A Look At Fastenal (FAST) Valuation After Revenue Meets Expectations But EBITDA Misses

Fastenal Company FAST | 0.00 |

Fastenal (FAST) just reported quarterly revenue in line with expectations, but a miss on EBITDA estimates prompted a 10.8% share price drop. This has put the focus squarely on how the company is balancing growth and profitability.

That EBITDA miss came after a strong run, with the share price still up 10.83% year to date and a 5 year total shareholder return of 92.79%. However, recent 3 month momentum has faded slightly.

If this earnings move has you reassessing your watchlist, it could be a good moment to broaden your search and check out 35 power grid technology and infrastructure stocks

With the stock still up year to date and trading only slightly below the average analyst price target, the key question now is whether Fastenal is trading at a fair premium or if recent weakness has opened a genuine buying window that markets have not fully priced in.

Most Popular Narrative: 3.6% Undervalued

Fastenal's most followed narrative places fair value at $46.49, slightly above the last close of $44.82, which frames the recent pullback as a relatively small gap to that estimate.

The analysts have a consensus price target of $46.49 for Fastenal based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0, and the most bearish reporting a price target of just $39.9.

To see what underpins that fair value, the narrative focuses on steady revenue expansion, firm profit margins, and a future earnings multiple that assumes sustained execution strength.

Result: Fair Value of $46.49 (UNDERVALUED)

However, this depends on tariffs and trade tensions not eroding margins, and on higher inventory levels not tying up too much cash or reducing flexibility.

Another Take: Valuation Looks Full On Earnings

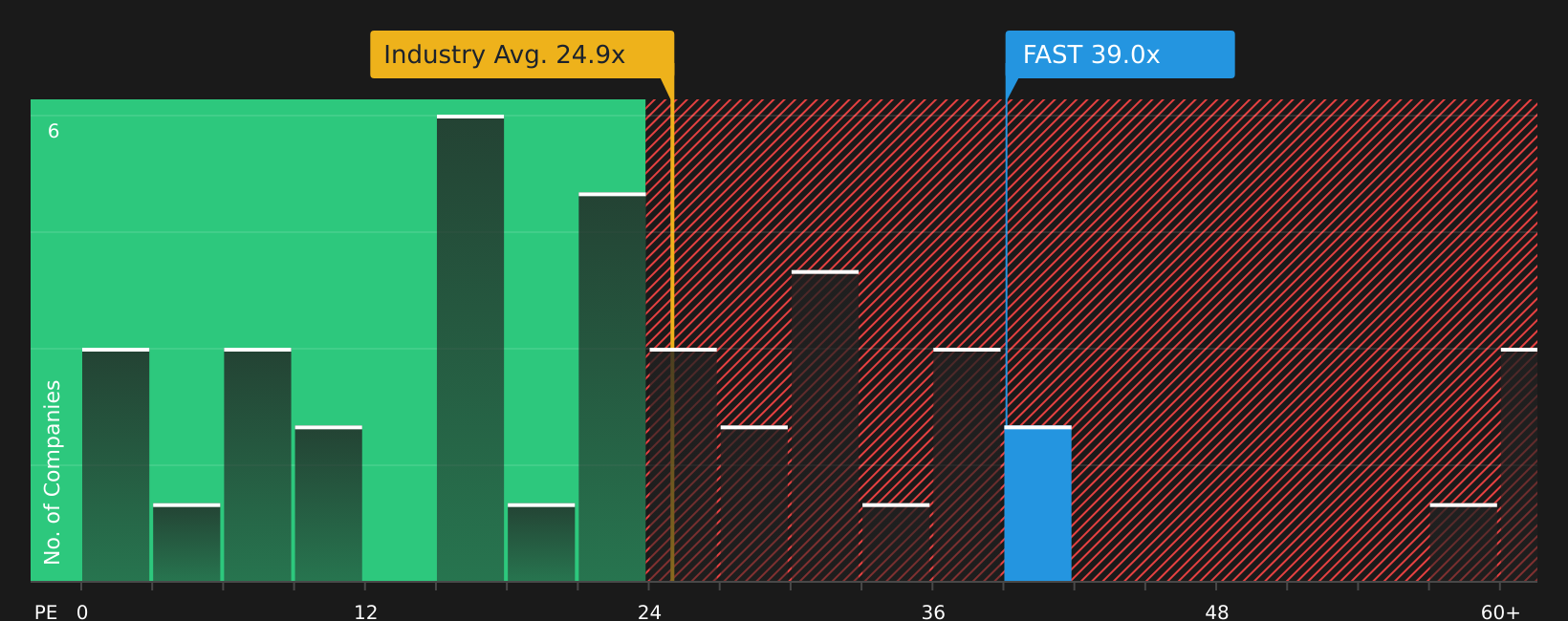

The analyst narrative points to Fastenal being 3.6% undervalued at $46.49 fair value, yet the current P/E of 39.3x sits well above the US Trade Distributors industry at 23.5x, the peer average at 24.7x, and the fair ratio of 29.6x. That premium suggests less margin for error if growth or margins fall short, so the real question is whether you think the business can keep justifying that kind of multiple.

Next Steps

With sentiment clearly split between potential upside and valuation risk, this is a moment to look through the numbers yourself and move quickly while opinions are forming. To weigh both sides with a clear lens, start by checking the 2 key rewards and 1 important warning sign.

Ready to find your next idea?

If Fastenal is already on your radar, this is a good time to widen the field and line up a few more stocks that could strengthen your portfolio.

- Spot potential mispricing and back your research with numbers by scanning 46 high quality undervalued stocks across the market.

- Focus on income-oriented ideas by zeroing in on companies screened as 10 dividend fortresses that may support regular cash returns.

- Prioritise resilience by concentrating on companies highlighted in 64 resilient stocks with low risk scores before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.