Wynn Resorts (WYNN) Stock Could Be 24% Undervalued After Al Marjan Expansion News

Wynn Resorts, Limited WYNN | 0.00 |

Wynn Resorts (WYNN) is back in focus after two separate announcements: a planned integrated resort at Wynn Al Marjan Island in Ras Al Khaimah, and a multi-year Wynn Revelry culinary partnership at Wynn Las Vegas.

Despite the new resort plan and Wynn Revelry partnership, Wynn Resorts’ recent share price momentum has been mixed, with a 1-month share price return of 6.56% contrasting with a decline of 15.46% year to date, while the 1-year total shareholder return of 16.58% points to a stronger longer term picture.

If these developments have you thinking more broadly about where growth and entertainment trends might intersect, it could be a good moment to scan 20 top founder-led companies

With Wynn Resorts trading at US$103.62 and one valuation measure suggesting the stock sits below an indicated fair value, the key question is simple: is this genuine mispricing, or is the market already accounting for the next leg of growth?

Most Popular Narrative: 24% Undervalued

With Wynn Resorts last closing at $103.62 against a narrative fair value of $135.89, the current price sits well below what this widely followed view considers justified, putting the focus firmly on how future earnings power might bridge that gap.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Curious what sits behind that kind of step change for Wynn Resorts? The narrative leans on measured revenue expansion, thicker margins, and a richer earnings base built over several years. The real story is how these moving parts combine with a premium earnings multiple to reach that fair value, and which assumptions matter most if conditions shift.

Result: Fair Value of $135.89 (UNDERVALUED)

However, Wynn Resorts still faces meaningful risks, including its heavy reliance on Macau and the execution and cost burden tied to large projects like Wynn Al Marjan Island.

Another View on Wynn Resorts’ Valuation

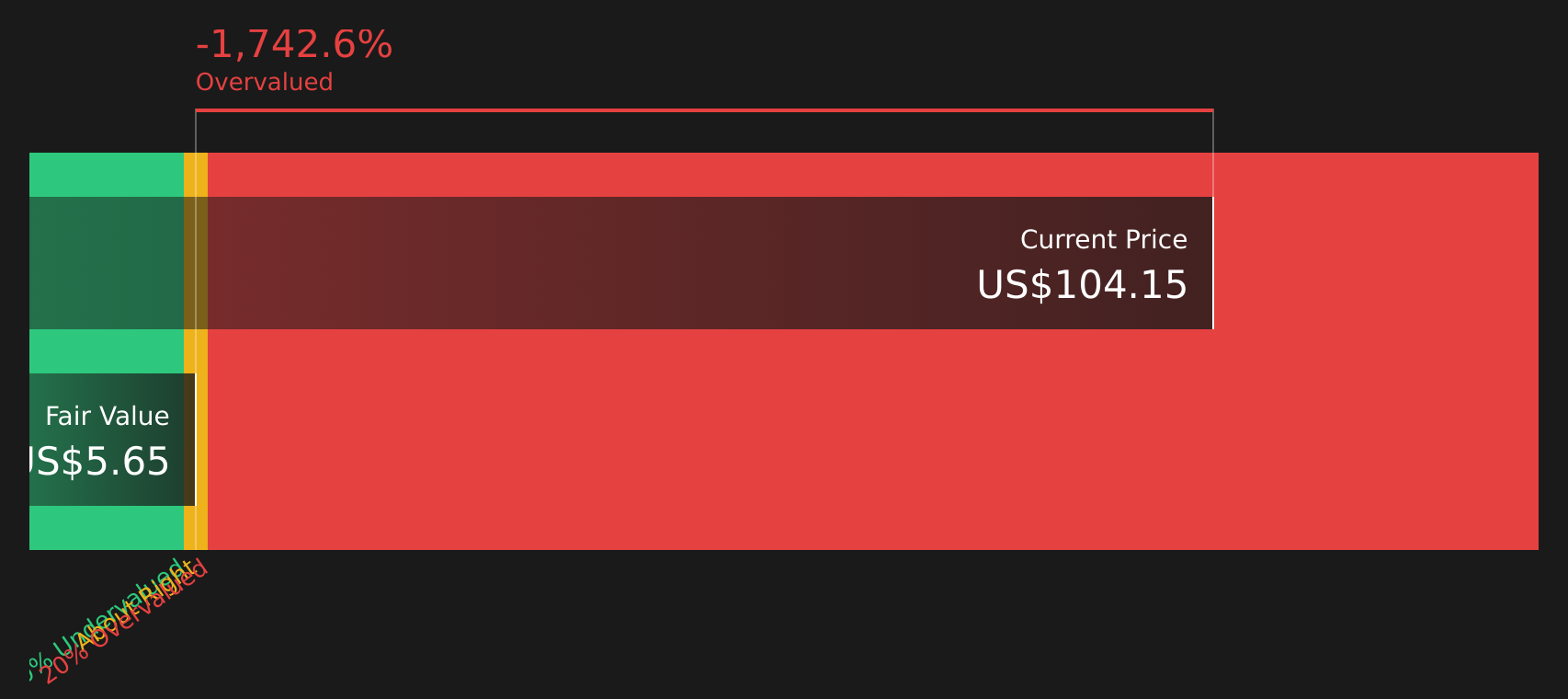

While the analyst narrative points to a fair value of $135.89, the SWS DCF model presents a very different perspective. Wynn Resorts is trading at $103.62 versus an estimated future cash flow value of $5.68, which suggests the stock appears expensive when viewed through this framework. Which perspective do you think better aligns with your expectations for the business?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wynn Resorts for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed sentiment across Wynn Resorts’ valuation signals, this is a good moment to review the numbers yourself and weigh both risk and upside potential. You can then round out your research by checking the 2 key rewards and 2 important warning signs

Looking for more ideas beyond Wynn Resorts?

If Wynn Resorts has sharpened your focus on where to put fresh capital, do not stop here. Broader idea generation can give you useful context and options.

- Target potential mispricing opportunities by scanning companies that screen as high quality yet priced below implied worth through the 44 high quality undervalued stocks.

- Build a steadier income stream by reviewing stocks that feature reliable payouts using the 7 dividend fortresses.

- Prioritize resilience by searching for companies that show strong fundamentals and lower risk profiles via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.