Williams Companies Growth Projects And Partnership Shift Valuation And Dividend Picture

Williams Companies, Inc. WMB | 70.86 70.86 | +0.14% 0.00% Post |

- Williams Companies (NYSE:WMB) has completed a series of major pipeline and offshore projects and formed a new partnership with Woodside Energy.

- The company has launched ten new initiatives across pipeline transmission, gathering, storage, and power-related projects.

- Williams has sold its Haynesville E&P business and outlined substantial new growth capital commitments.

- The company has also announced a 5% dividend increase alongside its latest expansion plans.

For investors watching NYSE:WMB, this cluster of moves comes as the stock trades around $72.28, with returns of 8.0% over the past week, 19.1% over the past month, and 18.8% year to date. Over the past year the stock is up 31.2%, and over three and five years the gains have been very large, including a 164.1% return over three years and a 308.4% return over five years.

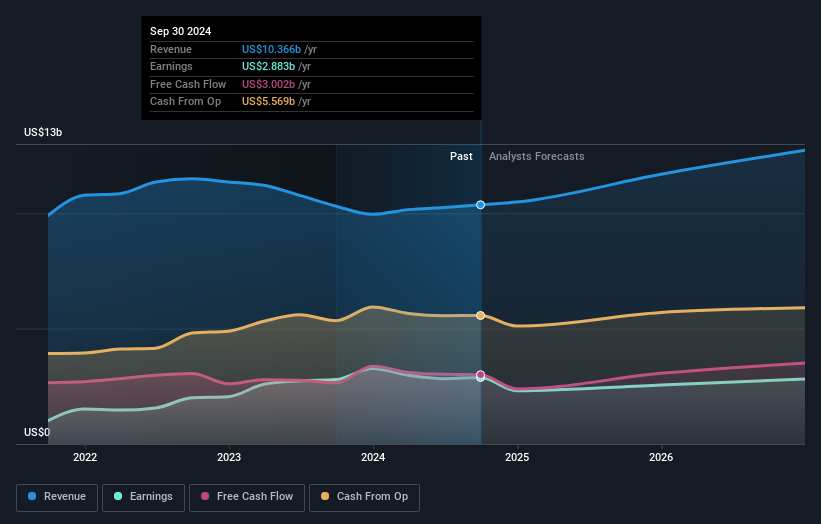

The recent project completions, fresh capital spending plans, and new partnership with Woodside Energy indicate a period where execution on growth projects may matter more for investors than routine quarterly results. As these ten new initiatives move from announcement to construction and operation, the mix of assets Williams owns and the cash flows they generate could become quite different from today.

Stay updated on the most important news stories for Williams Companies by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Williams Companies.

Investor Checklist

Quick Assessment

- ⚖️ Price vs Analyst Target: At $72.28, the share price is about 2% below the US$73.80 analyst target, which sits comfortably inside a US$60 to US$84 range.

- ✅ Simply Wall St Valuation: Shares are described as trading roughly 25.5% below an estimated fair value, which suggests a discount to that model.

- ✅ Recent Momentum: A 19.1% 30 day return points to strong recent momentum as these projects and partnerships have been announced.

There is only one way to know the right time to buy, sell or hold Williams Companies. Head to Simply Wall St's company report for the latest analysis of Williams Companies's Fair Value.

Key Considerations

- 📊 The completion of multiple projects and a new partnership means the asset base and earnings mix could shift as new infrastructure ramps up.

- 📊 Watch how the new capital commitments translate into returns, especially given the current P/E of about 33.8 versus an industry average near 14.2.

- ⚠️ A key flag is that the 2.91% dividend is reported as not well covered by earnings or free cash flow, which matters as spending on growth increases.

Dig Deeper

For the full picture including more risks and rewards, check out the complete Williams Companies analysis. Alternatively, you can check out the community page for Williams Companies to see how other investors believe this latest news will impact the company's narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.