Will Strong Q1 Results, New Financing and Buybacks Change Credit Acceptance's (CACC) Narrative?

Credit Acceptance Corporation CACC | 0.00 |

- In early May 2026, Credit Acceptance Corporation reported first-quarter 2026 results showing revenue of US$580 million and net income of US$135.8 million, alongside a US$450.0 million asset-backed non-recourse financing and completion of a buyback covering 588,925 shares, or 5.44% of its stock.

- The combination of stronger earnings, lower-cost term financing, and meaningful share repurchases points to a company tightening its balance sheet while seeking to enhance per-share profitability and operational focus.

- We’ll now examine how Credit Acceptance’s improved first-quarter profitability and new US$450 million asset-backed financing shape its existing investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 33 companies in the world exploring or producing it. Find the list for free.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you have to believe it can price risk in subprime auto loans well enough to earn a return comfortably above its funding costs, despite competition and credit uncertainty. The latest quarter’s higher earnings, active buybacks, and US$450.0 million ABS financing support that thesis but do not remove the key near term risk around future loan performance and accuracy of cash flow forecasts.

The new US$450.0 million asset backed, non recourse financing looks especially relevant here, because it directly affects how Credit Acceptance funds its loan book and manages interest expense. By using this facility to refinance higher cost debt while keeping dealer relationships intact, the company is trying to protect spreads at a time when any renewed deterioration in 2022 to 2024 vintages could quickly compress margins.

Yet, despite the stronger quarter, investors should still be aware that continued underperformance in recent loan vintages could...

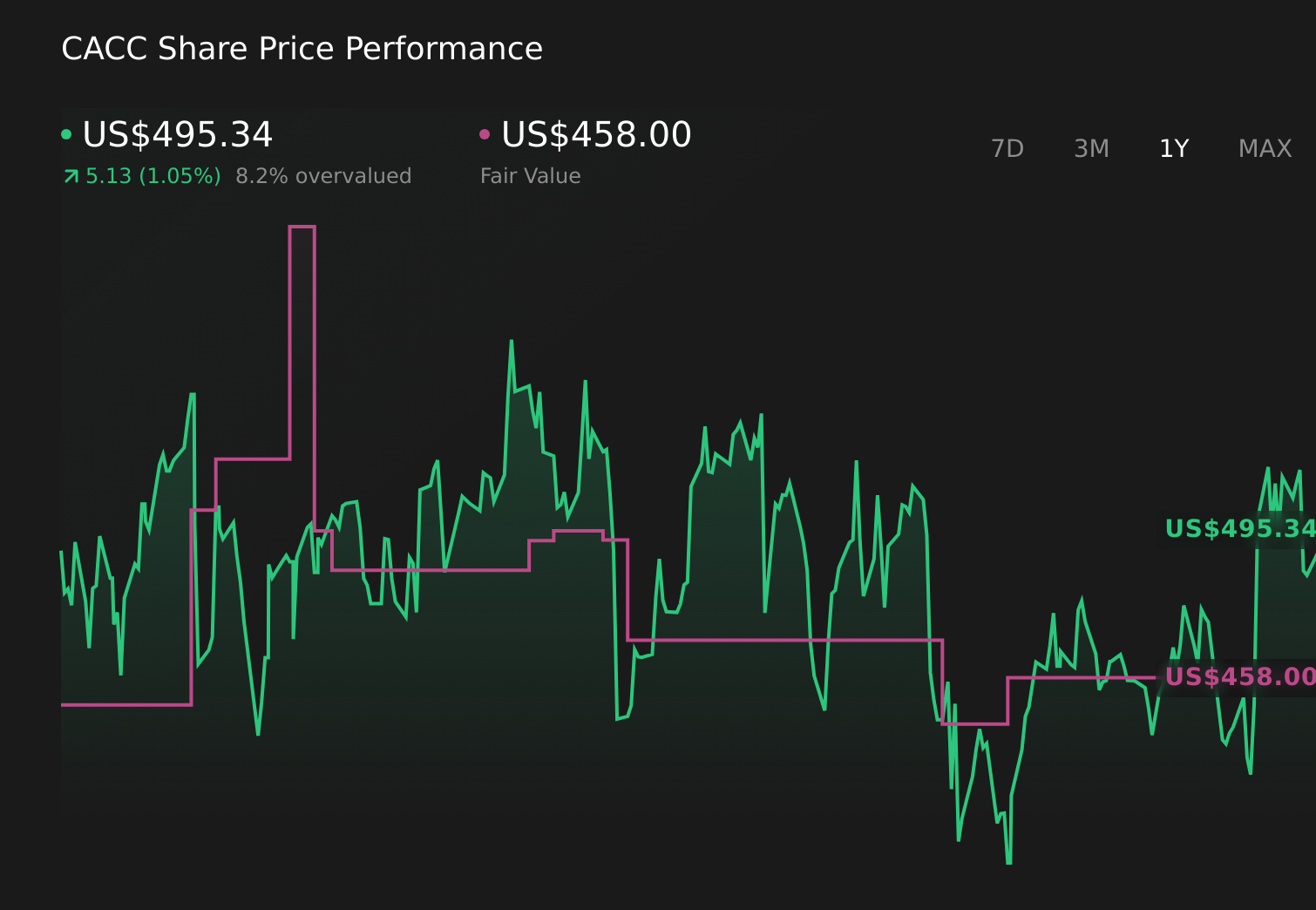

Credit Acceptance's narrative projects $3.3 billion revenue and $659.5 million earnings by 2029.

Uncover how Credit Acceptance's forecasts yield a $481.67 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates for Credit Acceptance span roughly US$335 to US$482 per share, underlining how far private investor views can diverge. When you set those against the ongoing concerns about recent loan vintages and credit performance, it becomes even more important to weigh several independent viewpoints before forming your own expectations for the business.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth 36% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.