Worthington Steel (WS) Stock Could Be 37% Below Fair Value After Strong Results

Worthington Steel, Inc. WS | 0.00 |

Worthington Steel (WS) is back in focus after reporting quarterly revenue of US$769.80 million and net profit growth of 24.64% year over year, figures that sharply contrast with mixed technical signals.

At a latest share price of US$40.73, Worthington Steel’s 1-day share price return of 3.90% contrasts with a 7-day decline of 6.26%. Its 1-year total shareholder return of 69.30% and 90-day share price return of 24.82% point to momentum that has cooled slightly in the very near term but remains strong over a longer window.

If strong recent results have you thinking about where else growth and pricing power might be emerging, it could be a good time to review 8 top copper producer stocks.

With Worthington Steel trading at US$40.73 against an analyst price target of US$38.00, but with an estimated intrinsic discount of about 37%, the key question is clear: Is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 7.2% Overvalued

Worthington Steel’s narrative fair value of $38.00 sits below the last close at $40.73, which puts extra weight on what is driving that gap.

Worthington Steel is poised to benefit from increased demand in the electrical steel market due to AI initiatives, more data centers, and an anticipated annual power demand growth of more than 6% over the next 15 years, which should lead to higher revenues.

Read the complete narrative. Read the complete narrative.

There is a detailed playbook sitting behind that fair value, tying together revenue growth, margin expansion and future earnings multiples. Curious which assumptions really move the needle on Worthington Steel’s valuation story.

Result: Fair Value of $38 (OVERVALUED)

However, recent declines in shipments across automotive, construction, agriculture and heavy truck markets, along with inventory holding losses and higher SG&A, could pressure the Worthington Steel narrative.

Another View on Worthington Steel’s Valuation

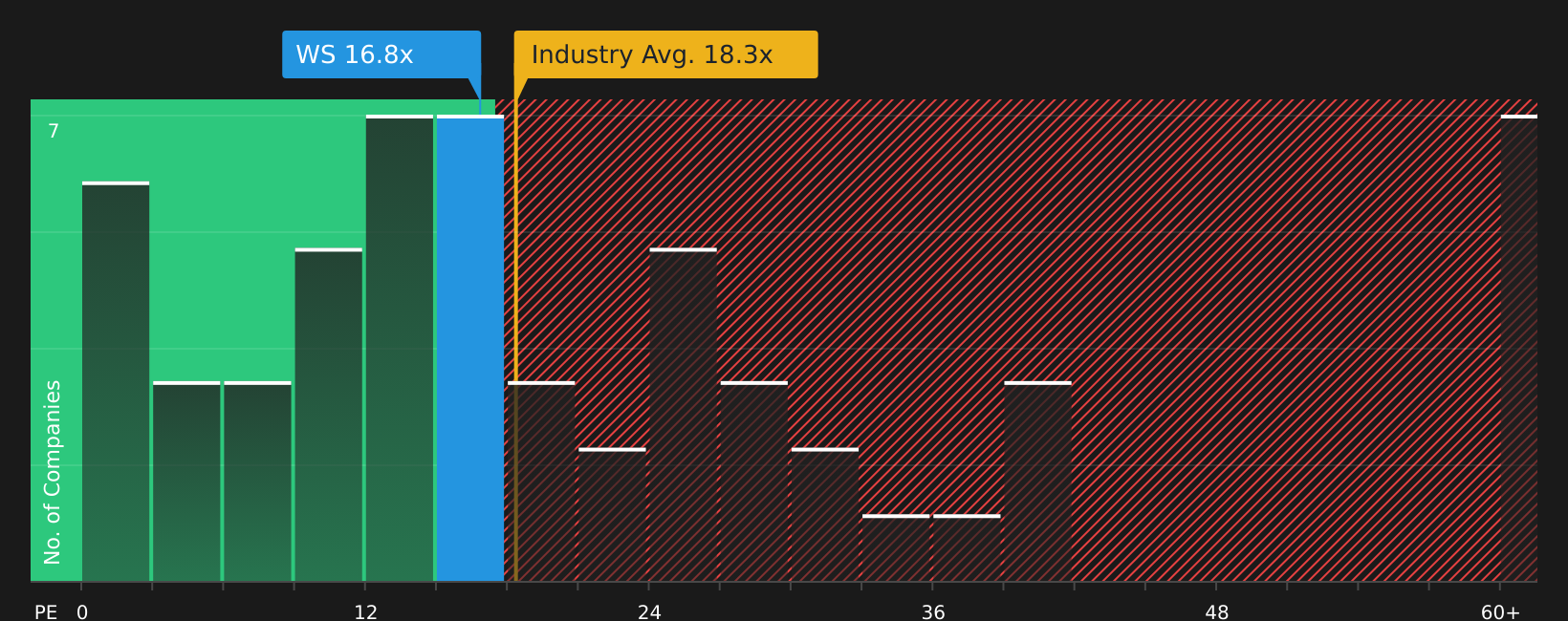

The narrative fair value for Worthington Steel points to shares being about 7.2% above the US$38 analyst target, yet the company scores as good value on a P/E of 17x versus an industry average of 18.1x, a peer average of 27x, and a fair ratio of 17.5x that the market could move toward. That mix of signals raises a simple question for investors: which yardstick should carry more weight in your own work?

Next Steps

If this mix of optimism and caution around Worthington Steel leaves you undecided, consider examining the underlying data now and forming your own view with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Worthington Steel?

If Worthington Steel has sharpened your focus on valuation and quality, this is the moment to broaden your watchlist before the next set of opportunities moves away.

- Target potential mispricing by scanning companies that screen as quality yet potentially overlooked using the 45 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that feature resilient payouts through the 8 dividend fortresses.

- Tighten your risk profile by focusing on companies that score well on stability and financial resilience with the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.