ZTO Express Shifts To Quality Led Growth After Volume Leadership Run

ZTO Express (Cayman) Inc. Sponsored ADR Class A ZTO | 24.95 | +0.60% |

- ZTO Express (Cayman) set out a new quality led growth plan at its 2026 National Network Conference.

- The company highlighted priorities around operational safety, service upgrades, and network optimization.

- The update follows a decade of industry leadership and expansion in parcel and reverse logistics volumes.

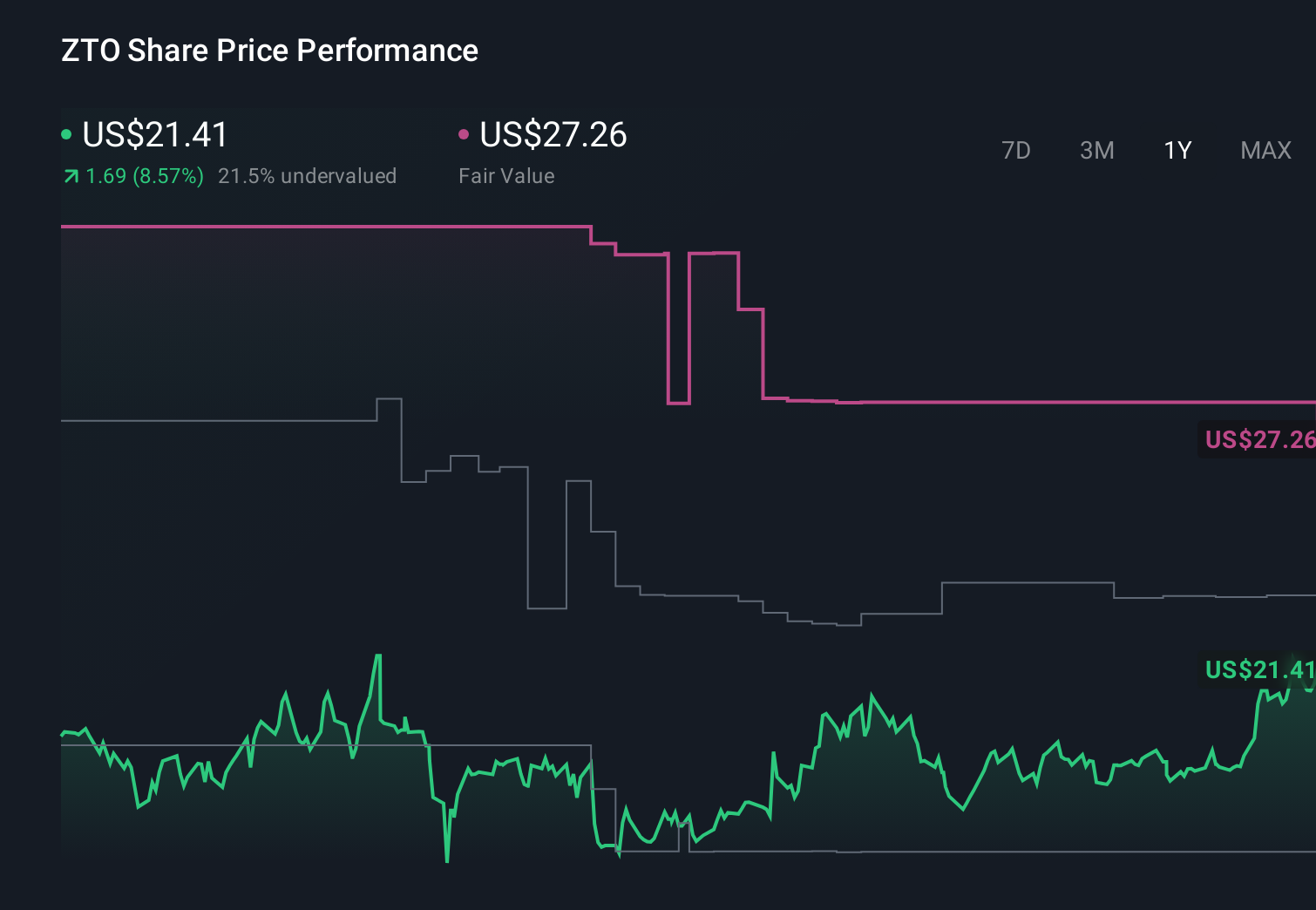

For investors watching NYSE:ZTO, the new roadmap arrives with the stock at $22.32 and a 25.1% gain over the past year. Over a 3 year and 5 year span, returns of 16.3% and 24.8% declines present a more mixed picture. This may help explain why management is putting fresh emphasis on quality and efficiency rather than just more volume. The company is signaling that its long run position in the parcel market could depend as much on reliability and service levels as on scale.

Management’s focus on operational safety, service upgrades, and network optimization suggests that capital and management attention could lean more toward execution quality than pure expansion. For investors, the key questions now are how this shift affects costs, pricing power, and customer retention over time, and whether ZTO Express can translate its decade of leadership into more durable, higher quality growth.

Stay updated on the most important news stories for ZTO Express (Cayman) by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on ZTO Express (Cayman).

ZTO’s leadership is effectively telling investors that the next phase is about deepening quality rather than just pushing higher volumes. After handling 38.52 billion parcels in 2025 and keeping a ten year lead in China’s express market, a push into operational safety, service upgrades, and network efficiency reads as an attempt to protect that position as competition shifts toward integrated logistics and more disciplined, sustainable competition.

How This Fits the ZTO Express (Cayman) Narrative

For anyone who has viewed ZTO mainly as a volume story, this update adds a layer around execution quality and network discipline. The new focus could influence how you weigh its long history of volume leadership against questions on service reliability, reverse logistics capabilities, and potential returns from moving into broader logistics solutions.

Risks and rewards in focus

- Earnings have grown 16.4% per year over the past 5 years, which may support the case that management has executed well through earlier expansion.

- ZTO is trading at what is described as 48.6% below an estimated fair value and at good value compared to peers and industry, which some investors may see as a potential upside case if the quality plan is delivered.

- Earnings are forecast to grow 9.81% per year, suggesting expectations for ongoing progress if the quality led plan takes hold.

- There is an unstable dividend track record, so the renewed focus on quality and efficiency may not immediately translate into a more predictable income stream for shareholders.

What to watch next

From here, it will be worth watching how leadership links its quality push to clear metrics, such as service levels, safety performance, network efficiency, and whether these priorities influence pricing and customer mix over time. You can see how different investors are interpreting this shift by reading community views in this narrative collection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.