XPeng (XPEV) Valuation In Focus After January 2026 Deliveries Drop 34%

XPENG INC. XPEV | 17.66 17.70 | -1.18% +0.23% Post |

XPeng (XPEV) is back in focus after January 2026 deliveries fell 34% year over year to 20,011 vehicles, a shift that has sharpened attention on its near term growth and profitability path.

The weaker January deliveries have been accompanied by fading share price momentum, with XPeng’s 30 day share price return of 16.77% and 90 day share price return of 29.80% both in decline. Its 3 year total shareholder return of 70.43% still contrasts sharply with its 5 year total shareholder return of 64.89%.

If XPeng’s recent volatility has you reassessing the sector, this could be a useful moment to scan other auto makers and review auto manufacturers.

With the share price sliding over the last month and quarter, a sizeable gap to analyst targets, and mixed delivery news, the key question now is whether XPeng is trading below its underlying potential or if the market is already factoring in future growth.

Most Popular Narrative: 40.4% Undervalued

At $16.77, XPeng trades well below the most followed narrative fair value estimate of $28.16, which is built on detailed growth and profitability forecasts using an 11.46% discount rate.

The analysts have a consensus price target of $26.291 for XPeng based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $33.26, and the most bearish reporting a price target of just $18.27.

Want to see what sits behind that gap between today’s price and the fair value line? Revenue scaling, margin shifts and a richer future earnings multiple all sit at the core of this narrative, but the exact mix of those assumptions might surprise you.

Result: Fair Value of $28.16 (UNDERVALUED)

However, this hinges on XPeng turning persistent net losses around while fending off intense price competition at home. Any stumble on either front could quickly challenge that upside story.

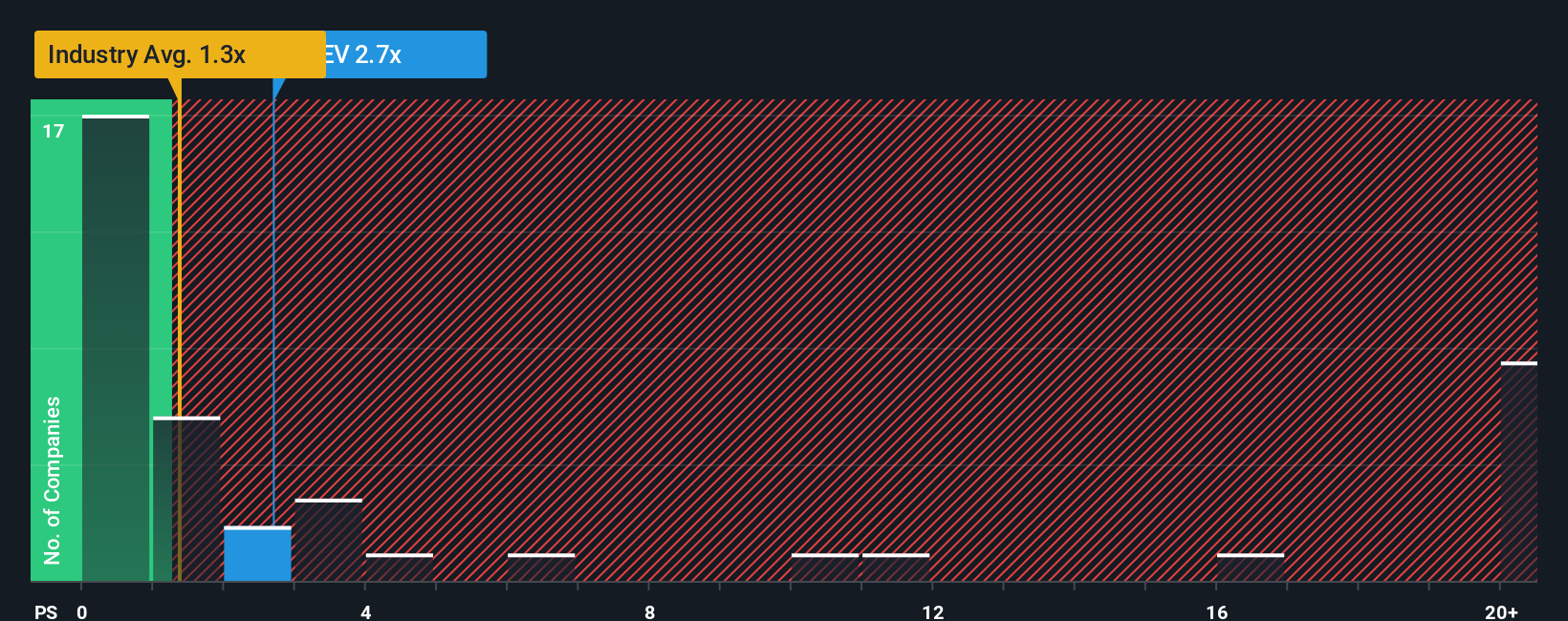

Another View: What The Sales Multiple Is Saying

XPeng screens as good value against its peer group on a P/S ratio of 1.6x versus 2x, yet looks expensive compared with the broader US Auto industry at 0.7x and sits exactly on our fair ratio of 1.6x. That mix points to limited cushion if sentiment weakens again, or room for a rerating if peers keep trading richer. Which side do you think gives first?

Build Your Own XPeng Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can spin up your own full XPeng story in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding XPeng.

Looking for more investment ideas?

If XPeng is only one piece of your watchlist, you can use the Simply Wall St Screener to spot other focused opportunities before the crowd.

- Target dependable income by scanning these 11 dividend stocks with yields > 3% that might suit investors who care about regular cash returns as much as share price moves.

- Explore developments in medicine by sorting through these 105 healthcare AI stocks that apply artificial intelligence to diagnostics, treatment planning, and healthcare operations.

- Review opportunities in the digital assets theme by looking at these 19 cryptocurrency and blockchain stocks that are building businesses around blockchain infrastructure and cryptocurrency services.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.