A Look At Blackstone Mortgage Trust’s (BXMT) Valuation After Profit Return And Loan Book Cleanup

Blackstone Mortgage Trust, Inc. Class A BXMT | 0.00 |

Blackstone Mortgage Trust (BXMT) is back in the spotlight after reporting full year profitability, highlighting that 99% of its loan portfolio is performing, and naming long time finance executive Marcin Urbaszek as its new Chief Financial Officer.

Despite the strong full year earnings rebound and the high share of performing loans, Blackstone Mortgage Trust’s recent share price moves have been relatively muted. The share price is US$19.54, and the 90 day share price return of 6.54% contrasts with a 1 year total shareholder return of 5.96%. This suggests momentum has picked up in the short term as investors react to the portfolio clean up and the CFO transition.

If this mix of income, credit risk and leadership change has you rethinking your watchlist, it could be a good moment to scan our 23 top founder-led companies for other potential ideas.

With BXMT back in profit, a 99% performing loan book, and the share price still close to US$19.54, you have to ask: is there an undervalued income story here, or is the market already pricing in the recovery?

Most Popular Narrative: 6.7% Undervalued

At a last close of $19.54 versus a narrative fair value of $20.94, the most followed view sees a modest gap that depends on how BXMT reshapes its loan book and earnings mix over the next few years.

The company is focusing on portfolio turnover through repayments and redeployment into high-quality new credit opportunities, which is expected to enhance future earnings by improving the overall credit composition and potentially increasing revenue from new investments.

Want to see what this portfolio reshuffle could mean for future earnings power and valuation multiples? The narrative focuses on shifting margins, a changing revenue mix and a different balance between impaired and performing assets. Curious how those moving parts feed into its fair value math and that small pricing gap to today’s share price? The full narrative lays out the numbers behind that story.

Result: Fair Value of $20.94 (UNDERVALUED)

However, there are still watchpoints, including the US$970 million of impaired loans and the risk that slower loan repayments could drag on earnings and capital redeployment.

Another Angle On Valuation

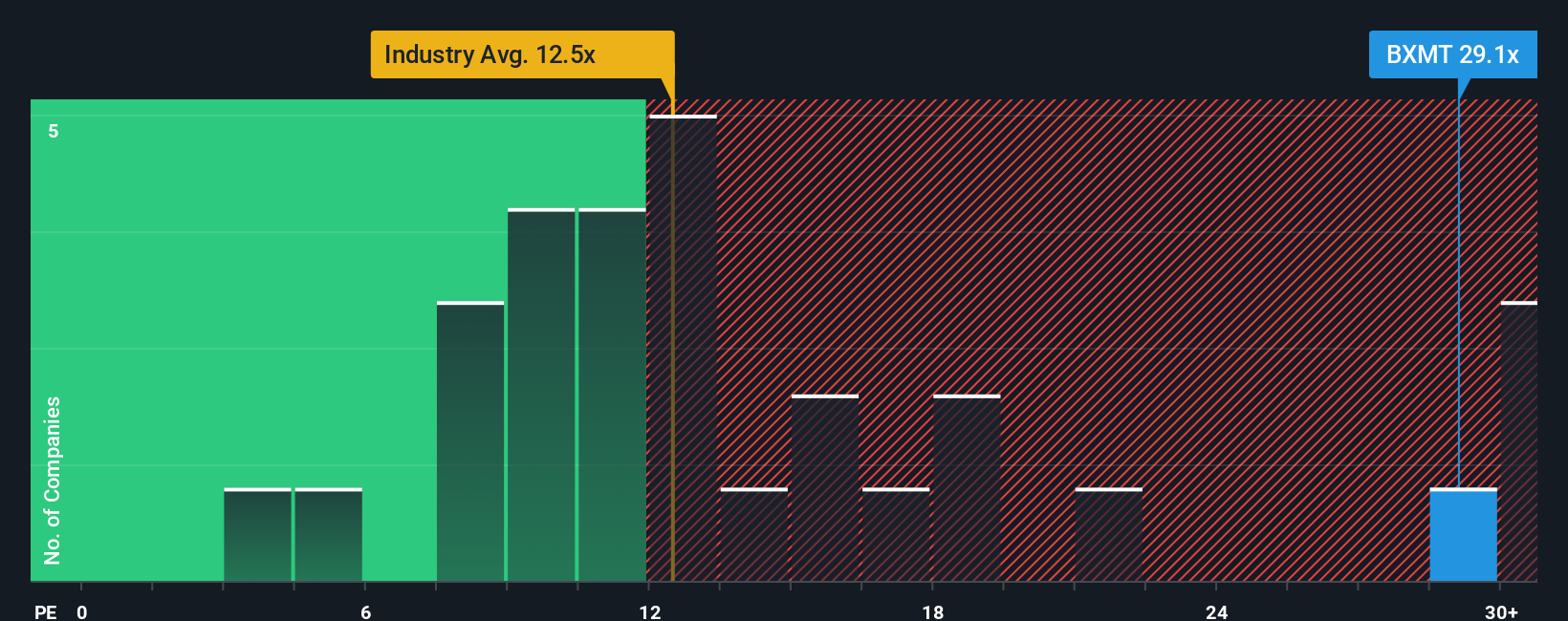

That 6.7% gap between the $19.54 share price and the $20.94 fair value looks modest, but the current P/E of 30.5x tells a different story. It is roughly double both the US Mortgage REITs industry at 12.4x and the peer average and the fair ratio, each at 15.7x.

In plain terms, the share price already bakes in a lot of optimism, so any wobble in earnings or credit quality could matter more than it would for a cheaper stock. The question for you is whether that kind of premium feels like a cushion or a tightrope.

Build Your Own Blackstone Mortgage Trust Narrative

If you are not sold on this view or prefer to lean on your own research, you can pull up the same data and build a narrative that fits your take in just a few minutes, Do it your way.

A great starting point for your Blackstone Mortgage Trust research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If BXMT has sharpened your focus, do not stop here. Cast a wider net with screeners that surface different types of opportunities you might otherwise miss.

- Target potential mispricing by scanning companies that look attractive on both quality and value using our 54 high quality undervalued stocks.

- Strengthen your income watchlist by checking out businesses highlighted in our 13 dividend fortresses.

- Cut down on unwelcome surprises by reviewing candidates surfaced through our 83 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.