Xometry (XMTR): Assessing Valuation Following Launch of New Workcenter Mobile App for Suppliers

Xometry, Inc. Class A XMTR | 0.00 |

Xometry (XMTR) has unveiled its new Workcenter Mobile App, designed to give suppliers in its network easier access to manage job offers, production, and shop performance from their smartphones. The launch builds on the company's existing Workcenter platform.

Xometry’s release of the Workcenter Mobile App comes as the company’s momentum has picked up noticeably. The stock boasts a 44% gain in its 90-day share price return and a total shareholder return of 166% over the past year. This strong run suggests the market is warming up to Xometry’s growth story, even as recent weeks saw a brief dip.

If the rapid innovation at Xometry has you curious about where else growth may be brewing, consider stepping outside the usual names and discover fast growing stocks with high insider ownership

Yet with shares soaring over the past year, the real question now is whether Xometry is actually undervalued or if the current price already reflects high expectations for future growth, which could leave little room for further gains.

Most Popular Narrative: Fairly Valued

At $50, Xometry’s latest close is just above the narrative’s fair value estimate of $49.33. The stage is set with analysts split on whether the stock price now fully reflects near-term optimism. Let’s look at the reasoning that’s fueling this view.

Xometry’s platform investments have helped it become a strategic sourcing partner for larger enterprise clients, leading to deeper integration into customer workflows and improved client retention. Expanding international reach and broadening instant quote capabilities across more product categories are positioning Xometry to capture greater share within the $2 trillion manufacturing market.

Intrigued by how these strategic bets and ambitious global moves translate into today’s price? The answer hinges on a web of projections for future revenues, margins, and scale that could surprise even seasoned market-watchers. Unpack the assumptions driving the narrative’s conclusion.

Result: Fair Value of $49.33 (ABOUT RIGHT)

However, persistent operating losses and intensifying competition in digital manufacturing could still threaten Xometry’s projected growth and margin improvements.

Another View: Multiple-Based Valuation Reveals Expensive Territory

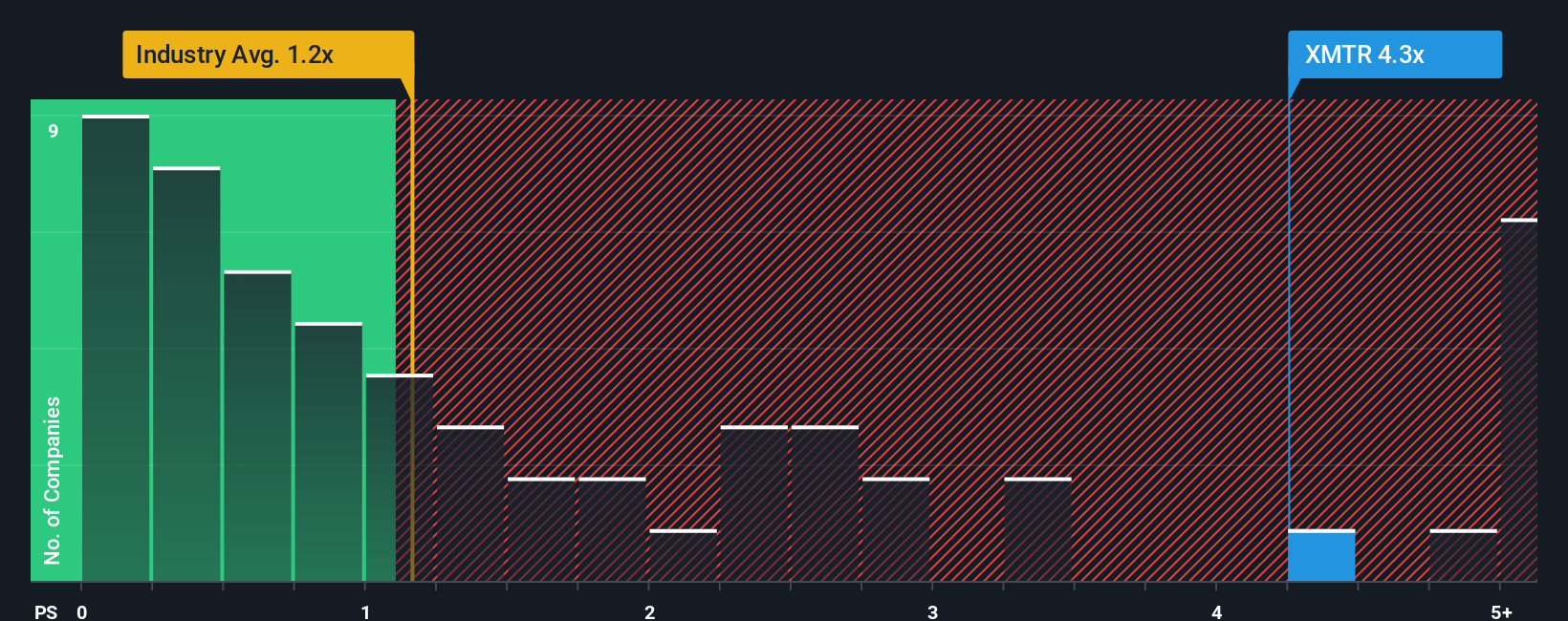

While our earlier analysis points to fair value, looking at Xometry’s price-to-sales ratio offers a different perspective. At 4.2x, it stands well above both industry average (1x) and peers (1.4x), and exceeds the fair ratio of 3.1x. This premium suggests the market is pricing in robust growth. However, does it leave enough margin for error?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Xometry for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Xometry Narrative

Prefer to form your own verdict or want to see how the data stacks up firsthand? Put together your own conclusions in just a few minutes with Do it your way

A great starting point for your Xometry research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never stop at just one stock pick. Use the Simply Wall Street Screener to uncover opportunities you may not have considered but definitely shouldn't miss out on.

- Strengthen your portfolio's income stream by tapping into these 18 dividend stocks with yields > 3% offering yields above 3 percent, designed to reward steady holders.

- Tap into tomorrow’s breakthroughs with these 25 AI penny stocks. Ride the surge in innovation across artificial intelligence and automation.

- Stay a step ahead of the crowd to spot value plays among these 887 undervalued stocks based on cash flows, which look attractively priced based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.