Yantai Jereh Stock And Two Power Plays For Fed Era Energy

Modine Manufacturing Company MOD | 0.00 |

With Kevin Warsh facing his first interest rate decision as Fed Chair and inflation running at 4.2% on the back of higher oil prices linked to the Iran war, energy stocks sit close to the policy crossfire. Tight Fed rhetoric, elevated inflation and strong labor data create a complex backdrop that can reward some companies and challenge others. This article highlights 3 large energy stocks from our screener that appear most exposed to these macro currents. The goal is to help you decide whether they belong on your watchlist as potential opportunities or risks as the Fed sets its tone under new leadership.

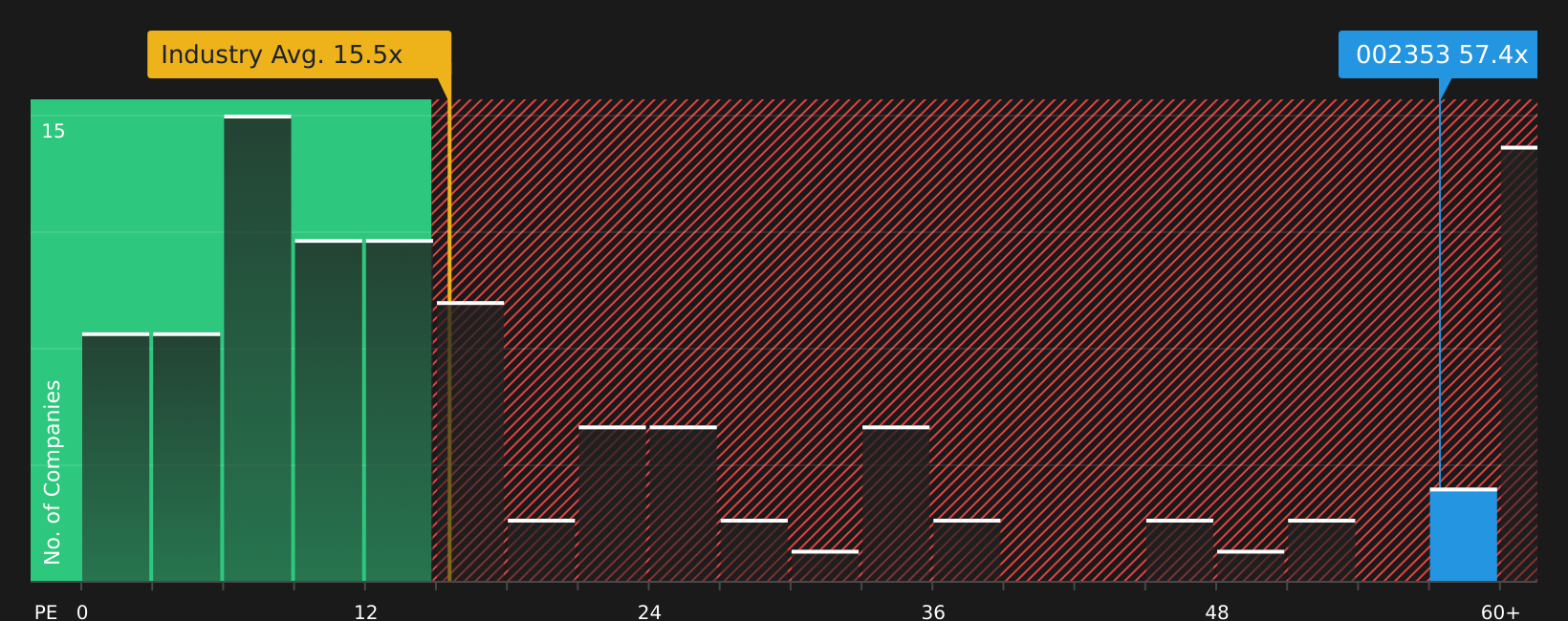

Yantai Jereh Oilfield Services Group (SZSE:002353)

Overview: Yantai Jereh Oilfield Services Group is a China based energy equipment and services company that supplies oilfield machinery, natural gas processing systems, data center and power solutions, and environmental and new energy technologies to oil and gas, industrial and infrastructure customers worldwide.

