3 Value Stocks Including Kratos Defense & Security Solutions That May Be Priced Below Intrinsic Value

Kratos Defense & Security Solutions, Inc. KTOS | 0.00 |

The United States market has experienced a notable upswing with a 4.4% increase over the past week and a substantial 32% rise in the last year, while earnings are projected to grow by 16% annually. In this environment, identifying stocks that may be priced below their intrinsic value can offer investors opportunities for growth, as they look for companies like Kratos Defense & Security Solutions that have strong fundamentals yet remain undervalued by the market.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Uranium Energy (UEC) | $13.36 | $26.41 | 49.4% |

| Roku (ROKU) | $98.20 | $193.48 | 49.2% |

| National Bank Holdings (NBHC) | $40.12 | $79.88 | 49.8% |

| Intapp (INTA) | $24.82 | $49.43 | 49.8% |

| Fluence Energy (FLNC) | $13.20 | $26.13 | 49.5% |

| First Internet Bancorp (INBK) | $21.82 | $43.01 | 49.3% |

| First Busey (BUSE) | $25.89 | $51.67 | 49.9% |

| Ellington Financial (EFC) | $12.10 | $23.90 | 49.4% |

| DNOW (DNOW) | $12.18 | $24.11 | 49.5% |

| Dime Community Bancshares (DCOM) | $34.41 | $67.79 | 49.2% |

Let's explore several standout options from the results in the screener.

