ZIM Integrated Shipping Services (NYSE:ZIM): How Recent Weakness Shapes Its Valuation Outlook and Investor Debate

ZIM Integrated Shipping Services Ltd. ZIM | 26.34 | -0.04% |

ZIM Integrated Shipping Services (NYSE:ZIM) has captured investor attention after its stock fell sharply, sparked by a combination of disappointing quarterly earnings and ongoing global shipping headwinds. The latest results have intensified the conversation around ZIM’s outlook and valuation.

The past year has been turbulent for ZIM, with the 1-year total shareholder return slipping 3.9%, and the share price itself falling more sharply over 2024. Recent setbacks in quarterly earnings and ongoing macro headwinds have weighed on momentum. Some investors are eyeing potential catalysts, such as a sector turnaround and takeover speculation, as reasons to stay tuned.

If this recent volatility has you rethinking your next move, now could be the perfect time to broaden your search and discover fast growing stocks with high insider ownership

With shares down sharply, but ZIM’s outlook featuring both warning signs and potential upside catalysts, investors are left wondering if the current valuation underestimates future growth or if all opportunity is already reflected in the price.

Most Popular Narrative: 6.2% Undervalued

The most widely followed narrative points to a fair value just above ZIM’s last close, implying potential upside if the narrative’s assumptions hold. With analyst expectations shaping the case, closely watched financial trends underpin the valuation outlook.

The company's significant exposure to volatile Transpacific trade leaves earnings highly sensitive to tariff changes and geopolitical shifts. The current overhang of US, China tariffs, unpredictable regulatory moves, and alliance restructurings threaten both volume and rate stability, challenging assumptions that future earnings will be resilient or steadily expanding.

Curious how much shrinking margins and fierce industry headwinds drive the fair value? The key assumptions here may surprise you. Want to see what specific future projections analysts rely on for their price target? Find out what really moves the needle in shipping stocks by clicking for the full breakdown.

Result: Fair Value of $13.26 (UNDERVALUED)

However, significant upgrades to ZIM’s fleet and successful expansion into new trade lanes could quickly shift the outlook and drive stronger than expected performance.

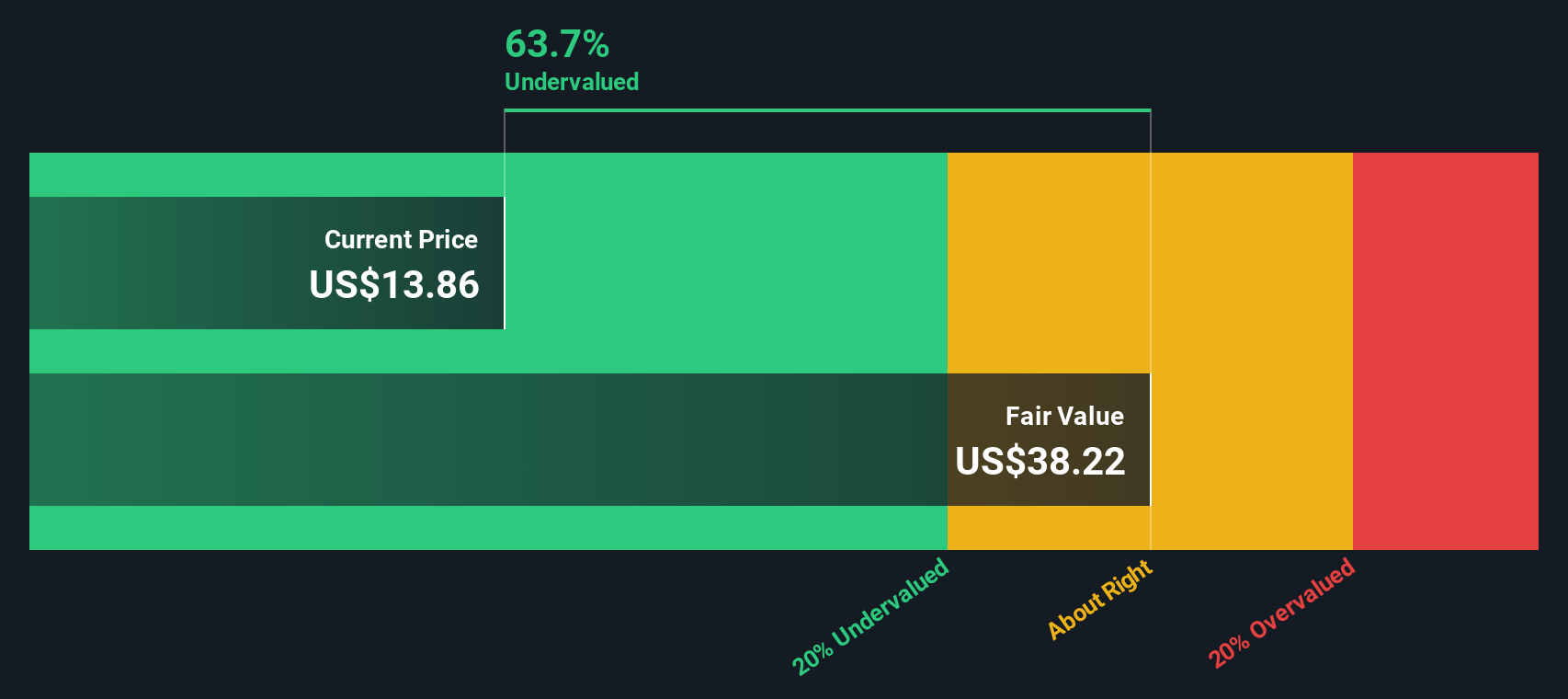

Another View: DCF Points to Much Deeper Undervaluation

While analyst price targets suggest only modest upside from current levels, our SWS DCF model tells a very different story. It estimates ZIM's fair value is a staggering $38.22 per share, which is far above both the market price and typical analyst forecasts. Does this discrepancy suggest hidden value, or are risks being overlooked?

Build Your Own ZIM Integrated Shipping Services Narrative

If you have a different perspective or want to see what the numbers reveal through your own lens, building a personalized view is fast and straightforward. Do it your way

A great starting point for your ZIM Integrated Shipping Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Want to spot your next big winner? Take a smarter approach by checking out handpicked opportunities in fast-moving and resilient sectors. Let Simply Wall Street’s screener power up your research with fresh angles you might otherwise miss.

- Tap into the surge of innovation by following these 24 AI penny stocks, which are making major waves in artificial intelligence and automation breakthroughs.

- Collect stable passive income and position your portfolio for steady growth by reviewing these 19 dividend stocks with yields > 3%, which offer strong yields above 3%.

- Get ahead of the market and track upside potential using these 892 undervalued stocks based on cash flows, which score highly for value right now based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.