A Look at Baker Hughes (BKR) Valuation Following Major Saudi Aramco Contract Expansion

Baker Hughes BKR | 0.00 |

Baker Hughes (BKR) just landed a multi-year agreement with Aramco to significantly expand its underbalanced coiled tubing drilling operations in Saudi Arabia. This expansion is notable for its potential impact on Baker Hughes’ business and presence in the region.

Baker Hughes’ new multi-year agreement with Aramco arrives on the back of sustained share price momentum. BKR is up 17% year-to-date and recent news like rising Saudi contracts and ongoing dividends seem to be fueling renewed optimism. Over the past 12 months, the stock delivered a strong 29.5% total shareholder return, and its 69.7% gain in three years highlights consistent long-term outperformance.

If you’re weighing new opportunities in energy and beyond, this is a perfect moment to broaden your horizons with fast growing stocks with high insider ownership

But with so much good news already fueling momentum, is Baker Hughes still undervalued at these levels, or has the market already priced in its next chapter of growth and international expansion?

Most Popular Narrative: 7.2% Undervalued

The most widely followed narrative values Baker Hughes at $52.43 per share, versus its last close at $48.64. This outlook is more optimistic for the stock. The narrative uses a discount rate of 7.63% and expects a combination of earnings stability and sector transitions to drive future value.

The company's strong momentum in securing large-scale service contracts, framework agreements, and technology-driven orders (such as for data centers, LNG, CCS, and recurring gas tech services) is driving an all-time high IET backlog. This builds strong visibility into future revenue and supports sustained earnings durability.

Want to see the surprising math behind this target? The key factor driving it is a mix of recurring revenue, higher margins, and aggressive assumptions about how digital technology and industrial services reshape Baker Hughes' profit profile. Curious if analysts are expecting margin expansion, rapid contract wins, or something even bigger? Dive in for the full story that builds this bullish case.

Result: Fair Value of $52.43 (UNDERVALUED)

However, persistent cost inflation or an unexpected drop in oil and gas demand could quickly challenge these optimistic assumptions and change Baker Hughes' growth outlook.

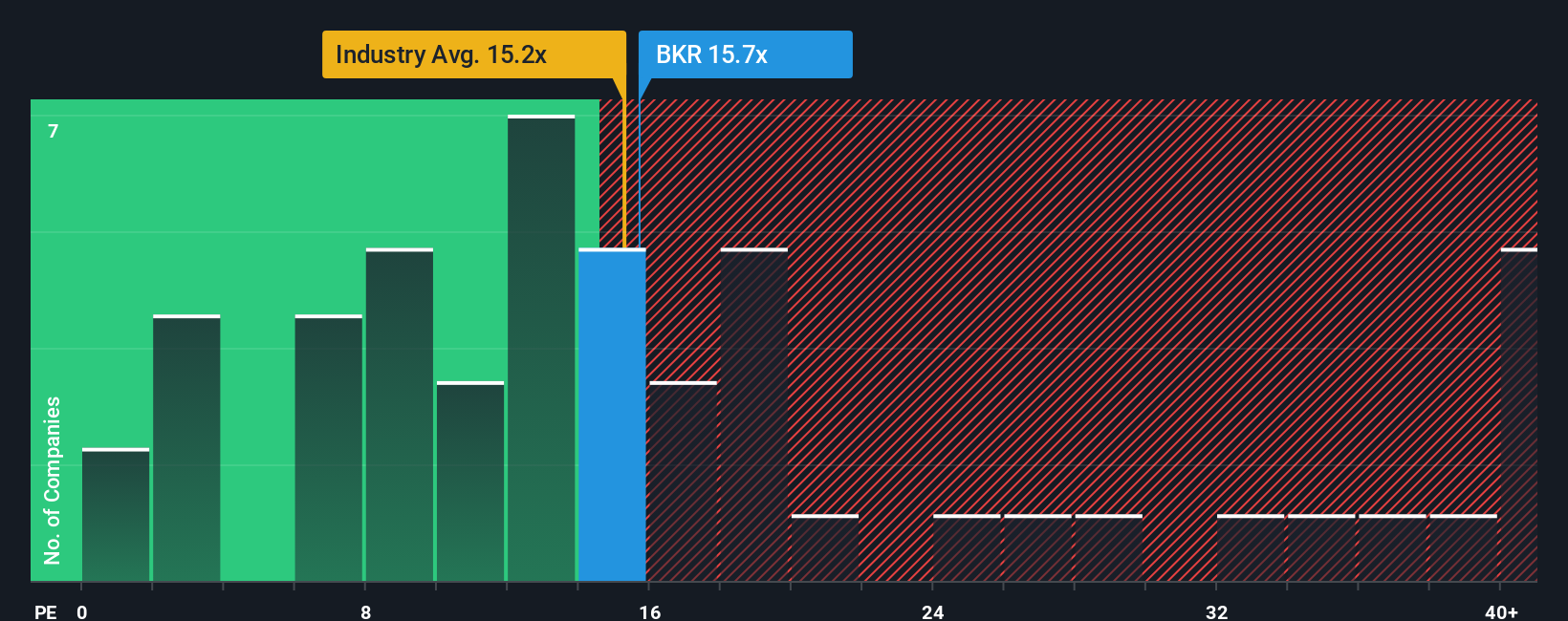

Another View: Looking at Earnings Multiples

But if we switch to the classic price-to-earnings lens, Baker Hughes actually trades at 16.6x, slightly above both its US Energy Services peers (16.1x) and the industry average (16.4x). While this premium suggests optimism about the future, it also means the stock may not be the bargain some expect. Might the market be pushing expectations a bit too far?

Build Your Own Baker Hughes Narrative

Don't forget, you can dive into the numbers yourself and shape your own view. Exploring your own analysis takes just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Baker Hughes.

Ready for More Smart Stock Picks?

There are countless ways to get ahead of the crowd. See what’s moving markets next by exploring these handpicked opportunities tailored to your interests.

- Spot tomorrow’s most promising players by scanning these 843 undervalued stocks based on cash flows, a resource filled with hidden gems trading below their fair value.

- Start cashing in on innovation and technological progress with these 26 AI penny stocks, featuring companies shaping artificial intelligence breakthroughs worldwide.

- Make your portfolio work harder by checking out these 18 dividend stocks with yields > 3%, which highlights quality picks with healthy yields above 3% for steady income potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.