Wynn Resorts (WYNN) Keeps Barclays Backing, Is It Still Below Fair Value?

Wynn Resorts, Limited WYNN | 0.00 |

Barclays’ latest update on July 9, 2026 kept its Overweight rating on Wynn Resorts (WYNN) while trimming its expectations, a combination that puts fresh attention on how investors are currently valuing the casino operator.

At a share price of US$99.77, Wynn Resorts has seen short term momentum pick up, with a 1 day share price return of 0.95% and a 7 day share price return of 4.02%. However, the 30 day and year to date share price returns show declines of 5.22% and 18.60% respectively, and the 1 year total shareholder return is down 9.43%. This suggests that recent optimism is emerging against a weaker longer term backdrop as investors react to updates like Barclays’ revised assumptions.

If this kind of reassessment has you looking beyond casinos, it could be a good time to broaden your watchlist with 18 top founder-led companies

Analysts see room above today’s US$99.77 price, with Wynn Resorts trading about 35% below Barclays’ target, yet the share price slide this year signals caution. Is that discount an opportunity or a warning sign for valuation?

Most Popular Narrative: 27% Undervalued

Against Wynn Resorts' last close of US$99.77, the most followed narrative pegs fair value at about US$135.89, a wide gap that puts its long term cash generation story under the microscope.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Read the complete narrative. Read the complete narrative.

Curious what needs to go right for Wynn Resorts to justify that higher fair value? The narrative leans on steady top line expansion, fatter margins, and a richer earnings multiple than the broader hospitality sector. The exact mix of growth, profitability and valuation assumptions is where the story really gets interesting.

Result: Fair Value of $135.89 (UNDERVALUED)

However, risks around Macau concentration and rising operating costs mean that any setback in regional demand or margins could quickly challenge the bullish Wynn Resorts narrative.

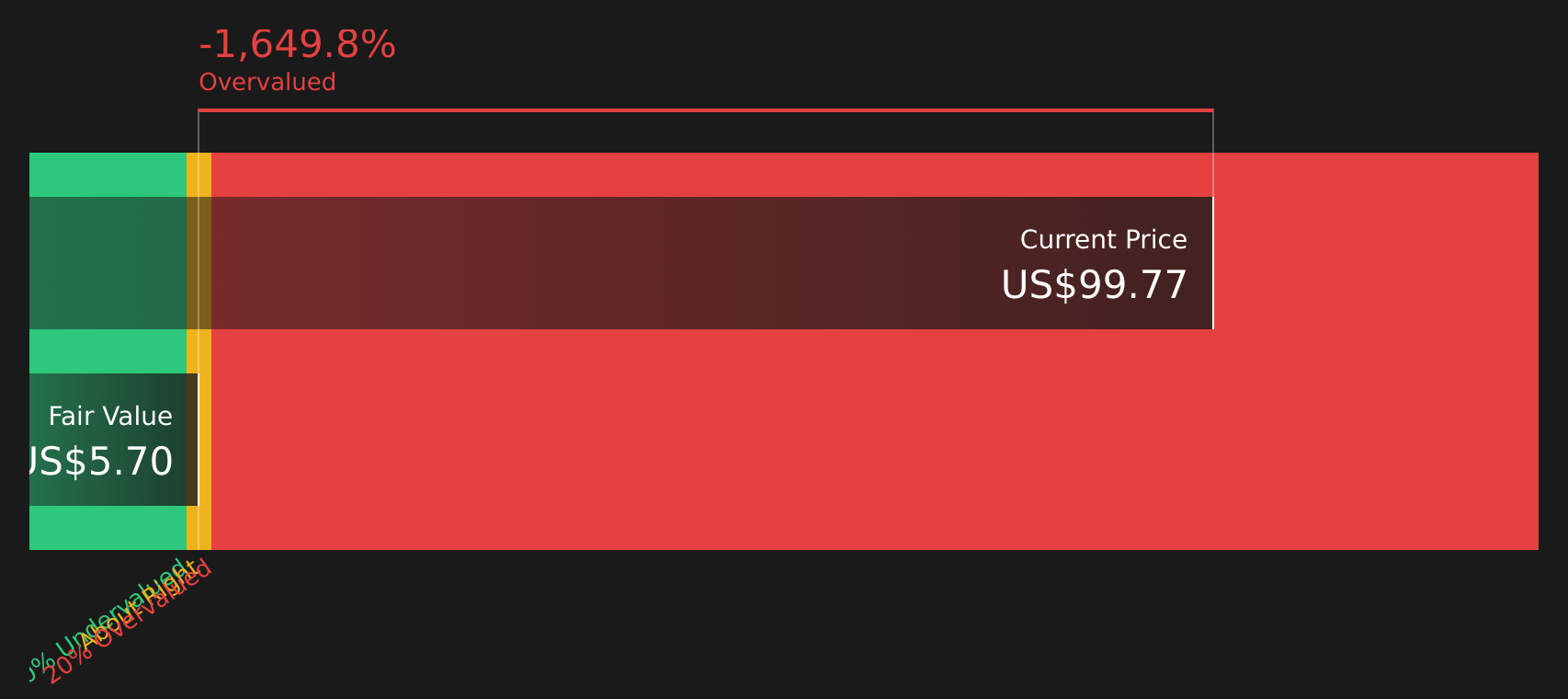

Another View: Wynn Resorts Through a Cash Flow Lens

Price targets for Wynn Resorts focus heavily on earnings and multiples, yet the SWS DCF model tells a very different story. On that framework, the current share price of US$99.77 sits far above an estimated future cash flow value of US$5.69, which points to a strongly overvalued outcome. How much weight should you put on a model that is this conservative compared with the earnings based narrative?

For readers who want to see how this cash flow based result is built from the ground up, our SWS DCF model is fully laid out in one place, including the key assumptions that drive the gap to today’s price. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wynn Resorts for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Wynn Resorts, do you lean toward the risks or the rewards? Take a close look at the numbers, be prepared to move quickly if the picture changes for you, and round out your verdict by checking the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Wynn Resorts?

If Wynn Resorts has sharpened your focus on valuation and risk, now is the moment to widen your opportunity set before the next move in the market catches you off guard.

- Target potential mispricings by scanning companies that combine quality fundamentals with attractive valuations through the 44 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with higher yields and resilient payouts using the 9 dividend fortresses.

- Prioritise resilience by filtering for companies with robust financial positions with the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.