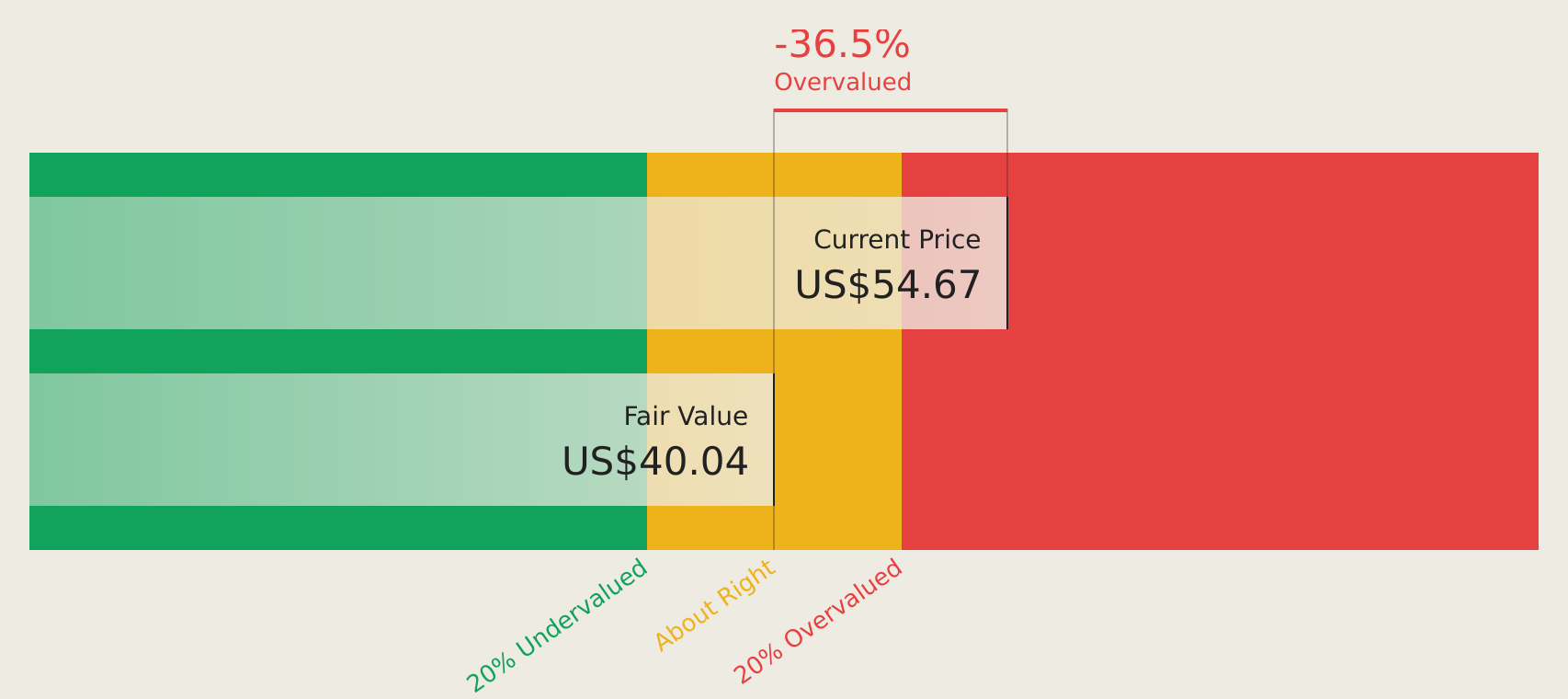

Kratos Defense & Security Solutions (KTOS)

Overview: Kratos Defense & Security Solutions, Inc. is a technology company that offers technology, hardware, products, systems, and software for defense, national security, and commercial markets globally with a market cap of approximately $12.57 billion.

Operations: The company's revenue segments include Unmanned Systems, generating $292 million, and Kratos Government Solutions, contributing $1.05 billion.

Estimated Discount To Fair Value: 13%

Kratos Defense & Security Solutions appears undervalued based on cash flows, trading at US$74.09 against a future cash flow estimate of US$85.15, suggesting a 13% discount to fair value. Despite recent shareholder dilution and volatile share prices, its earnings are projected to grow significantly at 32.7% annually, outpacing the market average. Recent contracts with the U.S. Navy and partnerships in hypersonic testing highlight Kratos' strong positioning in defense sectors, supporting potential revenue growth above market rates.

