Zscaler (ZS) Valuation Check After Launch Of AI Security Suite And 2026 AI Threat Report

Zscaler, Inc. ZS | 138.56 | +1.38% |

Zscaler (ZS) is back in focus after launching its AI Security Suite alongside the 2026 AI Threat Report, which flagged critical vulnerabilities across all analyzed enterprise AI systems and rapidly exploitable weaknesses.

Despite enthusiasm around the AI Security Suite launch, Zscaler’s recent share price returns have been weak, with a 30 day share price return of 11.78% and a 90 day share price return of 39.41%. Its 3 year total shareholder return of 41.94% contrasts with a 1 year total shareholder return close to flat, suggesting momentum has faded after a stronger multi year run.

If AI security is on your radar, this could be a moment to broaden your watchlist and check out high growth tech and AI stocks as potential peers and alternatives.

With Zscaler shares showing recent double digit declines and the AI Security Suite drawing fresh attention, the key question now is whether current prices understate its Zero Trust and AI security potential, or if the market is already baking in that future growth.

Most Popular Narrative: 37% Undervalued

With Zscaler last closing at $200.63 against a most followed fair value estimate of $318.35, the narrative frames the current price as a sizable discount and ties that gap to expectations around Zero Trust and AI security demand.

Accelerating customer adoption of Zero Trust Everywhere and Data Security Everywhere solutions, particularly among Global 2000 and Fortune 500 firms, is fueling large upsell deals and higher ARR per customer, which should drive sustained double-digit revenue growth and improve net retention rates.

Want to see why this story still lands on a higher fair value, even with an unprofitable base today and richer future margin and growth assumptions baked in, plus a premium earnings multiple that goes well beyond typical software names? The full narrative lays out the revenue path, the margin shift, and how recurring cash flows are treated to reach $318.35.

Result: Fair Value of $318.35 (UNDERVALUED)

However, this story can break if cloud providers integrate more security into their platforms or if rising competition and stock-based pay keep pressure on margins and earnings.

Another View: Multiples Paint a Richer Picture

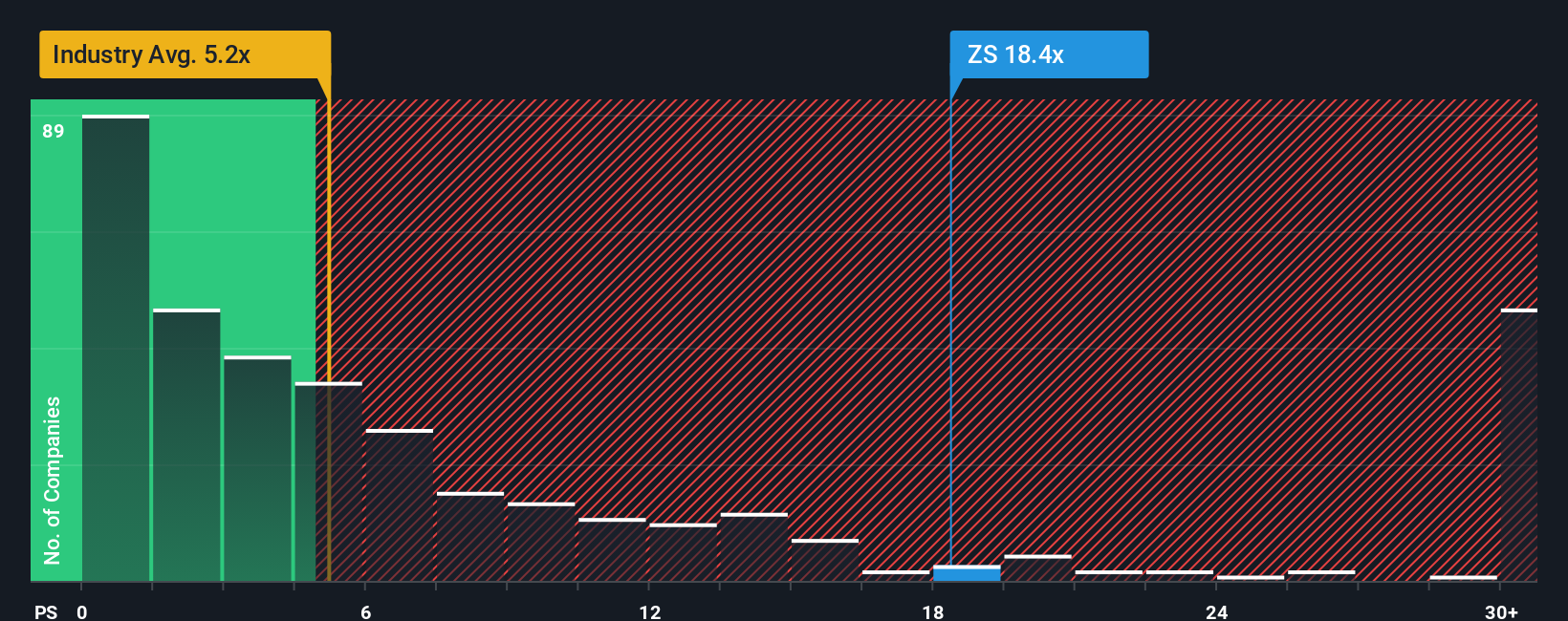

While the narrative and our fair value work point to upside, the current P/S ratio of 11.3x is far above both the US Software industry average of 4.5x and the peer average of 10.7x. It is also above the 10.6x fair ratio our model suggests the market could move toward. That gap can mean valuation risk if expectations cool, so the real question is whether you think Zscaler has earned its premium.

Build Your Own Zscaler Narrative

If this view does not line up with how you see Zscaler, or you prefer to test the numbers yourself, you can build a custom thesis in a few minutes with Do it your way.

A great starting point for your Zscaler research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Zscaler is on your radar, do not stop there. Widening your search with focused stock ideas can help you spot opportunities you might otherwise miss.

- Spot potential value plays by checking out these 866 undervalued stocks based on cash flows that could offer more attractive pricing based on cash flow fundamentals.

- Target the fast moving corner of artificial intelligence with these 23 AI penny stocks that are tied directly to AI themes and applications.

- Balance growth and income by reviewing these 14 dividend stocks with yields > 3% that may appeal if regular cash returns matter to you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.