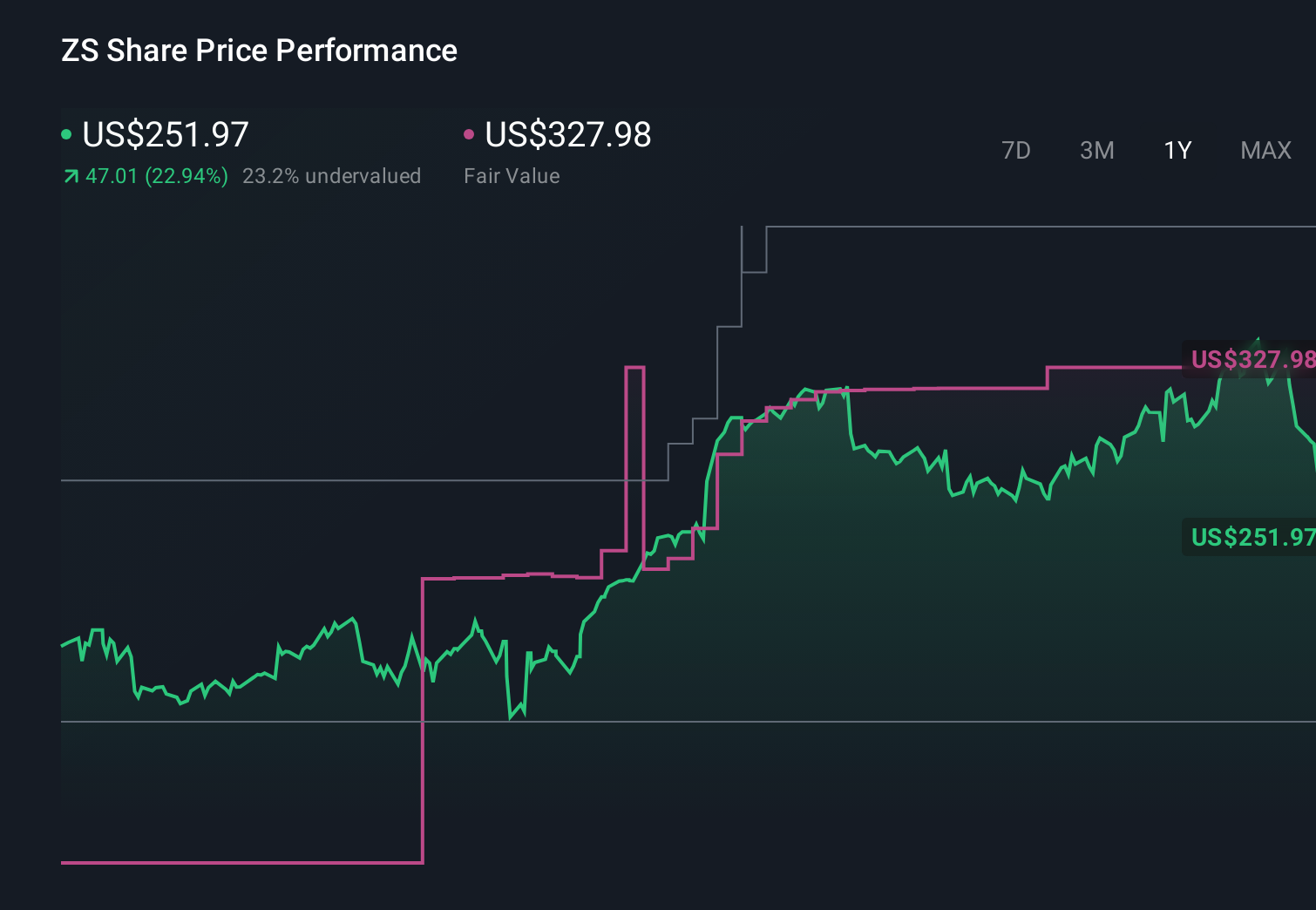

Zscaler (ZS) Is Down 27.5% After Cutting Free Cash Flow Margin Guidance Amid Higher Revenue

Zscaler, Inc. ZS | 0.00 |

- In its recently reported fiscal third quarter 2026, Zscaler posted US$850.48 million in sales, higher year on year, but its net loss widened and the company cut its full-year free cash flow margin guidance while modestly raising revenue guidance to about US$3.33 billion.

- At the same time, Zscaler highlighted strong momentum in AI-focused security products and new alliances, even as higher costs and senior sales departures raised questions about the durability of its execution.

- We’ll now examine how Zscaler’s stronger revenue guidance but lower free cash flow outlook could reshape the company’s Zero Trust AI investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe its Zero Trust and AI security platforms can keep gaining share despite heavy competition and ongoing losses. The latest quarter reinforced that demand story through stronger revenue guidance, but the sharply lower free cash flow margin outlook and rising costs make execution the key short term catalyst and risk, especially after the stock’s sharp pullback and recent senior sales departures.

Project AI Guardian, Zscaler’s new collaboration with major global system integrators, looks particularly relevant here. It ties the company’s AI Protect portfolio directly into large consulting partners that help shape enterprise AI security spending, aligning with the current catalyst around AI driven security budgets while also putting more pressure on Zscaler to convert this technical and channel momentum into more efficient growth and healthier free cash flow.

Yet beneath the AI excitement, investors should also be aware that...

Zscaler's narrative projects $5.2 billion revenue and $152.9 million earnings by 2029. This requires 19.9% yearly revenue growth and a $220.5 million earnings increase from -$67.6 million today.

Uncover how Zscaler's forecasts yield a $227.67 fair value, a 80% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue would grow about 19.7 percent a year and no profits within three years, so this cut to free cash flow margins and higher AI infrastructure spend could push their more pessimistic view on execution risk even further, which is why it is worth comparing how differently people can read the same numbers before you decide where you stand.

Explore 5 other fair value estimates on Zscaler - why the stock might be worth just $198.05!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Zscaler research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.