Wynn Resorts (WYNN) Valuation Check As CEO Engages Chinese Officials On Macau And Market Access

Wynn Resorts WYNN | 0.00 |

Wynn Resorts (WYNN) is back in focus after CEO Craig Billings joined other US executives in talks with Chinese Foreign Minister Wang Yi about trade barriers, market access, and operating conditions for American companies.

At a share price of US$105.26, Wynn Resorts has seen its 30 day share price return of 5.93% and 90 day share price return of 6.55% contrast with a year to date share price decline of 14.12%. Meanwhile, the 1 year total shareholder return of 21.38% and 3 year total shareholder return of 4.90% point to mixed momentum over different timeframes as investors weigh US China policy signals, recent entertainment announcements in Las Vegas, and operational headlines.

If this kind of headline has you thinking more broadly about where capital is moving next, it could be a good moment to scan 19 top founder-led companies

With Wynn Resorts trading at US$105.26, reporting revenue of US$7.29b and net income of US$375.04m, and carrying a low value score of 1, you have to ask: is this a buying opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 22.5% Undervalued

Against the last close of US$105.26, the most followed narrative pins Wynn Resorts' fair value at US$135.89, setting a higher bar for where the stock might trade if its assumptions hold.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Curious what sits behind that confidence in Al Marjan and future cash generation? The narrative leans on specific revenue growth, margin expansion, and earnings power assumptions that are not yet visible in current reported numbers.

Result: Fair Value of US$135.89 (UNDERVALUED)

However, this hinges on Macau staying resilient and large capital projects like Al Marjan hitting timelines and returns that justify Wynn Resorts' higher spending and risk profile.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

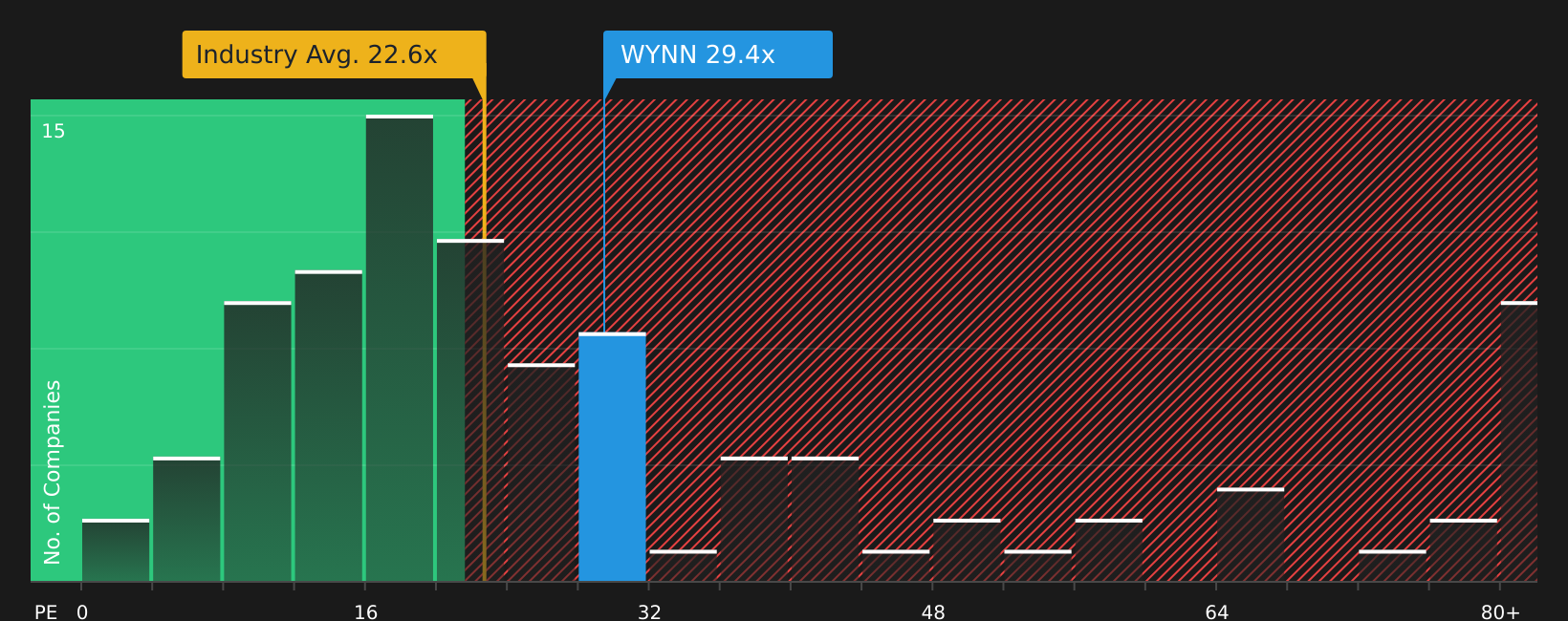

Another View: What The P/E Ratio Is Saying

While the fair value narrative points to upside, the current P/E of 28.7x tells a more cautious story. It sits above both the estimated fair ratio of 27.4x and the US Hospitality industry average of 20.6x, which suggests less margin for error if expectations slip.

For investors who lean on market based ratios rather than long term narratives, this gap raises a simple question: is the current price already baking in a lot of the optimism that analysts see in their forecasts, or not yet?

Next Steps

With sentiment split between optimism and concern, it helps to check the facts for yourself and decide where you stand on Wynn Resorts. To weigh both sides of the story in one place, take a closer look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Wynn Resorts has sharpened your thinking, do not stop here. Use focused stock lists to spot other opportunities that fit your style before the crowd does.

- Target potential mispricings by scanning companies flagged as 47 high quality undervalued stocks that combine solid fundamentals with a gap between market price and assessed worth.

- Strengthen your income side by reviewing 9 dividend fortresses built around companies with higher yields and a focus on consistent shareholder payouts.

- Reduce portfolio stress by checking 63 resilient stocks with low risk scores where resilient balance sheets and steadier risk profiles take center stage.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.