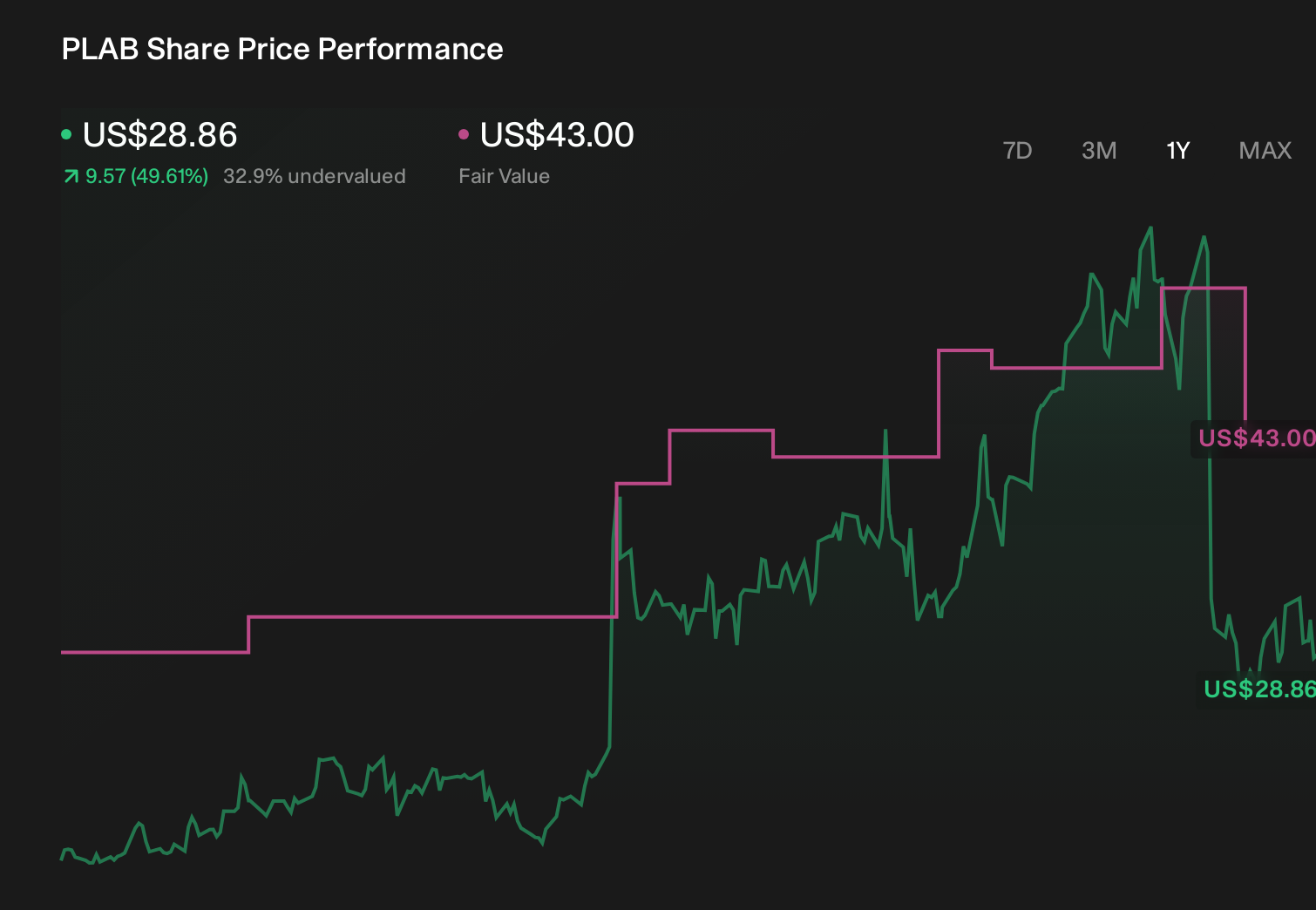

Photronics' narrative projects $930.0 million revenue and $81.2 million earnings by 2029. This requires 2.6% yearly revenue growth and a $77.9 million earnings decrease from $159.1 million today.

Uncover how Photronics' forecasts yield a $43.00 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community place Photronics’ fair value between US$21.74 and US$43.00, showing how far apart individual views can be. Set those opinions against the company’s heavy ongoing capital expenditure commitments, and it becomes clear why you may want to compare several different scenarios for Photronics’ future earnings power before deciding how it might fit in your portfolio.

Explore 5 other fair value estimates on Photronics - why the stock might be worth 34% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 43 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.