Will StandardAero's (SARO) Focus on Organic Growth Define Its Competitive Edge in Aerospace?

StandardAero, Inc. SARO | 26.26 | +0.04% |

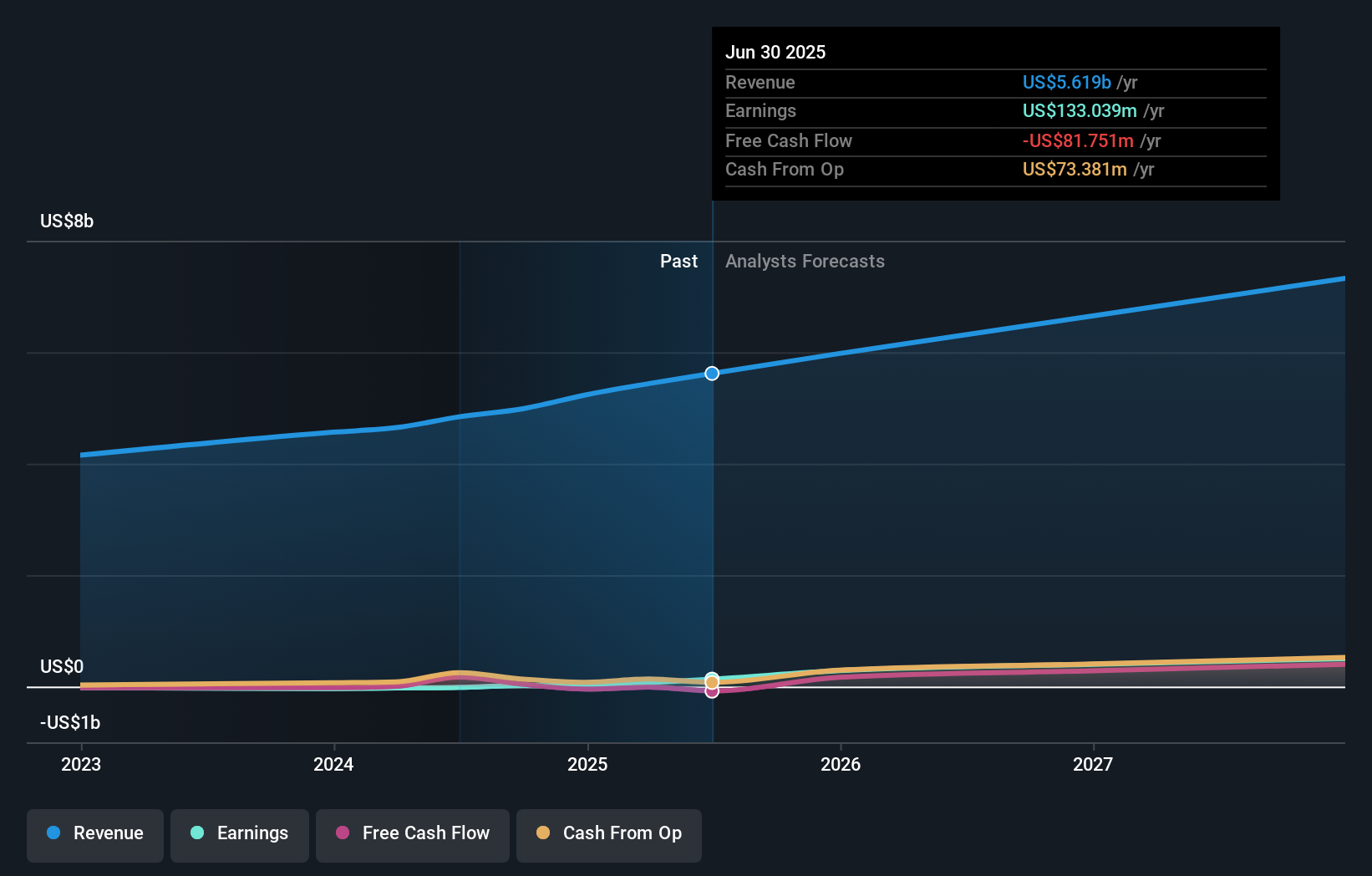

- StandardAero reported strong second quarter 2025 earnings with sales of US$1.53 billion and net income of US$67.71 million, alongside raised full-year revenue guidance to US$5.88–6.03 billion.

- The company also highlighted plans for disciplined capital allocation through both organic investments and potential acquisitions, aiming to grow in areas where it maintains a strong market position.

- We'll explore how StandardAero's expansion in commercial aerospace platforms could impact its investment narrative moving forward.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is StandardAero's Investment Narrative?

For anyone considering a stake in StandardAero, the big picture centers on whether you believe in the company’s ability to translate momentum in commercial aerospace and expansionary investments into stronger financial results, despite current valuation pressures. The recent quarterly earnings and raised guidance mark a positive short-term catalyst, bolstered by the company’s strong pipeline of M&A targets and ongoing organic growth, particularly in its commercial platforms. However, with shares trading at a price-to-earnings ratio well above both peers and industry benchmarks, valuation remains a risk, and the company’s return on equity is still relatively low. The increased focus on acquisitions and platform expansions, highlighted in the latest results call, could accelerate revenue and earnings growth and reshape risk factors, but integrating new buys and maintaining discipline will be crucial. Overall, these new developments may impact how quickly StandardAero can meet lofty growth expectations already priced into its shares.

Yet, integrating acquisitions is not a straightforward win, execution risk is a factor for investors to weigh. Despite retreating, StandardAero's shares might still be trading 10% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Explore 3 other fair value estimates on StandardAero - why the stock might be worth as much as 36% more than the current price!

Build Your Own StandardAero Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your StandardAero research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free StandardAero research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StandardAero's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.