Williams-Sonoma (WSM) Stock Could Be 11% Below Fair Value After Dividend Affirmation

Williams-Sonoma, Inc. WSM | 0.00 |

Williams-Sonoma (WSM) is back in focus after affirming a quarterly dividend of $0.76 per share, payable on August 21, 2026. This move highlights its ongoing capital return approach.

The latest dividend affirmation comes as Williams-Sonoma’s share price trades at $226.92, with a 30-day share price return of 17.88% and a 1-year total shareholder return of 44.95%, suggesting momentum has been building alongside ongoing buybacks and capital returns.

If this mix of income and strong past total shareholder returns has your attention, it could be a good moment to widen your search with the 20 top founder-led companies

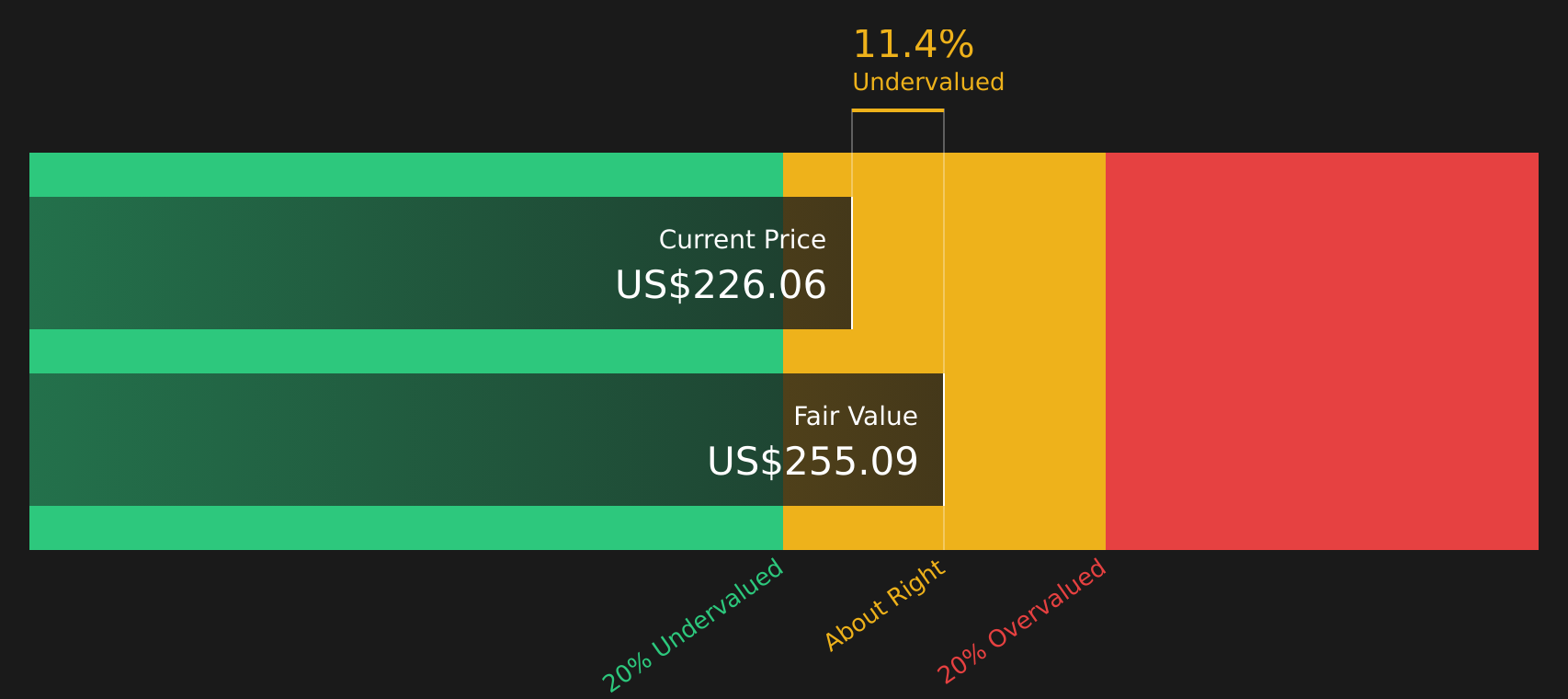

With Williams-Sonoma delivering solid capital returns and trading at an intrinsic value estimate that implies an 11% discount, you have to ask: is there still an entry point here, or is the stock already pricing in future growth?

Most Popular Narrative: 10% Overvalued

Against Williams-Sonoma’s last close at $226.92, the most widely followed narrative fair value of $207.00 points to a premium that investors should understand before reacting to the dividend news.

Continued investment and advances in AI-powered tools and digital platforms are driving higher conversion rates, improved customer experience, and measurable productivity gains, supporting both revenue growth and expanded operating leverage at the margin level. Successful focus on product innovation, exclusive partnerships, and expanding high-quality, differentiated merchandise is resonating across both core and emerging brands, enabling Williams-Sonoma to capture greater share from more affluent, urban, and younger consumers, a demographic that supports premium positioning and long-term revenue expansion.

If you are wondering how that kind of digital and merchandising story supports a higher price, the key lies in a specific growth glide path, steady margins, and a future earnings multiple that assumes Williams-Sonoma keeps converting those efforts into cash over time.

Result: Fair Value of $207.00 (OVERVALUED)

However, there are still clear pressure points, including tariff volatility that could squeeze Williams-Sonoma’s margins and weaker housing activity that may curb demand for big-ticket home furnishings.

Another View: Williams-Sonoma Through a Cash Flow Lens

While the analyst narrative points to a fair value of $207.00, our DCF model points in the opposite direction. On that framework, Williams-Sonoma at $226.92 screens around 11% below an estimated future cash flow value of $255.09. This raises a different question: is the market underestimating the cash generation story?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Williams-Sonoma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Does the mix of dividend income and differing fair value views on Williams-Sonoma leave you curious or confident about where you stand? Take a moment to review the full balance of risks and potential rewards for yourself with the 2 key rewards.

Looking for more investment ideas beyond Williams-Sonoma?

If Williams-Sonoma has sharpened your focus on quality and income, do not stop here. Use targeted screeners to spot other opportunities before they move out of reach.

- Target stronger income potential by reviewing companies in the 8 dividend fortresses.

- Hunt for value by checking stocks that appear mispriced in the 45 high quality undervalued stocks.

- Prioritize resilience by focusing on companies highlighted in the 65 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.