A Look At Energy Transfer (ET) Valuation After Raised EBITDA Outlook And Project Expansion Plans

Energy Transfer ET | 0.00 |

Energy Transfer (ET) just posted first quarter earnings that paired higher sales with slightly lower earnings per unit, prompting management to lift full year EBITDA guidance and capital spending plans, supported by record transportation volumes.

Energy Transfer’s share price has climbed 18.2% year to date to $19.61, with an 8.28% 90 day share price return and a 179.54% five year total shareholder return, which points to strong, longer term momentum around its cash flow and project pipeline.

If this kind of infrastructure driven story interests you, it is worth widening the lens and checking out 36 power grid technology and infrastructure stocks

With Energy Transfer lifting EBITDA guidance, boosting spending on new projects and offering a distribution backed by strong cash flow, the key question for you is whether the current price still leaves upside or if the market is already pricing in future growth.

Most Popular Narrative: 12% Undervalued

At $19.61, the most followed narrative points to a fair value of $22.26, which frames Energy Transfer as trading at a discount that hinges on very specific growth and margin assumptions.

The company's NGL export capacity expansions at the Nederland terminal and new pipeline loopings position it to benefit from increased U.S. hydrocarbon exports to international markets, supporting sustained throughput and export revenues as global energy demand rises. Recent long-term, investment-grade customer commitments on multi-billion-dollar projects de-risk cash flows and improve visibility into earnings growth, while the buildout of vertically integrated infrastructure (such as Lake Charles LNG tied to ET pipelines) enhances both margins and return on invested capital.

Want to see what sits behind that fair value gap? The narrative ties together projected revenue growth, modest margin uplift and a future earnings multiple that is far from conservative.

Result: Fair Value of $22.26 (UNDERVALUED)

However, this depends on major natural gas and LNG projects being completed on time and within budget, and on crude and NGL volumes not declining more than analysts expect.

Another View: Valuation Through Earnings Multiples

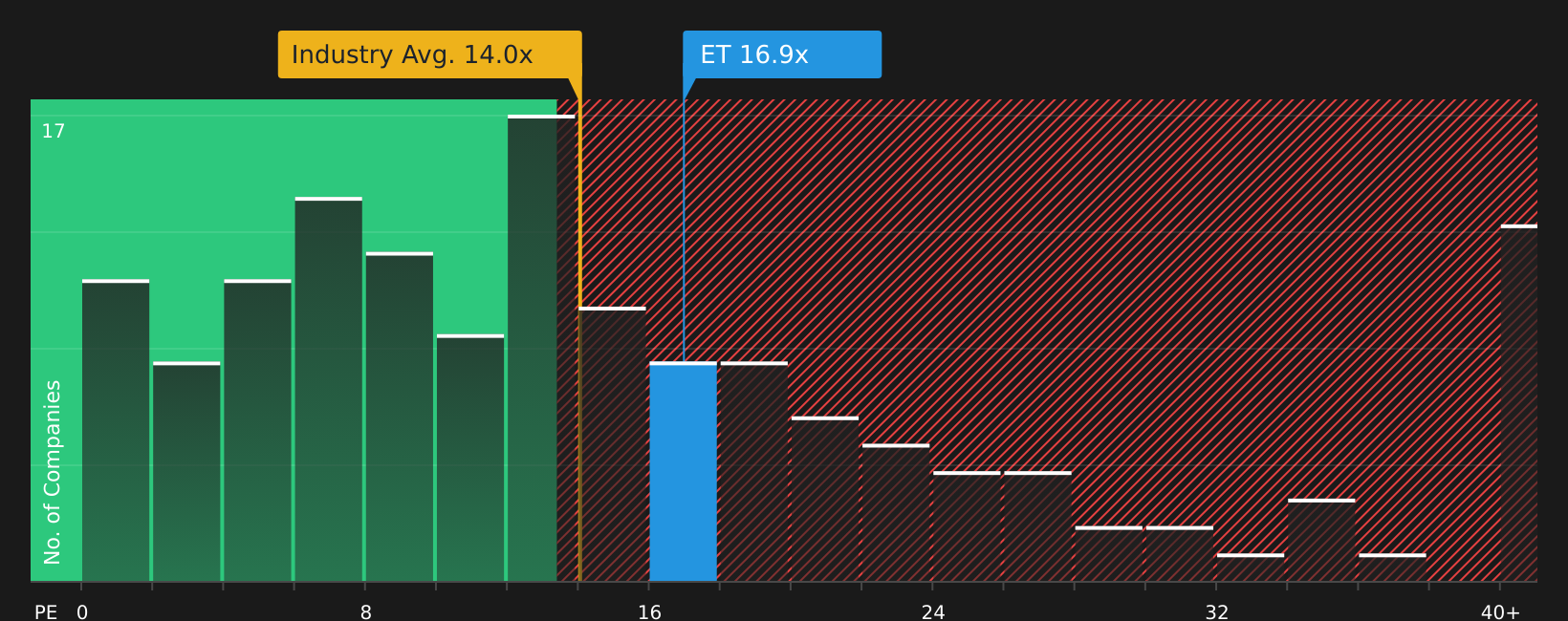

The analyst narrative points to a fair value of $22.26, but current earnings-based metrics are a bit more mixed. At a P/E of 16.4x, Energy Transfer trades above the US Oil and Gas industry average of 14.2x, yet below the peer average of 18.3x, while the fair ratio estimate sits much higher at 29.6x. That split suggests room for either catch up or a rethink of the optimism baked into the fair ratio. Which side of that range do you find more realistic?

Next Steps

With sentiment split between upside potential and clear risks, it makes sense to look at the data yourself, decide quickly where you stand, and weigh up the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with a single stock story. Use focused stock lists to widen your opportunity set with discipline.

- Target resilience by reviewing companies in the 70 resilient stocks with low risk scores that keep risk scores in check while still offering equity upside.

- Hunt for quality at a sensible price by scanning the 47 high quality undervalued stocks where stronger fundamentals meet potentially more attractive valuations.

- Spot potential early movers by checking the 26 elite penny stocks with strong financials that pair smaller market caps with comparatively stronger financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.