A Look At Alpha Metallurgical Resources (AMR) Valuation After Mixed Q1 2026 Earnings And Ongoing Buybacks

Alpha Metallurgical AMR | 0.00 |

Alpha Metallurgical Resources (AMR) is back in focus after its first quarter 2026 results, which combined a narrower net loss and firmer adjusted EBITDA with softer revenue, an earnings miss, and reaffirmed full year guidance.

At a share price of $188.03, Alpha Metallurgical Resources has seen its share price return decline 7.4% year to date, even as the 1 year total shareholder return is 47.28%. This suggests longer term holders have been rewarded while recent momentum has cooled despite ongoing buybacks and insider equity grants.

If earnings volatility and buybacks have your attention, this can be a good moment to widen your search and check out 33 elite gold producer stocks

With the stock roughly 3% below its analyst price target, trading on an intrinsic value estimate that implies a steep discount and backed by heavy buybacks, the key question is whether this is a genuine mispricing or whether the market is already baking in future growth.

Most Popular Narrative: 8.1% Undervalued

With Alpha Metallurgical Resources last closing at $188.03 against a narrative fair value of $204.50, the current price sits below what the most followed model implies. This sets up a clear tension between market and narrative.

Global underinvestment and persistent supply constraints in metallurgical coal mining (compounded by recent industry idlings and bankruptcies) are likely to elevate future prices and market share for well-capitalized producers like Alpha, pointing to potential upside for future revenue and margins as demand recovers or steadies, especially in high-growth markets like India and Brazil.

Curious what underpins that higher fair value? The narrative leans heavily on future revenue expansion, margin rebuild, and a compressed earnings multiple. The exact mix of growth, profitability, and discounting assumptions might surprise you.

Result: Fair Value of $204.50 (UNDERVALUED)

However, you also need to factor in risks such as weaker steel demand putting pressure on met coal pricing and higher regulatory or environmental costs squeezing future margins.

Another Angle on Value

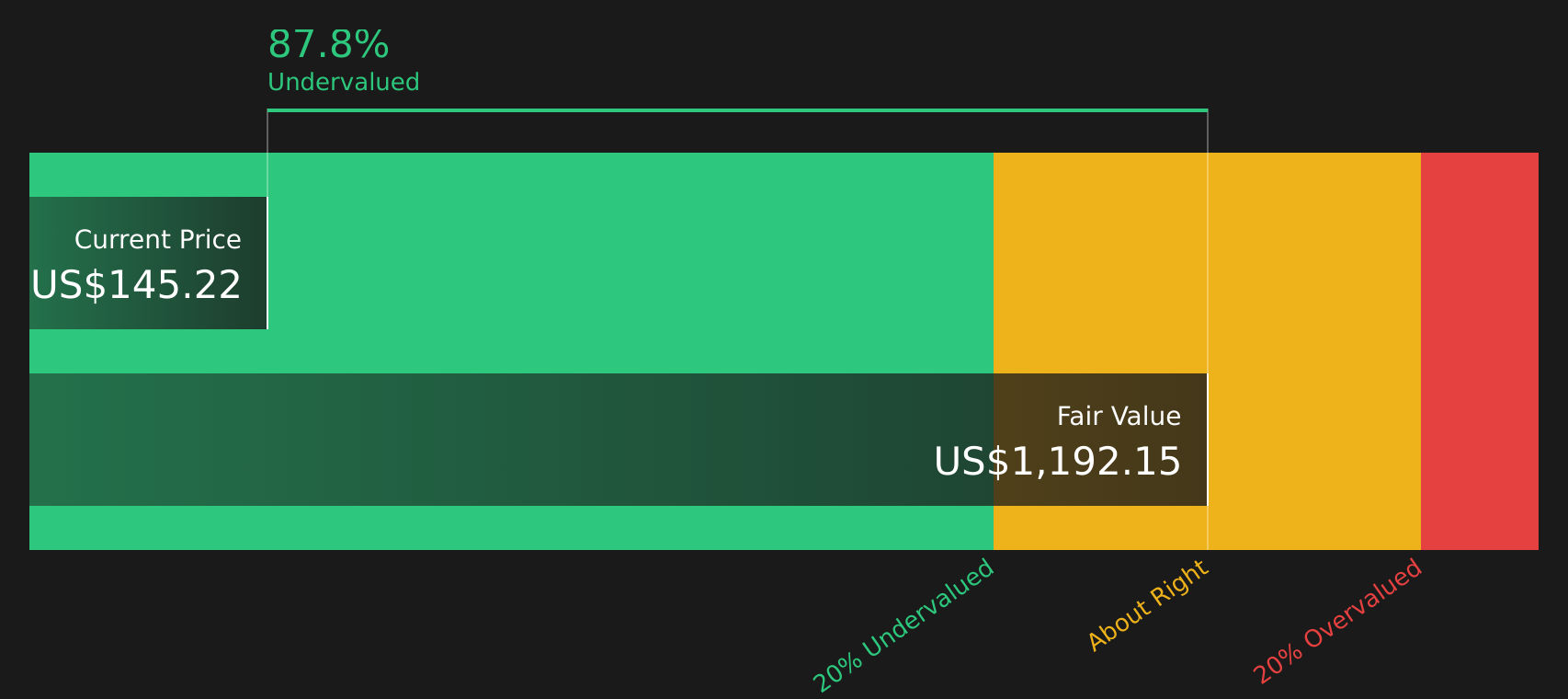

There is a twist here. While the narrative fair value suggests Alpha Metallurgical Resources is undervalued, our DCF model points to a far larger gap, with the stock trading at about 81.1% below its estimated future cash flow value. That kind of spread raises a simple question: is the model too optimistic or is the market too cautious?

Next Steps

Seeing mixed signals in the story so far? Take a closer look at the full picture yourself, then move quickly to weigh up the stock's 2 key rewards

Looking for more investment ideas?

If this story has sharpened your thinking, do not stop here, there are plenty of other stocks that could fit what you are looking for.

- Capture potential upside by scanning 45 high quality undervalued stocks that currently combine solid financial profiles with prices that sit below their estimated worth.

- Prioritise resilience by reviewing 70 resilient stocks with low risk scores that score well on balance sheet strength and business risk measures.

- Get ahead of the crowd by checking the screener containing 21 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.