Williams Companies (WMB) Could Be 3% Undervalued On Its Backlog Driven Growth Story

Williams Companies, Inc. WMB | 0.00 |

Williams Companies (WMB) stock drew fresh attention after a recent move that left its year-to-date total return at 27.4%, compared with a 5.4% gain over the past 3 months.

With the latest share price at $77.53, Williams Companies has seen momentum build recently, with a 7 day share price return of 6.03% and a year to date share price return of 27.41%. The 5 year total shareholder return of 263.79% highlights how longer term holders have been rewarded compared with more recent movers.

If you are comparing Williams Companies with other energy infrastructure opportunities, it can be useful to see what is happening across the wider power and grid space through the 34 power grid technology and infrastructure stocks

With Williams Companies posting solid recent returns, a low value score of 2 and an intrinsic value estimate pointing to a sizeable discount, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 3.2% Undervalued

Compared with the latest Williams Companies share price of $77.53, the most followed narrative points to a fair value of about $80.07, implying only a modest gap and putting the focus firmly on the underlying drivers rather than a big valuation mismatch.

The company's robust, fully contracted project backlog (extending beyond 2030), disciplined layering of short and long-cycle projects, and committed capital plan are driving upward revisions to EBITDA and AFFO guidance, indicating future earnings and dividend visibility that may not be fully reflected in current valuation.

Curious what is sitting behind that backlog story? The narrative leans heavily on compounded revenue growth, expanding margins and a punchy profit multiple a decade out. The mix and timing of those assumptions matter more than the small discount on offer.

Result: Fair Value of $80.07 (UNDERVALUED)

However, the Williams Companies narrative could be tested if decarbonization policies curb long term gas demand, or if permitting setbacks delay high spend pipeline projects.

Another View on Williams Companies Valuation

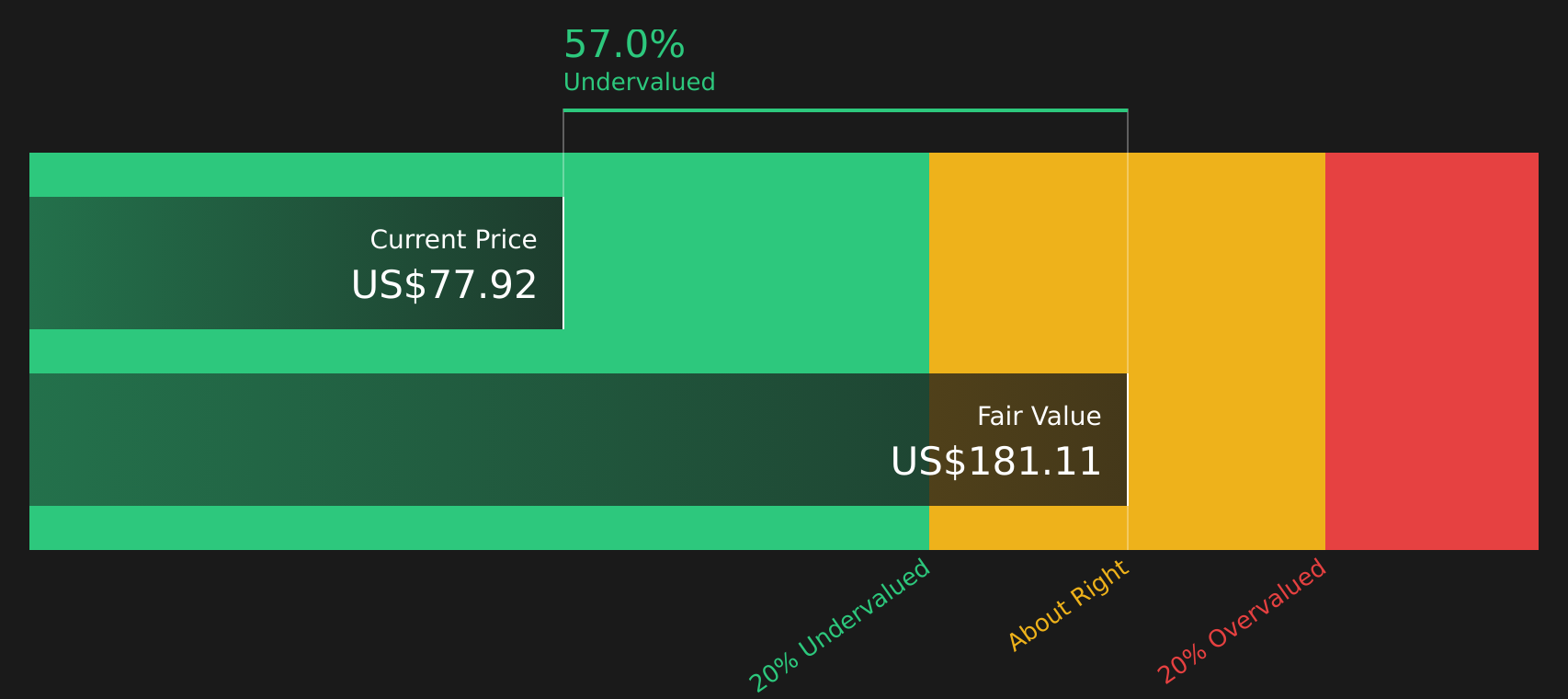

The analyst narrative treats Williams Companies as modestly undervalued at a fair value of about $80.07, yet our DCF model points to a much higher future cash flow value of $181.11. That is a very wide gap, which raises a simple question: which set of assumptions do you trust more?

Next Steps

Reading mixed signals on Williams Companies, with both risks and rewards on the table, is common, so move quickly to review the underlying data and weigh up the 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Williams Companies?

If Williams Companies has you thinking more broadly about your portfolio, this is the moment to widen your search and line up your next potential ideas.

- Target dependable cash flow by scanning for income opportunities through the 9 dividend fortresses that could complement a core holding like Williams Companies.

- Hunt for mispriced quality by checking the 43 high quality undervalued stocks and see which stocks currently pair solid fundamentals with attractive pricing.

- Prioritize resilience by reviewing the 67 resilient stocks with low risk scores so you do not miss companies that may help steady your overall portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.