Zscaler (ZS) Is Up 5.9% After Beating Q3 Views And Striking Aston Martin AI Security Deal – Has The Bull Case Changed?

Zscaler, Inc. ZS | 0.00 |

- In recent days, Zscaler reported fiscal third-quarter 2026 results that exceeded expectations and highlighted strong demand for its Zero Trust platform, alongside new integrations, AI security initiatives, and industry collaborations including a multi-year cybersecurity partnership announced by the Aston Martin Aramco Formula One Team.

- Together with its role in the new Akrites open source security initiative and expanded alliances such as Gigamon integration and Project AI-Guardian, these developments reinforce Zscaler’s growing importance in securing critical infrastructure, complex hybrid cloud environments, and AI workloads.

- We’ll now examine how Zscaler’s stronger-than-expected quarterly results and Aston Martin Aramco partnership may influence the company’s Zero Trust-focused investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe that its cloud native Zero Trust platform can stay differentiated even as large cloud providers and security suites bundle more capabilities. The immediate catalyst is execution on its raised fiscal 2026 guidance and large enterprise adoption, while the biggest near term risk remains intensifying competition and pricing pressure. The Aston Martin Aramco partnership and strong Q3 results support brand and platform relevance, but do not fundamentally change these drivers.

The Aston Martin Aramco Formula One Team deal is particularly relevant because it showcases Zscaler securing highly sensitive, latency critical data flows across track and remote facilities, reinforcing the Zero Trust use case for complex, performance driven environments. This high visibility deployment sits alongside initiatives like Project AI Guardian and Akrites, which collectively support the thesis that Zscaler’s platform is becoming more embedded in securing modern, distributed and AI centric workloads across industries.

Yet despite these positives, investors should still pay close attention to how rising competition could pressure margins and long term earnings power...

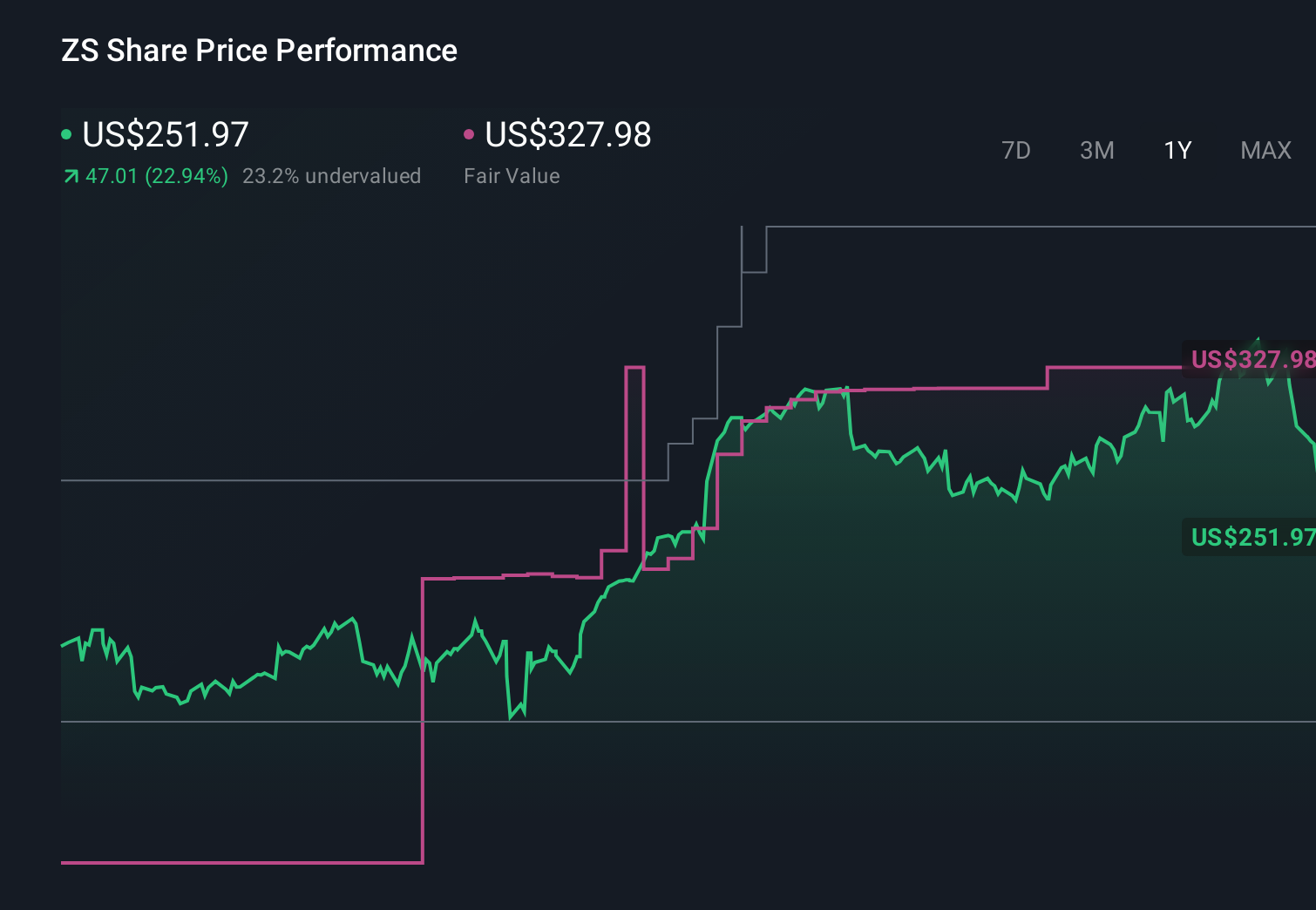

Zscaler’s narrative projects $5.2 billion revenue and $152.9 million earnings by 2029. This requires 19.9% yearly revenue growth and a $220.5 million earnings increase from -$67.6 million today.

Uncover how Zscaler's forecasts yield a $227.67 fair value, a 72% upside to its current price.

Exploring Other Perspectives

Some of the lowest analyst estimates before this news assumed revenue growth near 19.7% and no profitability within three years, which is much more cautious than the consensus view that leans on Zscaler’s Zero Trust expansion and AI security momentum.

Explore 5 other fair value estimates on Zscaler - why the stock might be worth just $192.58!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Zscaler research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

No Opportunity In Zscaler?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.