ZoomInfo Technologies (GTM) Valuation Check After Recent Share Price Volatility

ZoomInfo Technologies Inc GTM | 5.52 5.52 | +5.54% 0.00% Pre |

Without a specific news event driving attention, interest in ZoomInfo Technologies (GTM) currently centers on how its recent share performance compares with the business it runs in go to market data and sales intelligence.

At a share price of $7.31, ZoomInfo’s recent 7.82% 1 day share price return stands in contrast to a 30 day share price return of 30.25% and a 1 year total shareholder return of 26.9%. This points to pressure on longer term holders even as short term sentiment has flickered higher.

If ZoomInfo’s recent swings have you reassessing your watchlist, it could be a good moment to broaden your search with our screener of 22 top founder-led companies.

With the share price at $7.31, long term returns under pressure and the stock trading at what appears to be a steep discount to analyst targets, is ZoomInfo undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 51.3% Undervalued

With ZoomInfo Technologies last closing at $7.31 and the most followed narrative pointing to a fair value of $15.00, the gap between price and expectations is wide and very specific about what needs to go right.

The accelerating adoption of advanced AI-powered features such as Copilot and operations solutions is unlocking higher value use cases for enterprise customers, driving strong upsell momentum and expansion into new user personas. This broader product adoption raises average contract values and supports top-line revenue growth through both new customer wins and deeper penetration within existing accounts.

To understand how this growth story arrives at that higher fair value, the narrative focuses on rising margins, steadier revenue growth, and a future earnings multiple that assumes investors remain confident in ZoomInfo’s cash generation potential.

Result: Fair Value of $15.00 (UNDERVALUED)

However, this bullish case still runs into real hurdles, including tighter privacy rules around data collection and large customers building their own in-house data platforms.

Another View: Earnings Multiple Paints a Tougher Picture

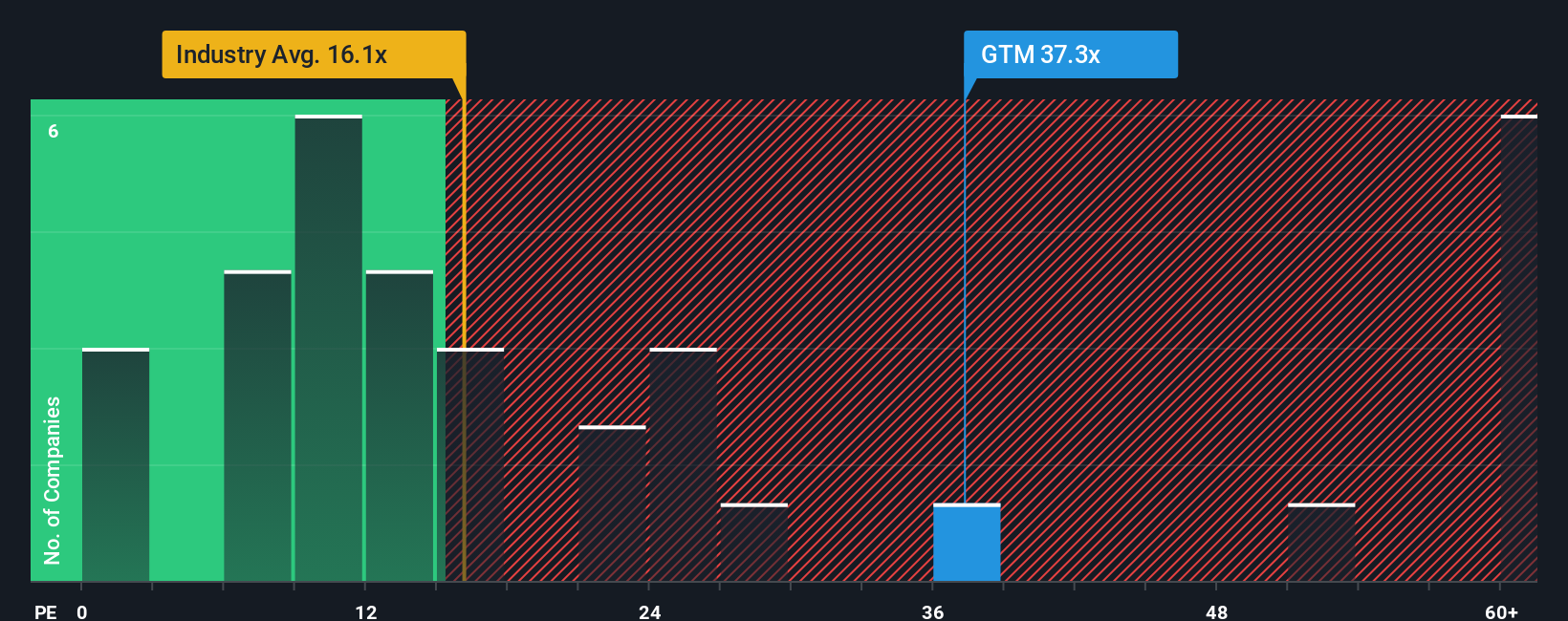

Our DCF model and the most popular narrative both land on ZoomInfo looking undervalued, yet the current P/E of 21.9x tells a different story. It is higher than the peer average of 7.2x, above the US Interactive Media and Services average of 12.7x, and slightly ahead of a 20.7x fair ratio. That gap suggests the share price already bakes in a lot of optimism, so you have to ask whether the business can grow into this richer earnings tag.

Build Your Own ZoomInfo Technologies Narrative

If you are not fully on board with this view or prefer to rely on your own work, you can test the assumptions yourself in a few minutes and Do it your way.

A great starting point for your ZoomInfo Technologies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

ZoomInfo might be on your radar, but you will give yourself a real edge if you widen the net and compare it with other focused ideas from our screener.

- Spot potential value candidates by reviewing companies our screener flags as 53 high quality undervalued stocks based on their fundamentals and pricing.

- Prioritise resilience by checking out businesses in our 86 resilient stocks with low risk scores that score well on stability and risk factors.

- Get ahead of the crowd by scanning our screener containing 24 high quality undiscovered gems featuring companies with solid fundamentals that many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.