A Look At GeneDx Holdings (WGS) Valuation After Guidance Cut And First Quarter 2026 Results

GeneDx Holdings Corp. Class A WGS | 0.00 |

GeneDx Holdings (WGS) is back in focus after first quarter 2026 results showed revenue of US$102.25 million, a net loss of US$63.32 million, and a cut to full year revenue guidance.

The latest earnings release and guidance cut came alongside sharp share price swings, with a 16.68% 1 day share price return but a 69.39% year to date share price decline. At the same time, the 3 year total shareholder return remains very large, suggesting recent momentum has faded even after earlier gains.

If GeneDx’s volatility has you looking across healthcare and AI, this could be a good moment to scan for other genomic and diagnostics players using our screener for 35 healthcare AI stocks

With the stock down 69.39% year to date, but still showing a very large 3 year total shareholder return and guidance now reset lower, are you looking at an undervalued genomics player or a stock already pricing in future growth?

Most Popular Narrative: 73% Undervalued

Against a last close of $40.50, the most followed narrative pegs GeneDx’s fair value near $148.89, creating a wide gap that hinges on aggressive long term assumptions.

Rapid expansion into new and underpenetrated markets, including general pediatrics (driven by American Academy of Pediatrics guidelines), NICU, and additional pediatric specialties, positions GeneDx for substantial future volume and revenue growth as adoption of genomics as a frontline diagnostic tool accelerates.

Scaling proprietary AI-powered genomic interpretation platforms and integrating newly acquired Fabric Genomics technology enhances efficiency and accuracy, which should both lower per-sample costs and support margin expansion as the business grows.

Want to see what kind of revenue path and margin turnaround sit behind that valuation gap? The narrative leans on ambitious growth, expanding profitability and richer reimbursement assumptions.

Result: Fair Value of $148.89 (UNDERVALUED)

However, this depends on reimbursement support and faster adoption. If payer policies tighten or physician uptake stalls, those assumptions quickly become much tougher to meet.

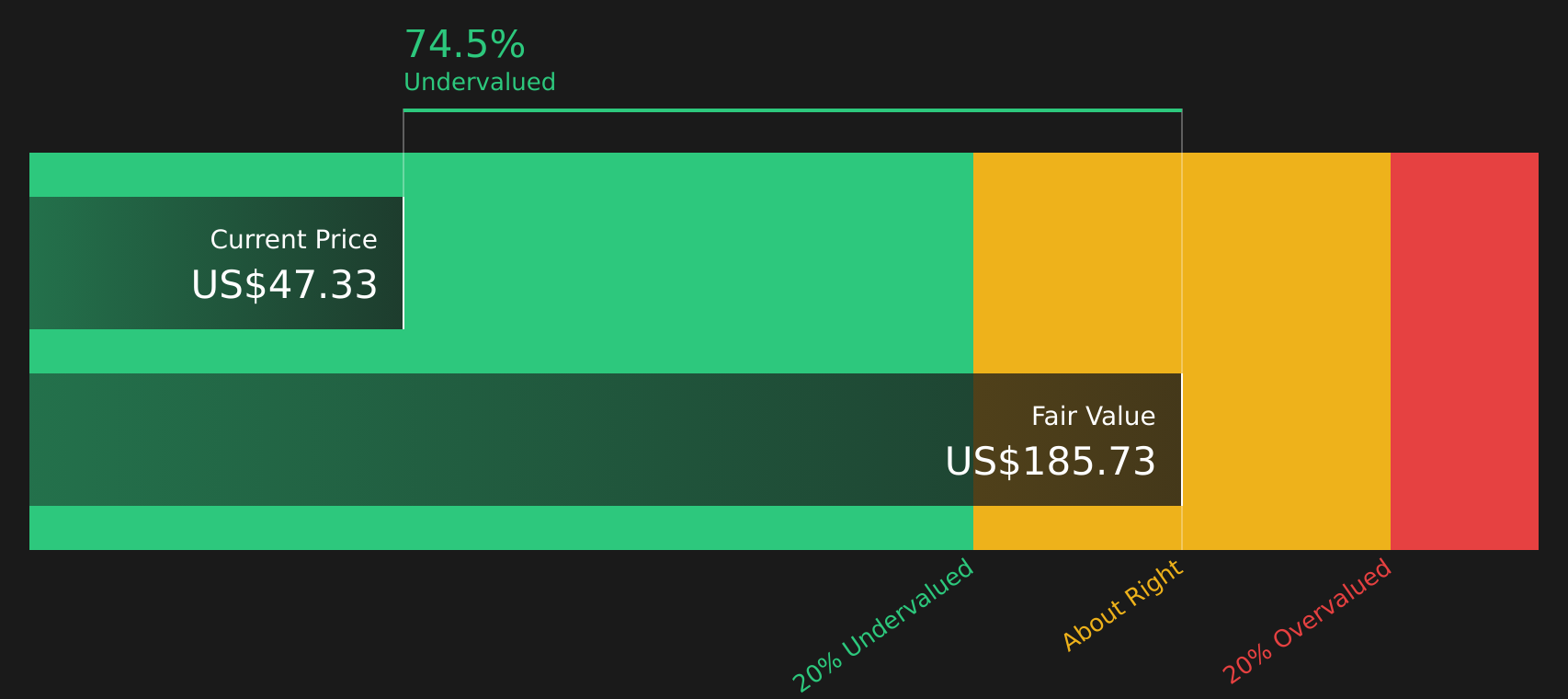

Another View On Valuation

Analyst narratives point to a fair value near $148.89. The SWS DCF model presents a higher estimate of $185.90 at a $40.50 share price. Both methods indicate that GeneDx is undervalued, but they rely on different growth and margin assumptions. Which set of assumptions do you find more realistic?

Next Steps

The mix of risks and potential rewards in this story is hard to ignore, so take a close look at the details and decide quickly where you stand with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop with a single stock; broaden your watchlist now with focused sets of companies that fit clear, tested criteria.

- Target potential bargains in quality companies by scanning the 51 high quality undervalued stocks that match solid fundamentals with attractive prices.

- Prioritize strength and resilience by reviewing the solid balance sheet and fundamentals stocks screener (44 results) that keep debt in check and liquidity in focus.

- Hunt for early opportunities by checking the screener containing 23 high quality undiscovered gems that combine strong financials with lower investor attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.