A Look At Envista Holdings (NVST) Valuation After Recent Share Price Momentum

Envista Holdings NVST | 27.38 27.38 | +1.75% 0.00% Pre |

Envista Holdings (NVST) has been drawing attention after recent share price moves, with the stock closing at $28.97. For investors, the question now is how this dental-focused business lines up against its fundamentals.

The recent rise to a 1 month share price return of 14.78% and 90 day share price return of 51.44% comes after a weaker 3 year total shareholder return of 24.71%. This suggests momentum has picked up recently.

If Envista’s move has you thinking about where else capital could work, this could be a good moment to look at 25 healthcare AI stocks as another potential hunting ground.

So, with Envista posting a 1-year total return of 33.9963% but still trading at a 5.12% intrinsic discount, are you looking at a genuine value opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 17.2% Undervalued

Envista’s most followed narrative pegs fair value at $35.00, above the last close at $28.97, which puts the company’s earnings power assumptions firmly in focus.

While consensus expects digital dentistry adoption to be an incremental growth driver, Envista's deepening R&D investment and rapid rollout of AI-integrated imaging, diagnostics, and workflow solutions, combined with strong traction in premium digital offerings through DSOs, could fuel an outsized shift toward high-margin, recurring software and service revenue, materially enhancing net margins and long-term earnings power.

Curious what kind of revenue mix change and margin lift would justify that $35.00 mark, all discounted at an 8.37% rate? The full narrative lays out how earnings, profitability and the future P/E all need to line up for Envista to earn that valuation anchor.

Result: Fair Value of $35.00 (UNDERVALUED)

However, that $35.00 fair value anchor still rests on assumptions that could be tested if digital adoption stalls or if margin pressure from tariffs and pricing intensifies.

Another Way To Look At Valuation

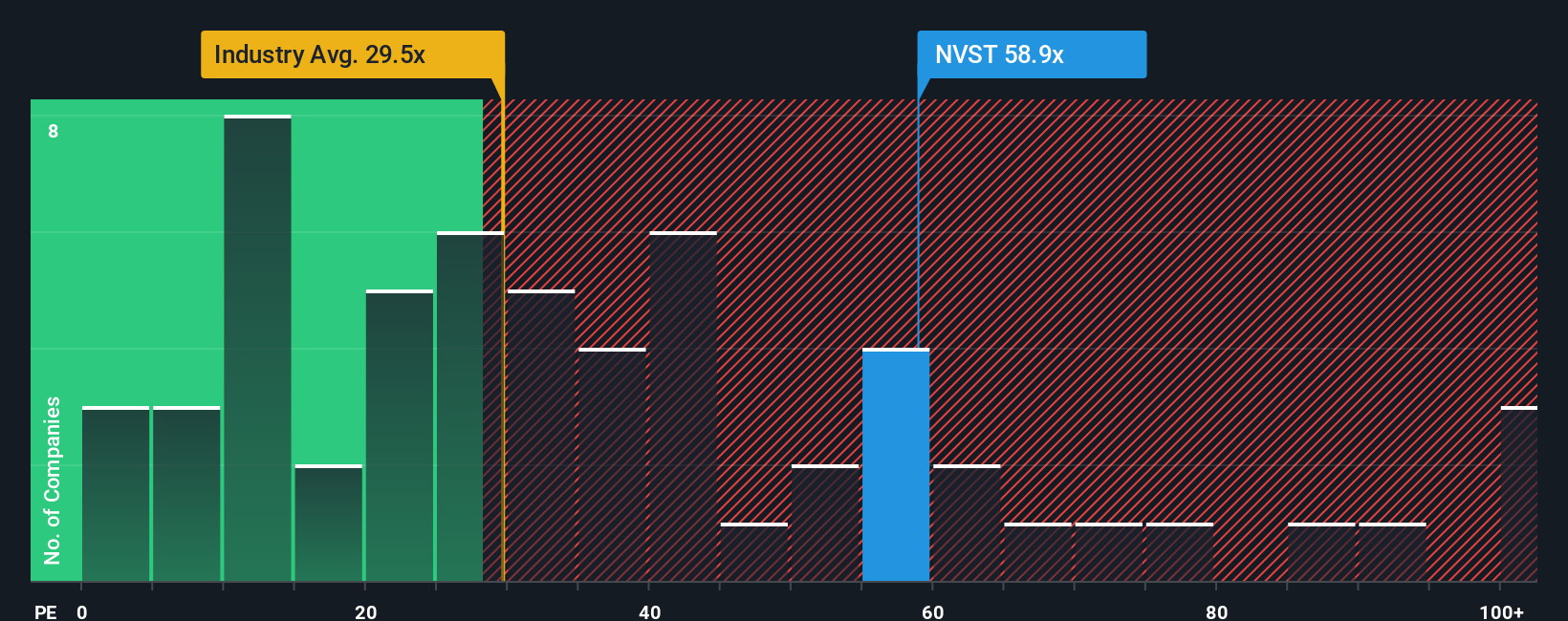

The earlier fair value work points to Envista trading at a discount, but the P/E picture tells a different story. NVST changes hands at about 101x earnings, compared with a fair ratio of 33x, the US Medical Equipment industry on 30.4x and peers on 70.5x, which leans toward valuation risk rather than a clear bargain. With that kind of gap, are you comfortable that future earnings can catch up to this price, or do you want a wider margin of safety?

Next Steps

If this mix of upside potential and valuation questions leaves you on the fence, act while the data is fresh and shape your own view with 3 key rewards.

Looking for more investment ideas?

If Envista has sharpened your focus, do not stop here; broaden your watchlist with other ideas that fit your style before the next opportunity moves away.

- Target potential mispricing by scanning our 54 high quality undervalued stocks, which pairs quality fundamentals with room for sentiment to catch up.

- Build a steadier income stream by reviewing the 13 dividend fortresses, which combines higher yields with an emphasis on resilience.

- Strengthen your core holdings by checking the solid balance sheet and fundamentals stocks screener (44 results) and focus on companies with financial foundations that can support their plans.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.