Will Walker & Dunlop's (WD) London Expansion Shift Its Edge in European Real Estate Finance?

Walker & Dunlop, Inc. WD | 44.44 | +0.36% |

- Walker & Dunlop, Inc. announced on October 6, 2025, that it expanded its London-based EMEA office by appointing Aaron Knight as senior managing director and co-head of Capital Markets - EMEA, focusing on sourcing debt and equity capital across a variety of European real estate asset classes.

- Knight’s appointment signals Walker & Dunlop’s commitment to strengthening its international capital markets capabilities by leveraging senior-level talent with deep expertise in commercial real estate debt throughout Europe.

- We’ll examine how heightened industry concerns around loan quality, sparked by recent peer disclosures, could alter the investment outlook for Walker & Dunlop.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Walker & Dunlop Investment Narrative Recap

To be a shareholder in Walker & Dunlop, you need to believe that pent-up investment capital, institutional demand, and expansion into global markets, like Europe, will drive long-term growth in loan origination and servicing, even as short-term headline risks emerge. The recent surge in loan quality concerns across the commercial real estate finance sector has heightened uncertainty, but so far the impact on Walker & Dunlop’s business outlook appears limited, with multifamily and international growth seen as key near-term catalysts.

Amid industrywide credit anxieties, Walker & Dunlop’s announcement of its Q3 2025 earnings release date stands out as the most relevant upcoming event for investors focused on near-term catalysts. This update comes just as the company highlights growth in its London-based EMEA office, signaling its commitment to broadening revenue streams beyond its U.S. core, an important lever as industry headwinds intensify.

But in contrast to these expansion efforts, investors should be aware that ongoing volatility in commercial real estate lending trends may...

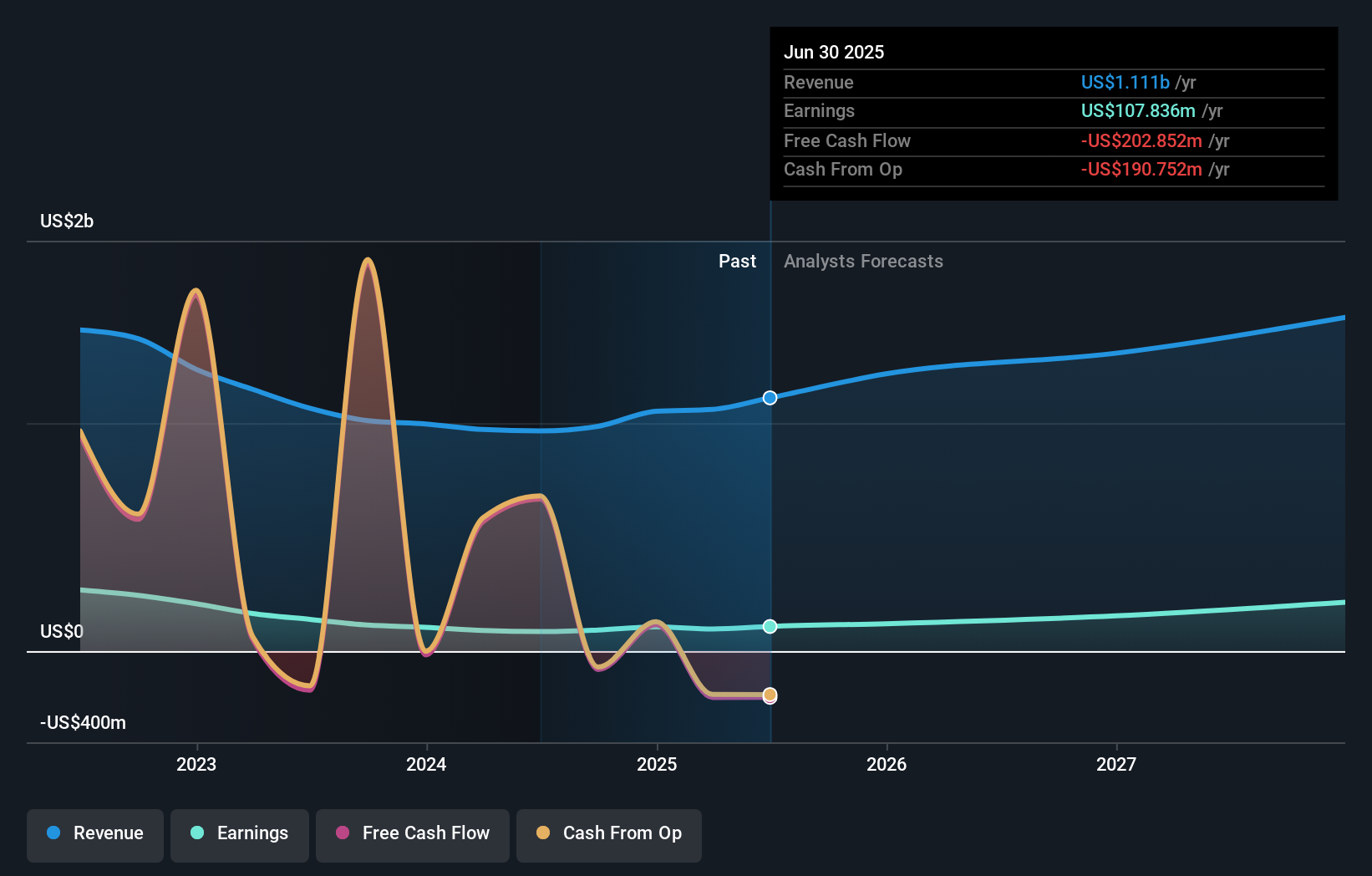

Walker & Dunlop's narrative projects $1.5 billion revenue and $233.2 million earnings by 2028. This requires 11.2% yearly revenue growth and a $125.4 million earnings increase from $107.8 million.

Uncover how Walker & Dunlop's forecasts yield a $92.50 fair value, a 14% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s three fair value estimates for Walker & Dunlop range from US$34.61 to US$92.50 per share, showing a wide variety of individual investor outlooks. With industry loan quality now a central risk, these perspectives reflect sharply different expectations on how market conditions might shape the company’s performance, explore several viewpoints to inform your own.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth less than half the current price!

Build Your Own Walker & Dunlop Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.