W.W. Grainger (GWW) Is Up 7.4% After Raising 2026 Guidance And Boosting Dividend - What's Changed

W.W. Grainger GWW | 0.00 |

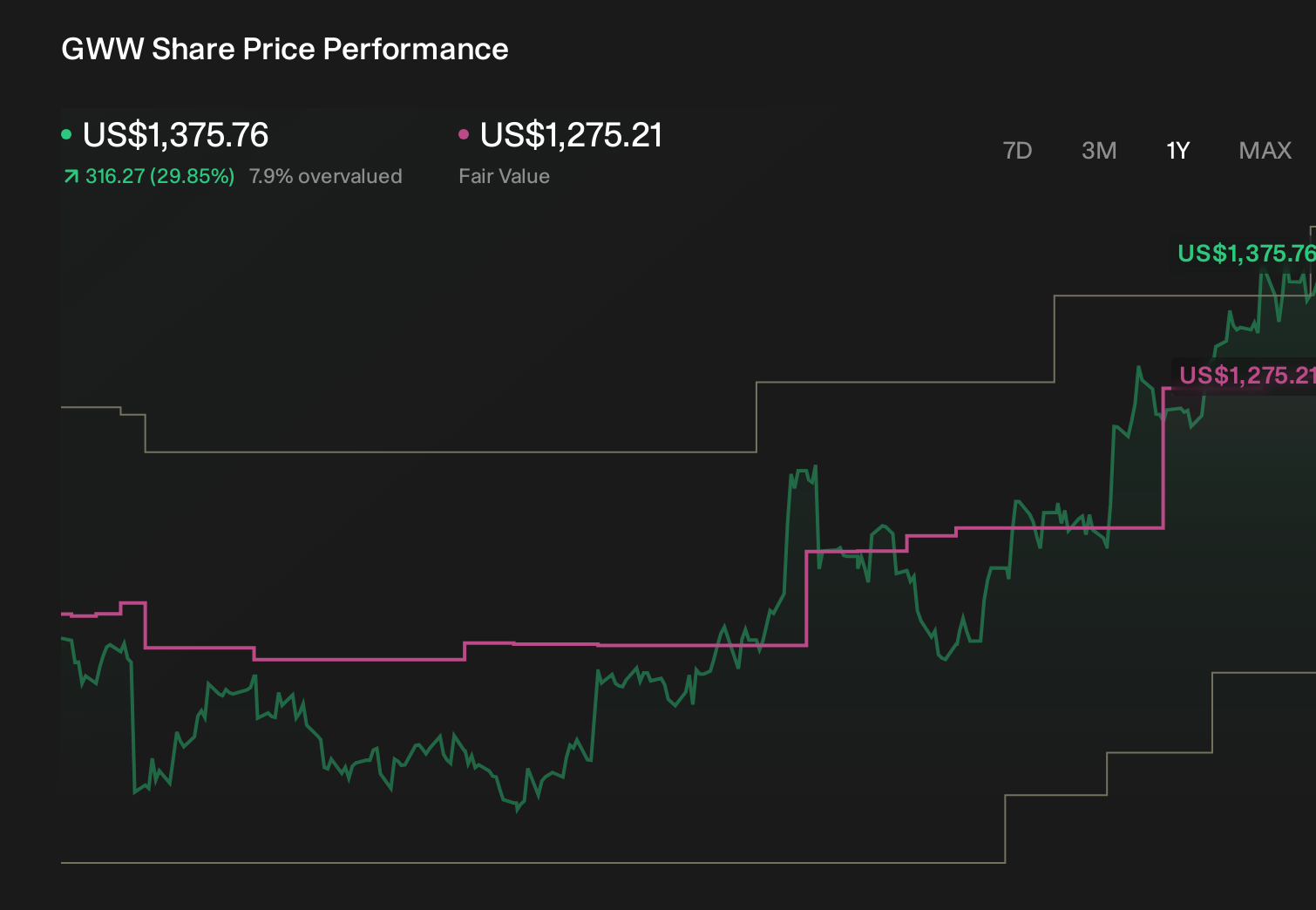

- In early May 2026, W.W. Grainger reported first-quarter 2026 results showing higher sales of US$4.74 billion and increased net income of US$555 million year over year, raised its full-year 2026 net sales and EPS guidance, and filed a new shelf registration for debt securities.

- Alongside these results, the company also announced a higher quarterly dividend of US$2.49 per share, extending its multidecade pattern of annual dividend increases and underlining management’s confidence in cash generation.

- Next, we’ll examine how the raised full-year guidance could influence W.W. Grainger’s existing investment narrative and longer-term expectations.

Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

W.W. Grainger Investment Narrative Recap

To own W.W. Grainger, you generally need to believe that steady MRO demand, digital ordering, and supply chain upgrades can support durable earnings and cash generation. The latest guidance raise reinforces the near term catalyst around profitable growth, but it does not eliminate key risks such as potential margin pressure from tariffs, cost inflation, or a weaker industrial cycle that could curb MRO spending and test Grainger’s pricing power.

The most relevant development is the higher 2026 net sales and EPS guidance, which reflects a stronger first quarter start and underpins the near term growth narrative. By contrast, the new automatic shelf registration for debt simply adds financing flexibility and, on its own, does not materially change the balance between Grainger’s growth catalysts and existing risks around margins, capital intensity, or regional economic exposure.

Yet even with stronger guidance, investors should be aware that tariff and cost pressures could still...

W.W. Grainger's narrative projects $21.6 billion revenue and $2.4 billion earnings by 2029. This requires 6.3% yearly revenue growth and roughly a $0.7 billion earnings increase from $1.7 billion today.

Uncover how W.W. Grainger's forecasts yield a $1150 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$21.5 billion and earnings near US$2.4 billion by 2029, and their focus on flat demand and tariff risk contrasts sharply with the recent guidance upgrade, reminding you that equally informed people can read the same data very differently and that both the optimistic and pessimistic views may shift as fresh results come through.

Explore 3 other fair value estimates on W.W. Grainger - why the stock might be worth as much as 9% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your W.W. Grainger research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free W.W. Grainger research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W.W. Grainger's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.