Xometry (XMTR): Assessing Valuation Following Launch of Automated Injection Molding Quoting in the U.S.

Xometry, Inc. Class A XMTR | 0.00 |

Xometry (XMTR) is shaking up the manufacturing space again by rolling out automated quoting for injection molding services across the U.S. This move comes after a strong European debut and aims to make sourcing molded parts much faster and simpler for businesses.

The momentum around Xometry continues to build, with management set to present at upcoming tech and AI investor conferences following this U.S. product expansion. The 1-year total shareholder return of 116.6% highlights the market’s renewed confidence in the company’s growth potential, particularly after a notable 90-day run despite some recent short-term volatility.

If this kind of digital manufacturing innovation sparks your interest, now is a smart time to discover See the full list for free.

With shares not far from analyst price targets but still trading below some measures of intrinsic value, investors have to ask whether there is more upside left or if all the future growth is already reflected in the current price.

Most Popular Narrative: 2.8% Undervalued

Xometry’s fair value, according to the most widely followed narrative, is $50.11 per share, just above its recent close of $48.69. With analysts expecting solid forward growth and expanding market share, the stage is set for both bullish momentum and healthy debate about future upside.

The rapid deployment of AI and machine learning across pricing, supplier selection, and workflow automation is substantially improving efficiency, optimizing gross margin, and providing significant operating leverage. This positions the company for margin expansion and improving EBITDA.

Wondering what ambitious projections get Xometry so close to a premium tech multiple? The full narrative hints at major revenue acceleration, sharper profit margins, and a leap in expected earnings that rivals high-growth disruptors. Hungry to see exactly which quantitative targets back up this valuation? Find out inside the complete narrative.

Result: Fair Value of $50.11 (UNDERVALUED)

However, persistent lack of consistent profitability and fierce industry competition could still derail Xometry’s optimistic growth story and temper near-term investor enthusiasm.

Another View: What If the Market’s Right?

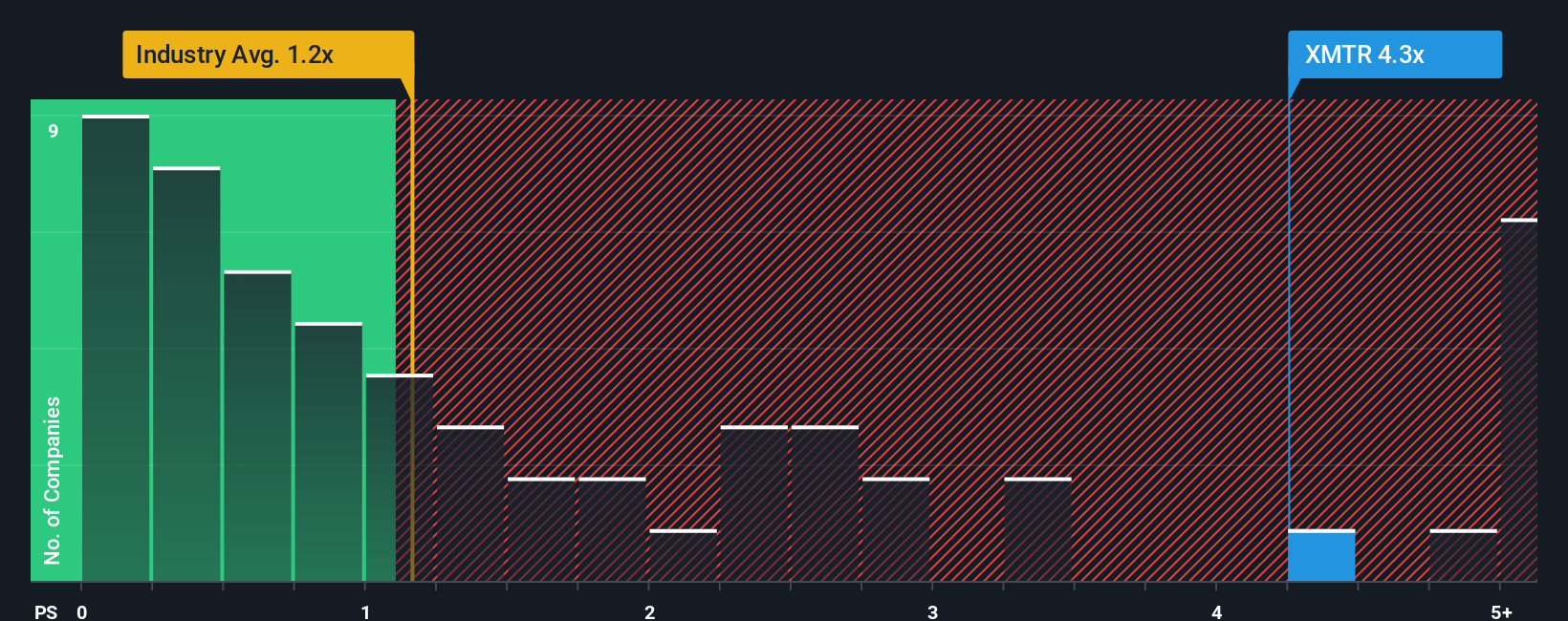

While the main narrative points to some upside, looking at Xometry’s price-to-sales ratio tells a different story. Currently, shares trade at 4.1 times sales, which is not only higher than the industry average of 1.1 and peer average of 1.4, but also above the fair ratio of 3.2. This means Xometry is priced at a premium, suggesting the market has already baked in a lot of optimism and leaves less room for upside if the company stumbles. Could this premium signal more risk than opportunity if expectations aren’t met?

Build Your Own Xometry Narrative

If you see the numbers differently or want to dig deeper into your own research, Xometry's platform lets you piece together a custom perspective in minutes. Do it your way

A great starting point for your Xometry research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Miss out on the chance to broaden your portfolio and you might overlook companies set to outperform. Jump on these timely opportunities now with a powerful head start from the Simply Wall Street Screener.

- Capitalize on the momentum by checking out these 839 undervalued stocks based on cash flows, where you'll find stocks trading below their intrinsic worth and potentially poised for big gains.

- Pounce on income opportunities as you boost your yield with these 23 dividend stocks with yields > 3%, spotlighting companies offering robust dividends and consistent payouts above 3%.

- Seize an edge in transformative technology by scanning these 26 AI penny stocks, highlighting innovative firms powering the surge in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.