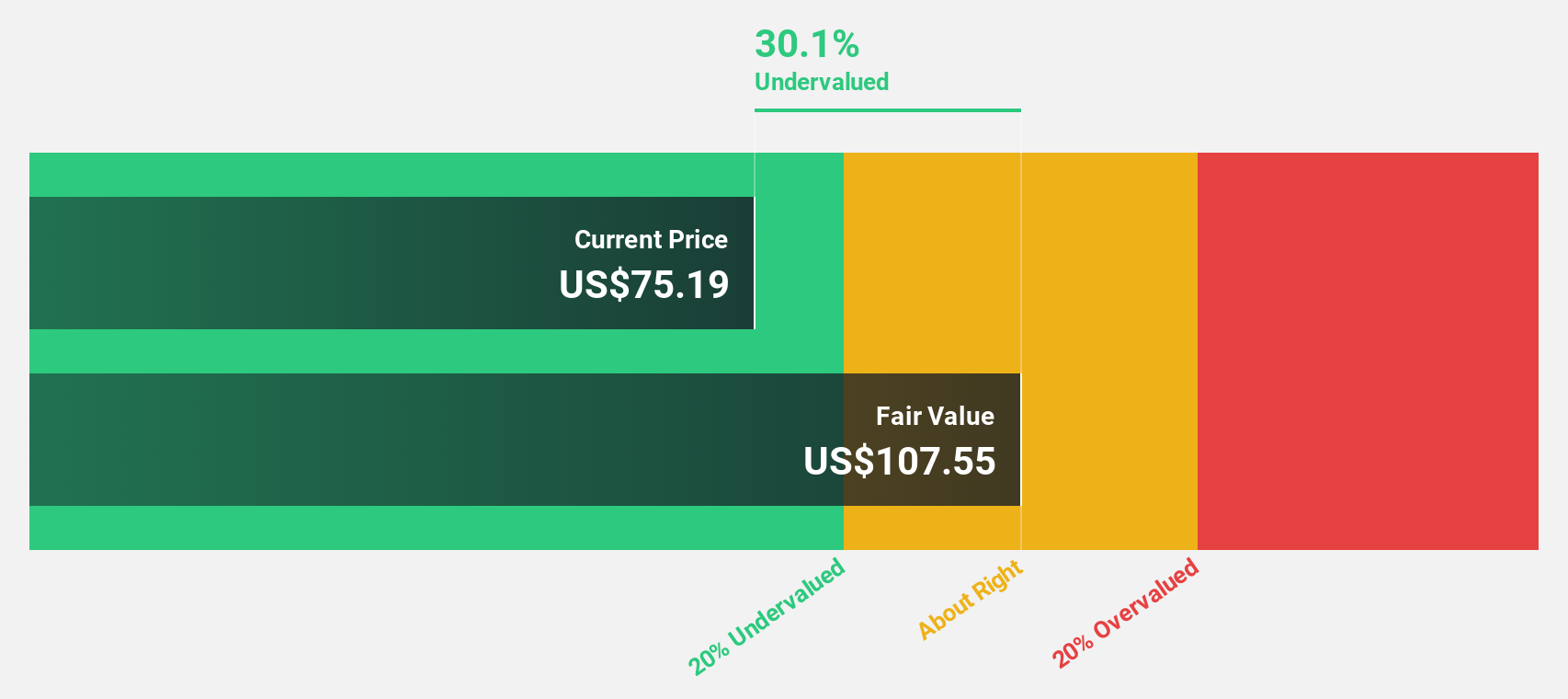

Estée Lauder Companies (EL)

Overview: The Estée Lauder Companies Inc. is a global manufacturer, marketer, and seller of skincare, makeup, fragrance, and hair care products with a market cap of approximately $25 billion.

Operations: The company's revenue segments include skin care at $7.14 billion, makeup at $4.21 billion, fragrance at $2.65 billion, and hair care at $564 million.

Estimated Discount To Fair Value: 22.2%

Estée Lauder Companies is trading at US$70.91, below its estimated future cash flow value of US$91.11, reflecting a 22.2% discount to fair value. Despite high debt levels and slower revenue growth projections than the market, earnings are forecast to grow significantly at 44.64% annually over the next three years as profitability improves. Recent merger discussions with Puig Brands could further enhance its market position amidst sector consolidation trends in beauty and fashion industries.

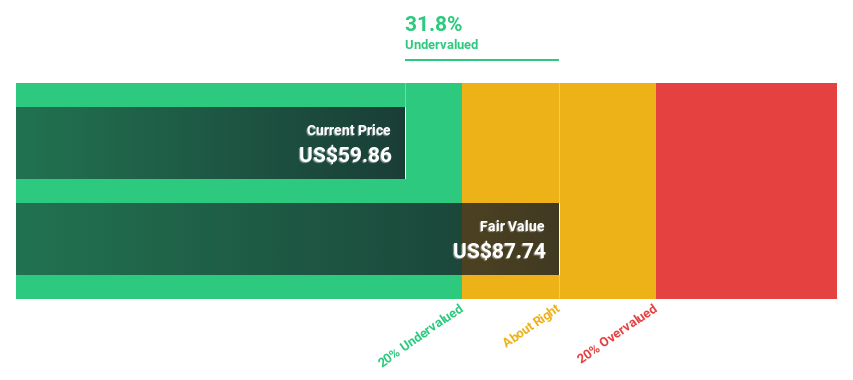

Somnigroup International (SGI)

Overview: Somnigroup International Inc., along with its subsidiaries, is engaged in the design, manufacturing, distribution, and retail of bedding products both in the United States and internationally, with a market cap of $15.33 billion.

Operations: The company's revenue segments include Mattress Firm at $3.51 billion, Tempur Sealy International at $1.27 billion, and Tempur Sealy North America at $3.68 billion.

Estimated Discount To Fair Value: 13.4%

Somnigroup International is trading at US$74.37, slightly below its estimated future cash flow value of US$85.87, indicating a modest undervaluation. Despite lower profit margins this year compared to last, earnings are projected to grow significantly at 20.6% annually, outpacing the broader U.S. market's growth rate. However, revenue growth forecasts lag behind market expectations, and debt coverage by operating cash flow remains a concern amidst recent strategic alliances enhancing its research capabilities in sleep health.

Make It Happen

- Get an in-depth perspective on all 161 Undervalued US Stocks Based On Cash Flows by using our screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.