A Look At Hannon Armstrong (HASI) Valuation After Its C‑Corp Transition And Capital Light Growth Shift

HA Sustainable Infrastructure Capital, Inc. HASI | 39.66 | +0.03% |

Why HASI's C-Corp shift is back in focus

HA Sustainable Infrastructure Capital (HASI) is back on investor radars after recent analysis emphasized its transition to a C-Corporation, highlighting capital retention and a more capital light approach to funding future infrastructure deals.

HASI’s recent C-Corp shift and focus on more capital light deal funding appear to be landing with investors, with a 1-month share price return of 7.98% and year to date share price return of 13.54% alongside a 1-year total shareholder return of 35.51%. However, the 5-year total shareholder return of a 24.77% decline shows the longer track record has been tougher.

If this kind of transition story interests you, it could be a good moment to widen your search and check out 24 power grid technology and infrastructure stocks as another way to find infrastructure related ideas.

With the shares up strongly over the past year and trading at a discount to the average analyst price target and some intrinsic value estimates, it is reasonable to ask whether there is still an attractive entry point or if the market is already fully pricing in future growth.

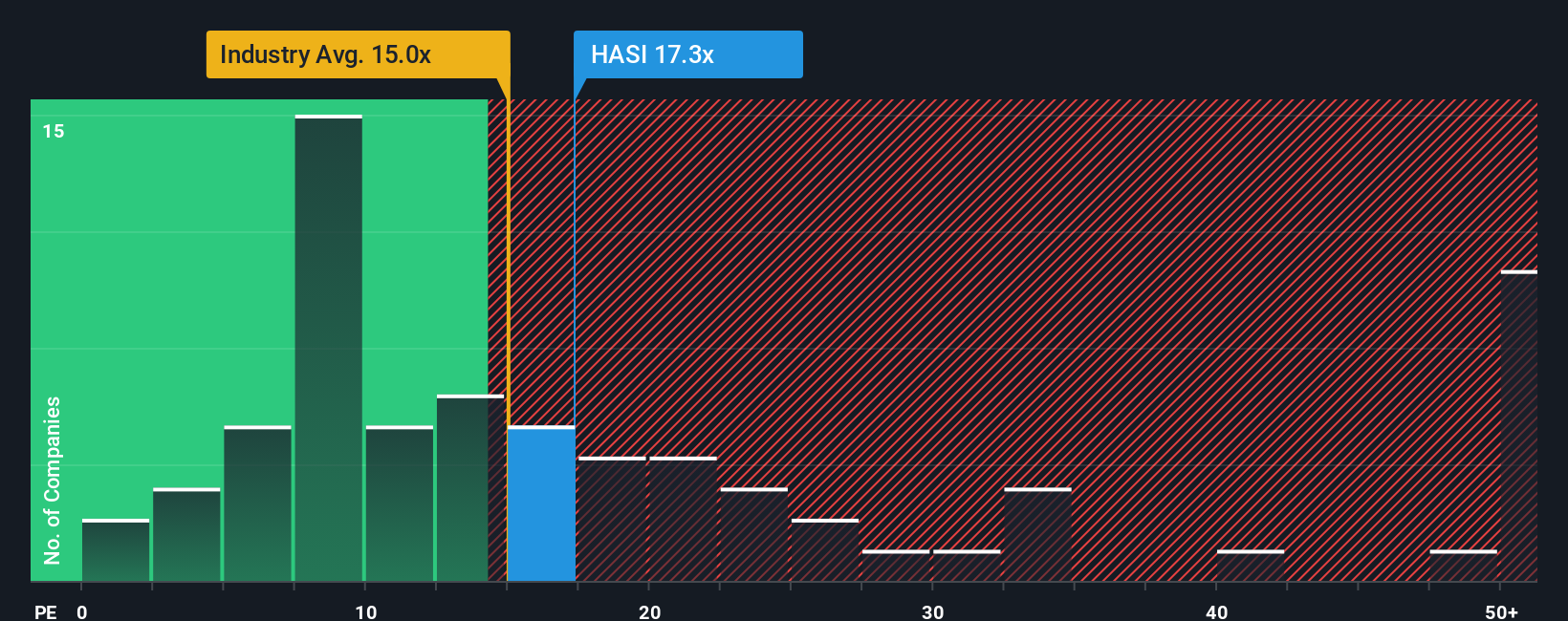

Price-to-Earnings of 14.9x: Is it justified?

Based on our SWS DCF model, HA Sustainable Infrastructure Capital has an estimated future cash flow value of $41.97 per share, compared with the last close of $36.13, which points to a 13.9% discount to that fair value estimate.

The DCF model estimates what a company might generate in cash over time, then brings those future cash flows back to today using a discount rate to reflect risk and the time value of money. It is a cash flow focused lens, rather than one built purely on earnings or revenue multiples.

For HA Sustainable Infrastructure Capital, this approach can be useful because the business is tied to long term energy efficiency, renewable power and other sustainable infrastructure projects, where contract structures and financing terms influence cash generation as much as headline earnings. The model is effectively asking whether the current $36.13 price fully reflects those projected cash flows, or if the current discount leaves some room between market pricing and the SWS DCF estimate of $41.97.

Result: DCF fair value of $41.97 (UNDERVALUED)

However, you still need to weigh the tougher 5 year total return record and the possibility that infrastructure project cash flows differ from DCF assumptions.

Another angle on the valuation

That same 14.9x P/E that looks inexpensive versus peers at 30.9x and the US Diversified Financial industry at 15.8x sits slightly above a fair ratio of 14.6x. In plain terms, the market is offering a relative discount. However, with only a slim cushion to that fair ratio, how much room for error is really there?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HA Sustainable Infrastructure Capital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HA Sustainable Infrastructure Capital Narrative

If you look at these numbers and reach a different conclusion, or simply want to piece the story together your own way, you can spin up a custom view, test your assumptions against the same data set, and shape a thesis that fits your style, all in just a few minutes with Do it your way

A great starting point for your HA Sustainable Infrastructure Capital research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If HASI has you thinking differently about your portfolio, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target potential value opportunities early by scanning companies our screener flags as 52 high quality undervalued stocks with solid fundamentals backing their prices.

- Prioritize resilience and financial strength by focusing on businesses highlighted in our solid balance sheet and fundamentals stocks screener (45 results) that may better handle tough conditions.

- Aim to spot lesser known opportunities before the crowd by reviewing the screener containing 24 high quality undiscovered gems that currently look underfollowed yet financially compelling.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.