Market Cap: CN¥158.00b

Yantai Jereh Oilfield Services Group sits at the intersection of higher oil prices and rising demand for energy and power infrastructure equipment, which helps explain its strong recent revenue and earnings momentum. Forecast earnings growth of 28.61% a year and revenue growth of 25.1% a year are paired with high quality earnings and solid net profit margins. However, the stock trades on a rich P/E and well above one cash flow based fair value estimate, so expectations are high. The company also has a modest but reliable dividend and active buybacks, and it has exposure to energy infrastructure that could benefit if the Fed holds rates while inflation stays firm. Overall, this is a growth story where execution risk and valuation discipline matter just as much as the potential upside.

Yantai Jereh’s rapid revenue and earnings momentum, together with its exposure to energy and power infrastructure, raises a key question: does the growth story still justify the current valuation premium in the analyst forecasts for Yantai Jereh Oilfield Services Group

Modine Manufacturing (MOD)

Overview: Modine Manufacturing is a US based industrial company that provides thermal management and heat transfer solutions, from heaters and cooling systems for buildings and vehicles to advanced cooling equipment for data centers and power infrastructure.

Operations: Modine generates about US$2.1b from Climate Solutions and US$1.1b from Performance Technologies, with a small corporate adjustment of US$13m.

Market Cap: US$14.5b

Modine Manufacturing sits at the crossroads of energy infrastructure and digital infrastructure, supplying thermal systems that keep data centers, industrial sites and HVAC installations running efficiently just as investors focus on energy costs, inflation and grid reliability. The company has strong growth expectations for revenue and earnings, backed by a long term US$4b data center cooling agreement and plans to focus more tightly on higher margin Climate Solutions. At the same time, a very high P/E ratio, thinner recent profit margins and reliance on external borrowing mean the market is already pricing in a lot of success. For investors watching how the Fed’s next moves intersect with energy and AI related demand, Modine is a stock that may warrant closer analysis.

Modine Manufacturing’s data center story is accelerating, yet the market is already pricing in a lot of success. Before you decide where the real upside and pressure points sit in this setup, read the analyst forecasts for Modine Manufacturing

Flex (FLEX)

Overview: Flex is a global manufacturing and supply chain partner that designs, builds and manages complex hardware for customers across data centers, communications, automotive, industrial and healthcare, with a growing focus on high power and cooling systems for AI data centers and other power hungry infrastructure.

Operations: Flex generates US$11.1b from Integrated Technology Solutions, US$10.2b from Regulated Manufacturing Solutions and US$6.6b from Cloud and Power Infrastructure.

Market Cap: US$54.85b

Flex stands out for investors looking at energy linked opportunities because it sits where high power AI data centers, grid infrastructure and advanced manufacturing meet. Analyst forecasts currently indicate earnings growth of about 39.8% a year and revenue growth close to 19.7%. The planned spin off of its cloud and power infrastructure business, upcoming inclusion in the S&P 500 and new AI focused power products give Flex direct exposure to capital spending on energy hungry compute. At the same time, a rich 62.1x P/E, thin 3.2% net margins, heavy use of external borrowing and recent insider selling mean expectations are already elevated and funding risk matters. How investors weigh that trade off is what makes Flex a stock worth closer attention as Fed policy and energy costs stay in focus.

Flex’s AI and power story is accelerating, but the real tension sits between those growth ambitions and elevated expectations in the analyst forecasts for Flex

The three stocks covered here are just a starting point, with the full screener surfacing 135 more large energy companies that also fit this theme and each carry their own potential narrative in the Energy Sector Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts, balance sheet strength and earnings profiles that align with your highest conviction ideas in the energy sector.

Take Control of Your Investment Journey

If Modine Manufacturing or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the most interesting ideas move from quiet to crowded fast, as momentum builds and prices shift before the crowd catches on. Scan these fresh setups and look for opportunities early.

- Spot potential turnaround stories with stronger fundamentals than their share prices imply by running your eye over the 212 high quality undervalued stocks.

- Track where real earnings power meets AI momentum by scanning the 61 profitable AI stocks that aren't just burning cash before these companies move out of under the radar for now.

- Zero in on balance sheet strength and staying power using the curated list of solid balance sheet and fundamentals (409 results) while it still matters for finding resilient entries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.