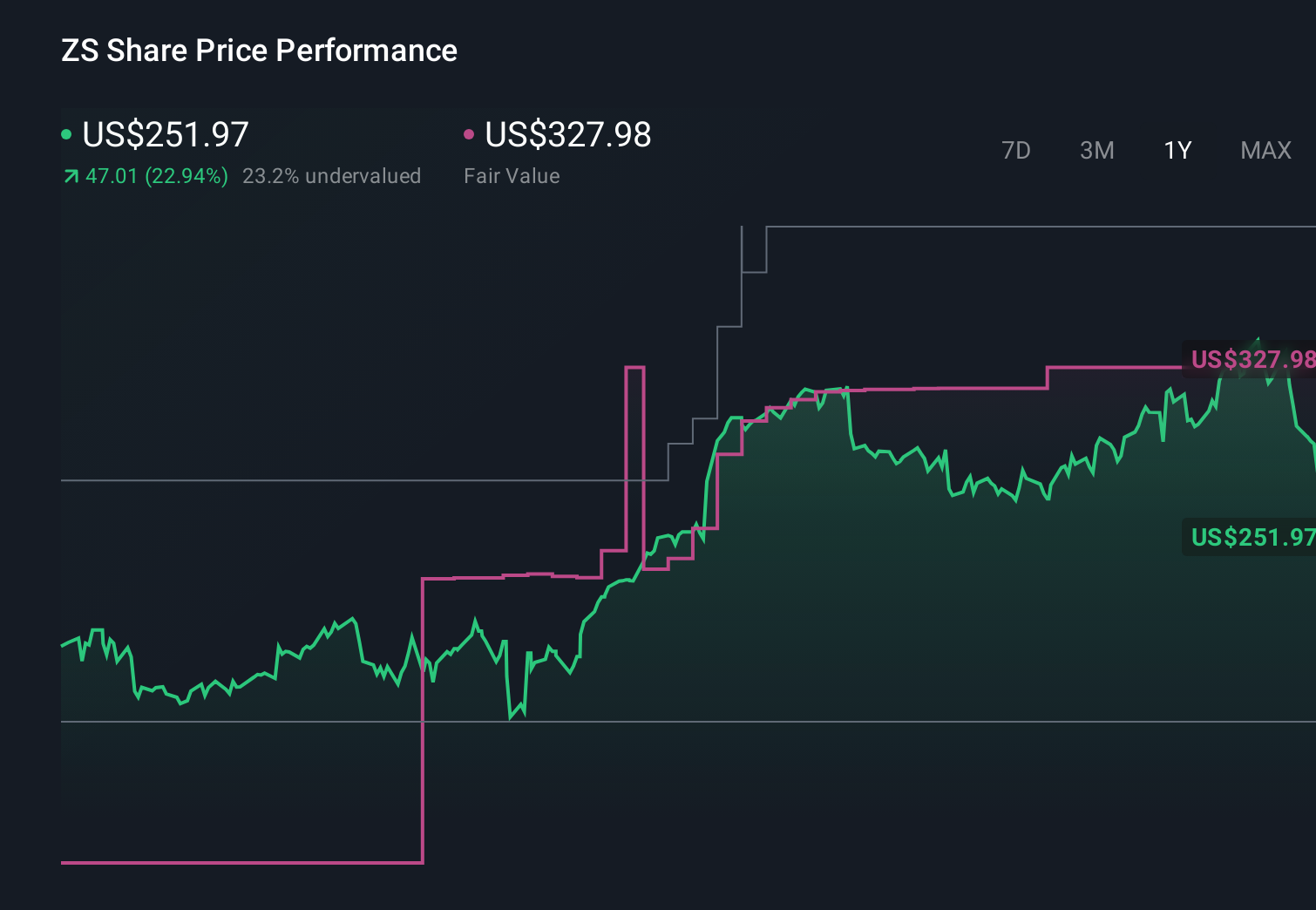

Zscaler (ZS) Is Up 5.9% After Raised ARR Outlook And Software Sector Optimism What's Changed

Zscaler, Inc. ZS | 0.00 |

- In recent days, Zscaler reported strong billings growth and raised its full-year Annual Recurring Revenue guidance, underscoring solid demand for its zero trust cloud security platform.

- This occurred alongside renewed optimism in the broader software sector following Cisco Systems’ upbeat outlook, which has encouraged traders to position ahead of Zscaler’s upcoming Q3 fiscal 2026 earnings report on May 26.

- Next, we’ll examine how Zscaler’s raised ARR guidance and sector tailwinds may influence its existing zero trust AI security investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Zscaler Investment Narrative Recap

To be comfortable owning Zscaler, you need to believe in long term adoption of zero trust, cloud delivered and AI enhanced security despite intense competition and ongoing losses. The latest billings strength and raised ARR guidance support that demand narrative and keep the upcoming Q3 FY2026 report as the key short term catalyst, with execution risk around maintaining growth and margins still the most important concern.

The most relevant recent announcement is Zscaler’s lift to full year fiscal 2026 ARR guidance to about US$3.73–3.75 billion, alongside revenue of roughly US$3.31–3.32 billion. This higher outlook, coming before the May 26 earnings date, ties directly into the ARR driven thesis and will likely frame how investors weigh growth catalysts like AI security against the risk of rising competition and cost pressure.

Yet beneath the stronger ARR guidance, there is a risk around tighter IT budgets and slower zero trust rollouts that investors should be aware of...

Zscaler's narrative projects $5.2 billion revenue and $152.9 million earnings by 2029.

Uncover how Zscaler's forecasts yield a $227.67 fair value, a 41% upside to its current price.

Exploring Other Perspectives

The most pessimistic analysts sounded cautious, assuming about 19.7 percent annual revenue growth and no profitability within three years, so even with upbeat ARR news, you should recognize how differently others weigh execution and AI margin risks before deciding which narrative you find more convincing.

Explore 8 other fair value estimates on Zscaler - why the stock might be worth 38% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Zscaler research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.